What's taking the steam out of Wall Street's rally

Heading into the three-day Easter holiday weekend on Wall Street, U.S. equities bounced back from early losses on Thursday to finish nearly unchanged.

News flow was light as attention remains focused on recent hawkish comments from Federal Reserve officials and renewed weakness in crude oil on a lack of progress toward an OPEC-Russia supply freeze amid rising Iranian output, a slowdown in global demand growth and swelling inventories.

Other factors in play include ongoing weakness in corporate profitability, a downturn in GDP growth expectations and narrowing market breadth as buyers find fewer stocks attractive at current levels.

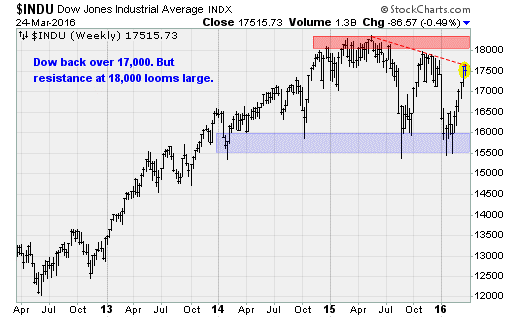

Indeed, large-cap stocks are contending with major overhead resistance levels near 18,000 on the Dow Jones industrials index, so a bout of market weakness looks likely in the days to come. It's possible the Dow will return to support near the 16,000 level.

After last week's "dovish hold" policy decision by the Fed -- which cut in half the number of expected rate hikes this year to just two -- the chatter has turned in the other direction. A number of policymakers are talking up the odds of an April rate hike even though Wall Street didn't expect action until June at the earliest. Not only has that dampened stock prices, it's contributing to the energy pullback by strengthening the dollar in a way that hasn't been seen since the start of the greenback's October-December rally.

St. Louis Fed President James Bullard made the case for the April rate hike earlier this week after commenting that inflation is likely to soon overshoot the Fed's 2 percent target. He added that the unemployment rate, currently at an eight-year low of 4.9 percent, would likely fall to 4.5 percent later this year.

The change in tone has been so severe that CNBC wondered aloud whether Fed Chair Janet Yellen's leadership is under threat.

Turning to earnings, the first-quarter 2016 reporting season will kick off on April 11 when Alcoa (AA) report. Currently, analysts expect an 8.4 percent year-over-year decline in S&P 500 earnings according to FactSet data. That would represent four consecutive quarters of declining profitability for the first time since the recession ended.

Finally, on a technical basis, the Dow remains in the grips of an epic topping pattern going back to 2014 bordered by 18,000 on the high side and the 15,500 level on the low end (chart above). The pattern has been driven by a topping of forward earnings expectations in the autumn of 2014. Since then, rallies have been led in large part by surges in GDP growth expectations in the hopes that faster economic growth would reinvigorate corporate revenue growth.

Unfortunately, GDP growth expectations are falling away again. On Thursday, the February durable goods orders report showed a drop of 2.8 percent month-over-month, while core orders fell 1.8 percent, much worse than expectations for a 0.5 percent decline. As a result, the Atlanta Fed downgraded its first-quarter GDPNow forecast to just 1.4 percent from 1.9 percent previously.

Given all this, it's no wonder that buyers are backing away from stocks. The 20-day moving average of NYSE net advancing issues peaked near 900 earlier this month before rolling over as fewer and fewer stocks participate to the upside. On Thursday, the measure fell below the 500 mark.

Ominously, a similar pattern was seen as stocks topped back in November ahead of a four-month downtrend.