What's wrong with small growth stocks?

(MoneyWatch) Investors who think passive investing is the most prudent, financially rewarding strategy tend to fall into two camps. One group believes in market-cap weighting their portfolio. Their investment solution is simple -- buy the Vanguard Total Stock Market Fund (VTSMX). If you also want to own international stocks, there is the Vanguard Total International Stock Index Fund (VGTSX), which owns both developed and emerging market stocks.

The other group consists of those who believe that a "one-size-fits-all" approach isn't ideal for all investors. Depending on your financial circumstances, for example, you may prefer small or value stocks. My book, co-authored with Kevin Grogan and Tiya Lim, "The Only Guide You'll Ever Need for the Right Financial Plan," discusses who can tolerate more or less exposure to small and value stocks, international and emerging market stocks, and other asset classes, such as commodities and real estate.

That said, financial advisers who believe in using what has come to be known as a "slicing-and-dicing" approach -- offering greater or lesser exposure to various asset classes than a total stock market fund does -- often recommend avoiding small-cap growth stocks. Why?

History lesson

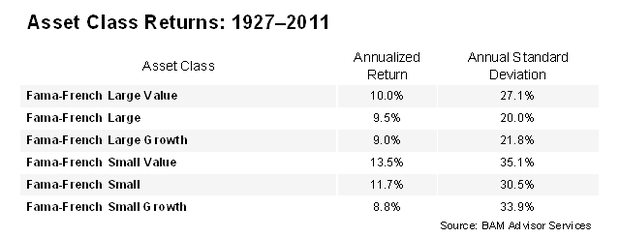

Answering that requires first reviewing the historical evidence. The following table covers the period from 1927 through 2011. It provides the annualized returns and standard deviations of each of the major domestic equity asset classes. The data is from the Fama-French indexes, which measure returns using academic definitions of asset classes. (Note that utilities have been excluded from the data.)

The data lines up as you should expect, with one exception. Riskier small-cap stocks have provided higher returns than safer large-caps, but with more volatility. Riskier large-cap value stocks have provided higher returns than large-cap growth stocks, but with greater volatility. And riskier small-cap value stocks have provided higher returns than relatively safer large-cap value stocks, again with higher volatility. The exception is that the riskier small-cap growth stocks have underperformed large growth stocks, but have experienced much greater volatility, though lower returns and less volatility than small-cap value stocks.

The fact that small-cap growth stocks have produced lower returns with higher volatility than safer large-cap growth stocks, and much lower returns than small-cap value stocks while only experiencing slightly less volatility, is why those who "slice and dice" avoid the small-cap asset class. It's also why small growth has been called the "black hole of investing." These trends also represent of the two biggest challenges to the efficient markets hypothesis, the other being momentum.

Is there an explanation for the anomaly? The field of behavioral finance provides us a likely explanation.

Playing the lottery

Individual investors have a tendency to prefer investments with "lottery-like" distributions. In technical terms, that means these investments exhibit both excess kurtosis and positive skewness. Kurtosis is the degree to which exceptional values, much larger or smaller than the average, occur more frequently (high kurtosis) or less frequently (low kurtosis) than in a normal (bell-shaped) distribution. High kurtosis results in exceptional values that are called "fat tails" -- these are the handful of investors who win the large lottery payoffs. Skewness is a measure of the asymmetry of a distribution. Positive skewness occurs when the values to the right of (more than) the mean are fewer (most people lose when they buy lottery tickets), but farther from the mean than are values to the left of the mean (in terms of percent returns, the few winners win much more than the many losers lose).

This taste, or preference, for investments with lottery-like distributions leads to them being "overvalued," at least according to traditional economic theory. However, because investors prefer that type of distribution of potential returns, for them the investment is perfectly rational. But if you don't fall into that category, you should avoid an investment that has a lottery-like distribution. For you, those investments are suboptimal. And that's why many recommend avoiding small-cap growth stocks.

There's another likely explanation for the small-cap growth anomaly. These investments tend to be high-beta stocks (meaning they are more exposed to market risk than the overall market). Institutional investors who want to increase their exposure to market risk, but are already at their maximum stock allocation under their investment policy statement, could accomplish their objective by selling low-beta stocks in their portfolio and buying high-beta stocks. This policy constraint can create a preference for high-beta stocks.

Here's one last explanation. Consider an investor who has a 100 percent allocation in the form of an investment in the VTSMX and who wants to increase her exposure to stock market risk. One way to do that would be to use leverage -- borrow money, with the portfolio value serving as collateral -- and use the proceeds to invest in stocks. However, the use of what is called "margin" creates the risk of margin calls. Investors receive a margin call -- a demand for more collateral -- from their broker-dealer when the portfolio's value falls below a specified percentage of the debt. To avoid this risk, investors prefer to increase their market exposure by purchasing high-beta stocks.

It's important to note that there are several other categories of investments besides small-cap growth stocks that exhibit lottery-like distributions. IPOs, stocks in bankruptcy and low-priced ("penny") stocks all have this attribute. So unless you prefer such investments, it seems logical to avoid them.

Limits of arbitrage

Finally, you might ask -- If these assets are overvalued, why doesn't the market arbitrage this overvaluation away? Why don't sophisticated investors short these stocks, while going long stocks that don't have these characteristics?

The basic reason is that there are limits to arbitrage. First, selling short can result in unlimited losses and margin calls. Second, in order to go short a stock, you must borrow it from another investor. The demand for borrowing these stocks is high. That means the the borrowing costs, or the fee you must pay the lender of the security, are also high. And you have the risk that the lender will demand his security back at any time (and the market can remain irrational longer than you can remain solvent). The risks and the high costs limit the ability to profit from any overvaluation.

Image courtesy of Flickr user 401K