Cheaper oil's great and not-so-great news

Crude oil hasn't been acting much like black gold these days.

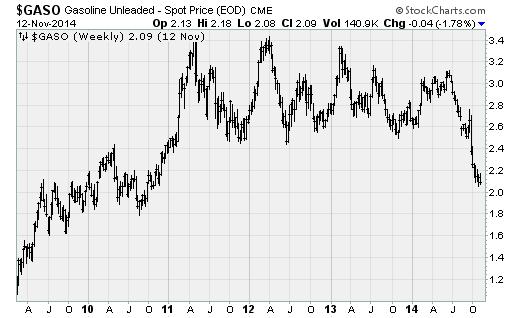

More like the Black Death in the way it has been sliding relentlessly lower since peaking in June. From a high of nearly $108 a barrel, West Texas Intermediate has fallen nearly 30 percent, losing almost 4 percent on Thursday to close around $74.30 a barrel -- a level last seen in 2011. Wholesale gasoline futures have fallen even more and are now back their price from late 2010.

Many catalysts are in play.

OPEC seems unwilling to countenance a production cut, with Saudi Arabia in particular not taking any action, as the chatter of a price war designed to crush U.S. shale oil producers grows louder. This is somewhat surprising because rising social spending by many OPEC members has increased their reliance on higher oil prices.

The massive rally in the greenback is probably more important, however. The U.S. Dollar Index (measuring the dollar against a basket of other currencies) has increased 10 percent from its July low to return to the highs tested in 2009 and again in 2010. Further upside moves would put levels not seen since 2006 in play.

Fueling the dollar's rise is the relative health of the U.S. economy, the end of the Federal Reserve's QE3 bond-buying stimulus in October, the yen-destroying antics of the Bank of Japan and widespread expectations that the European Central Bank will need to start a more aggressive bond-buying program of its own.

The result of the dramatic drop in energy prices has been mixed.

Clearly and unequivocally, this is fantastic news for American consumers still waiting for a rebound in wages. Inflation-adjusted household income is down nearly nine percent from a high of roughly $57,000 in 1999. Less take home pay is part of this. But a higher cost of living has played a role as well.

Cheap prices at the pump will help turn this measure around and will magnify the benefit of any increase in wage inflation.

Yet the drop in oil prices is also fanning fears of a deflation scare given that it's coming in the context of a general pullback in commodity prices and economic slowdowns across Asia and Europe.

While most people would consider deflation, or falling prices, a good thing, it would be disastrous now given high debt levels, a Fed that is far from a neutral policy stance and the risk it would result in economic weakness as consumers and business hold off on purchases in the hope of cheap prices later.

In fact, John Higgins at Capital Economics believes the stock market's limited reaction to the drop in energy prices -- and the hope for a strong holiday shopping season as consumers enjoy a lift in disposable income -- reflects concerns about global economic growth inherent in the decline of oil and other industrial commodity prices.

Part of the problem is that the energy sector, including stocks like Exxon Mobil (XOM), is so heavily weighted in the S&P 500 that lower oil prices tend to drag the overall market lower -- despite the strength of stocks in areas like transportation, which benefit from cheaper energy.

So, while lower gas prices are great for American shoppers, an outright collapse in oil would be bad if it's the result of things like currency market volatility, deflation concerns and economic weakness. Truly, too much of a good thing could lead to problems.