Why CDs can still be better than bonds

(MoneyWatch) These days, I am often advising clients to put a greater percentage of their fixed income into bond funds than I have in the past. I'm also using certificates of deposit a bit less. Here's why and what it means to you.

Background

For over a decade, I've been recommending longer-term CDs with easy early withdrawal penalties as substitutes for bonds. That's because rising rates can clobber bonds and bond funds, whereas CDs with small early withdrawal penalties offer intermediate-term yields with an insurance policy to escape if interest rates go up. Liam Pleven at The Wall Street Journal compared the small penalty to the deductible on an insurance policy.

The strategy worked quite well as interest rates continued to decline. While my clients didn't exercise the insurance by bailing out of the CDs, they continued to earn above market yields until the CDs matured.

New game - new rules

As recently as three months ago, the game was very simple. I would tell clients an Ally Bank 5-year CD was paying 1.54 percent APY, and that the 60 day early withdrawal penalty was the equivalent of a 0.26 percent fee to close the CD early. The Vanguard Total Bond Fund ETF (BND) was also yielding about the same at 1.56 percent, but would decline by an estimated 5.50 percent with a one percentage point increase in interest rates. It was a no-brainer in my book to get virtually the same yield with far less risk.

Today, however, things are much less clear. Interest rates have ticked up a bit and BND is now yielding 2.04 percent, while Ally Bank's 5 year-CD is still yielding only 1.50 percent. So the previously free interest rate insurance is no longer free -- one must give up 0.54 percent annual yield to get this insurance.

Ken Tumin, founder of DepositAccounts.com tells me that banks typically lag bond interest rate changes. This means that when rates are declining, banks are slower to lower rates which makes their yields more attractive relative to those bonds. The opposite happens when bond rates increase as exemplified by Ally not raising its CD rates.

Why CDs can still make sense

To understand the value of insuring against the possibility of rising rates, we can compare BND to the Vanguard Short-term Bond ETF (BSV). It is yielding 0.76 percent and would decline by an estimated 2.7 percent with a one percent increase in rates. Thus, Ally Bank still pays nearly twice the yield with less interest rate risk.

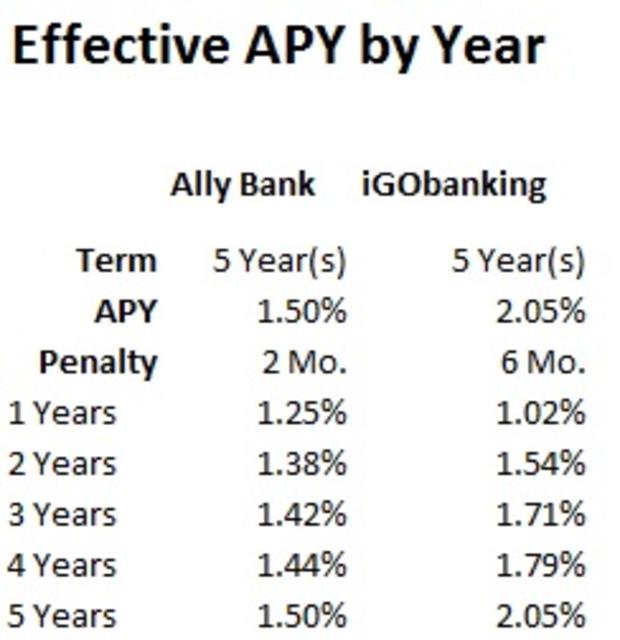

DepositAccounts.com shows the best five year CD with a reasonable early withdrawal penalty to be at iGoBanking.com. It's yielding 2.05 percent with a 180 day early withdrawal penalty. That penalty is the equivalent of about a 1.02 percent charge to get out early. Thus, it's yielding the same as the BND fund and still has far less interest rate risk, if you feel it's possible rates could increase by one percentage point.

DepositAccounts.com has a nifty calculator to compare CD yields taking into account penalties. Below is the comparison between Ally and iGOBanking. Ally Bank is superior through the first 16 months.

Unfortunately, there are fewer and fewer CDs paying rates as attractive as high quality intermediate-term bonds. And since I never recommend going above FDIC or NCUA (credit unions) insurance limits, I'm using fewer CDs and more bond funds.

If rates do continue to rise, I'll be exercising some of those easy early withdrawal penalties in my own portfolio of CDs. Whether they go into new CDs or into bond funds will depend on the CD rates relative to high quality bond funds.