Where to stash your cash to make more

Want to make an extra $10 to $100 a week -- or more -- by doing virtually nothing? That's possible if you have some significant cash at a bank or credit union paying something in the neighborhood of 0.01 percent annually.

To that end, here are two strategies to earn more with your cash.

First, a high-paying savings account may be the ticket if you want to keep your money liquid. DepositAccounts.com has been my best source of interest rates for years. As of the time of this writing, their listing of savings accounts rates showed Palladian Private Bank paying the highest rate, at 1.26 percent annually.

DepositAccounts founder Ken Tumin told me that Palladian doesn't have the same track record of other banks when it comes to paying the highest rates and that their web interface to transfer funds might not be as smooth. Tumin pointed to Sallie Mae Bank and Barclays Bank as more established leaders, with high rates and an easy way to transfer funds. Both yield 0.90 percent annually, and the Sallie Mae's offering is a money market account where you can write checks.

Now if these rates don't sound like much, consider $60,000 in cash earning 0.01 percent, versus 0.90 percent, amounts to an extra $534 a year, or $10.27 a week. More money translates into more risk-free earnings. Admittedly, if you have only $6,000 in cash, the extra $53 may not be worth your time.

The second cash-generating strategy is to find longer-term CDs that have liberal early-withdrawal penalties. The benefit of the easy early withdrawal penalty is that you can close out the CD if you find you need the money or if rates increase and you can earn more by paying the penalty and buying a new CD.

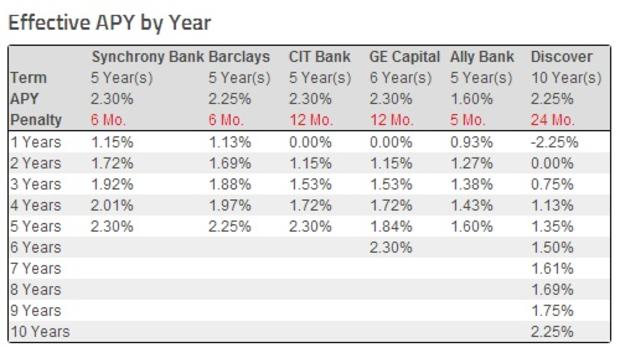

Looking at longer-term CDs using DepositAccounts.com early withdrawal penalty calculator turns up the following:

If, for example, you think you might need the money in three years, your best choices would be Synchrony Bank or Barclays Bank. After paying the penalty, you'd get an annual yield of 1.92 percent and 1.88 percent, respectively. A $60,000 CD would earn at least an extra $1,122 annually over that 0.01 percent your bank or brokerage firm might be paying you. That's not bad pay for an hour of your time.

If you have a decent amount of cash earning nothing, you have to fight inertia to pick this low-hanging fruit. Click on the links above and check out current rates, as well as any other source of higher rates, including your local newspaper. Always make sure the institution is backed by the FDIC or, if it's a credit union, the National Credit Union Administration. Never go above those insurance limits, though there are ways to get over $2 million in insurance by titling the accounts correctly.

Read the bank disclosures and make sure they don't reserve the right to retroactively change the early withdrawal penalty on an existing CD.

Do whatever it takes to start earning more risk-free. You may even want to treat yourself to something you feel is a bit extravagant, such as paying yourself a commission equivalent to the first three months interest earned.