When hot investments go cold

One of our worst tendencies as investors is to chase "hot" stocks, sectors and asset classes. Unfortunately, the historical evidence shows that we often end up buying yesterday's winners (after their great performance has already run its course), and sell yesterday's losers (after all losses have occurred).

This causes investors to buy high and sell low -- not exactly a recipe for investment success. This behavior explains why studies show that investors actually underperform the very mutual funds they invest in by significant margins.

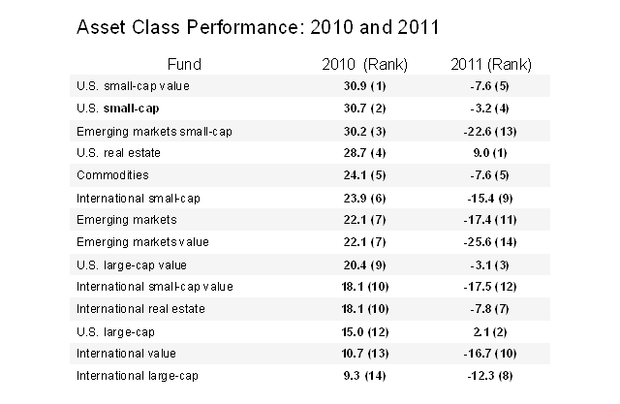

The past year gave us another great example of how hard it is to pick next year's winners. The table below compares the returns of various asset classes in 2010 and 2011. (The asset classes are represented by funds from Dimensional Fund Advisors, except commodities, which is represented by a fund from PIMCO.)

As you can see, sometimes the winners of 2010 repeated, but other times they became losers. For example, emerging-market small-cap stocks, which was the third best performing asset class of 2010, was the second worst performer in 2011. And U.S. large caps, which finished near the bottom in 2010, was the second best performer in 2011.*

Unfortunately, while there are streaks in asset class returns, they occur randomly relative to expectations. The streaks have no more meaning than streaks at the craps table -- a good or poor return in one year doesn't predict a good or poor return the next year. In fact, great returns actually lower future expected returns, and below-average returns raise future expected returns.

Thus, the prudent strategy for investors is to act like a postage stamp. The lowly postage stamp does only one thing, but it does it exceedingly well -- it adheres to its letter until it reaches its destination. Similarly, investors should adhere to their investment plan -- asset allocation. Adhering to one's plan doesn't mean just buying and holding. It means buy, hold and rebalance, which restores your portfolio's asset allocation to the plan's targeted levels.

* An earlier version used the incorrect 2011 returns for international real estate, showing a return of 1.8 percent. The table and corresponding rankings have been updated.