Where have all the bears gone?

(MoneyWatch) For the first time since September, stocks are suffering their first significant bout of weakness. Blame better-than-expected economic data, which since May has been associated with market weakness because it increases the odds the Federal Reserve will pull back on their ongoing $85 billion-a-month "QE3" bond purchase stimulus.

You can see this in the latest Investors Intelligence Advisor Sentiment survey, which has just 14.4 percent of respondents feeling bearish vs. 55.7 percent feeling bullish. As a result, the ratio of bulls to bears has blown out to levels not seen since 1987 and has exceeded highs seen before the 2011 debt ceiling selloff and the late 2007 bull market top. You can see this in the way noted market bears, including Gluskin Sheff's David Rosenberg, GMO's Jeremy Grantham, and portfolio manager Hugh Hendry (who cashed in during the 2008 washout) have all switched to the bull side.

Rosenberg has been talking up what he sees as areas of strength in the economy (after pooh-poohing it for years). Grantham no longer wants to lean against the market's relentless rise "despite almost universal disappointment in economic growth." And Hendry recently admitted that he may be providing a public utility here, as the last bear to capitulate.

There are still a few out there. I've personally been warning of trouble for weeks as technical signals worsened, expectations became unrealistic, breadth narrowed, and the "smart money" as represented by professional hedgers in the equity futures market, for instance, started backing away.

You could see this in the way the percentage of NYSE stocks above their 50-day moving averages peaked at 85 percent in October but is less than 60 percent now, a sign that buyers are finding fewer and fewer stocks attractive at these valuations. That makes the market's rise vulnerable, since it relies on a narrowing base of support. Just look at how stocks like Caterpillar (CAT) and IBM (IBM) have been floundering, forcing the bulls to use parabolic rises in stocks like Bank of America (BAC) to keep the Dow Jones Industrial Average inching higher.

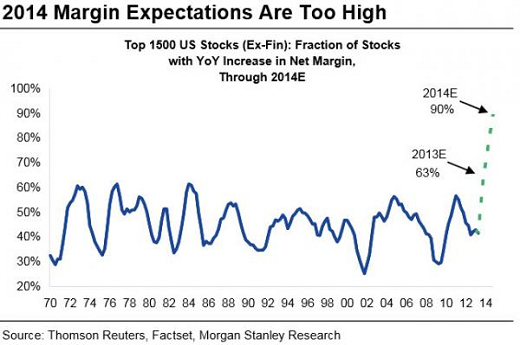

And you can also see this in the chart above, from Morgan Stanley, of how off-the-reservation expectations have become for corporate profitability. Despite the fact that GDP growth expectations are being marked down (Goldman just cut its Q4 estimate to 1.3 percent) investors are expecting an incredible 90 percent of non-financial stocks to post a year-over-year increase in profit margins vs. roughly 40 percent in 2012.

Albert Edwards at Societe Generale, who has also been steadfast in his skepticism of the market's foam-at-the-mouth enthusiasm, worries about this last point since he notes that labor costs are now rising faster than the pace companies can raise prices. This is late cycle behavior last seen in a big way back in 2007 and in 2000 before that.

In other words, if history is any guide, both on lopsided sentiment as well as the profit picture, now is the time to sell.