What's up with inflation?

And old foe is making a comeback.

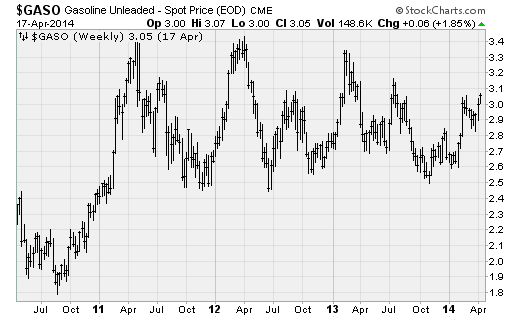

Last month, producer prices (less food and energy) increased at the fastest rate in three years. Food prices, particularly proteins like shrimp and beef, are moving higher. And gas prices are pushing back towards the heights reached only a handful of times over the last few years -- peaks that proved short-lived as consumers have repeatedly proven they just can't handle the pressure of higher energy prices.

I'm talking about inflation, which has been dormant since 2011's Arab Spring pushed up energy prices, forced the Federal Reserve to pull back on its cheap money stimulus, and caused the Consumer Price Index to swell at nearly a four percent annual rate.

Since then, price pressures have cooled. The Eurozone debt crisis dampened enthusiasm in early 2012. China's efforts to lower inflation and ease credit growth dampened it a little more. And a harsh winter here at home literally froze out consumers, pushing inflation so low for so long that Fed policymakers started highlighting it as a potential concern.

While low inflation (or even deflation, or falling prices) can be great in the right circumstances (since it can increase living standards and real purchasing power) in a heavily indebted society like ours it's dangerous. That's because consistent and steady inflation helps reduce the real burdens of debt. Your fixed principal mortgage will steadily erode away over time as the general price level and your wages rise.

The nightmare debt-deflation dynamic, where falling prices and lower wages increase the real cost of debt, is the reason the Japanese economy has been hamstrung for decades.

That's why, in recent comments, the Fed has pledged to hold short-term interest rates near zero percent until inflation drifts back towards their two percent target level. Currently, the Fed's preferred measure of inflation stands at just 1.1 percent.

This Goldilocks scenario of low inflation, modest growth, and aggressive Fed stimulus has been a perfect recipe for the stock market. And the bulls have been excited by the prospect of a continuing pattern of low inflation well into 2015. But evidence is building that inflation could hit sooner rather than later, putting the market's cheap money junkies on notice.

Producer prices are pushing higher, suggesting inflation is building deep within the supply chain. The year-over-year inflation rate increased to 1.4 percent in March from 0.9 percent the previous month. Paul Dales, senior U.S. economist at Capital Economics, believes this "could mark the start of a gradual upward trend that would eventually filter through into higher consumer price inflation."

The team at Capital Economics expects the upward pressure to continue as the full effects of severe weather feed through into food prices -- including both the winter weather we've suffered as well as the severe drought underway in California.

Inflationary pressures are also coming from higher rents and higher medical costs.

The wild card is what happens with wages. Fed Chair Janet Yellen has consistently repeated her belief that the job market is weaker than many believe, based on measures such as long-term unemployment. And thus, she believes that wage inflation -- which would truly unleash inflationary pressures across the economy -- is not forthcoming.

But new research suggests this belief could be mistaken. Research by economists including Robert Gordon of Northwestern University and Mark Watson of Princeton find that the short-term unemployment rate could be a much better predictor of the amount of slack in the job market. When it's low, as it is now, then wage pressures can quickly follow.

The rationale is that the long-term unemployed are increasingly discriminated against in the labor market. So employers view then as essentially being out of the available work force, reducing the supply of labor and creating competition for skilled workers.

Overall, Robert Gordon estimates that if the Fed should try to push the unemployment rate, which stands at 6.7 percent, towards 5.0 percent over the next five years it will push inflation to as high as 3.8 percent. Instead, Gordon recommends that Fed should continue pulling back on the stimulus to keep inflation under control.

So there you have it. After a long slumber inflation is coming back to life.

And that's a good thing, in that it indicates some reacceleration in the economy, reflects the potential for some increase in wages, and keeps the debt-deflation scenario at bay.

But if the Fed pushes too hard, and causes prices to rise so much that it starts damaging the economy, we could face a painful future of higher prices, higher interest rates, and a slowing economy amid a stock market suffering from stimulus withdrawals. No one said managing the economy was easy.

Anthony Mirhaydari is founder of the Edge and Edge Pro investment advisory newsletters, as well as Mirhaydari Capital Management, a registered investment advisory firm.