What's fueling volatility on Wall Street

Investors are feeling seasick this week as the stock market whipsaws up and down violently.

At the end of September, the NYSE Composite Index closed below its 200-day moving average for the first time since 2012, stoking fears that the smooth and easy two-year-old uptrend was coming to an end. Then, miraculously, a rebound materialized. Then, another triple-digit decline came on Tuesday, followed by Wednesday's huge intraday bounce -- the largest since 2011.

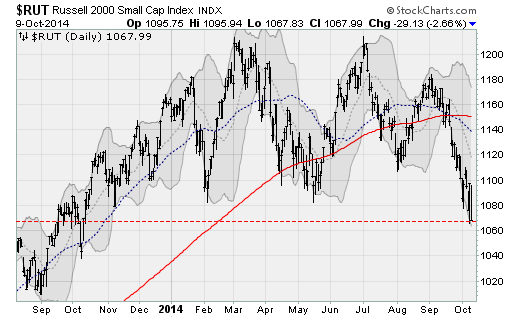

But on Thursday, it was all washed away as the NYSE Composite dropped another 2.2 percent to return to levels last seen in April. Smaller stocks are in worse shape: The Russell 2000 is down 8.2% for the year-to-date and has returned to year-ago levels.

The impetus for the sell-off has been discontent with central bank stimulus and growing realization that the global economy is stalling hard.

On the first point, investors are slowly realizing that the Federal Reserve's "QE3" bond-buying program -- which has been bolstering the stock market since 2012 -- will end in three weeks. During the current bull market, the periods during which the Fed wasn't buying bonds (such as in 2010 and 2011) were periods associated with dramatic market pullbacks.

While the bulls point to the Fed's insistence that short-term interest rates will remain near zero percent, the 2010 and 2011 sell-offs also occurred in an environment of zero percent interest rates.

In fact, one way to measure market volatility is to look at the average range or the distance prices are covering in the day's trade. One measure of this has ballooned out to levels not recorded since the August 2011 market wipeout associated with the loss of America's AAA credit rating. So, the parallel is apt.

Moreover, the U.S. job market is rapidly tightening (the unemployment rate now stands at 5.9 percent), which means the Fed will be hard pressed to justify restarting its bond buying should the market melt lower.

It's also worth noting that it's not just discontent with the Fed but with central banks around the world.

On Thursday, some of the disappointment came from Europe where the head of the European Central Bank downplayed the need for its own program of buying government debt (something the ECB has been resisting because it might, in fact, be illegal according to its charter). Japan seems to be at the limit of what its bond-buying program can do. And it's apparent that China's efforts to boost its economy with cheap money is losing its efficacy and worsening a possible credit bubble there.

The second impetus for the sell-off has been deterioration in the global economy. Germany has been the focal point this week, on terrible industrial production (weakest result since the the recession in early 2009) and export data. As a result, Germany has joined with Japan as being among the world's largest economies that very well could already be in recession. Japan's economy contracted outright last quarter on a recent sales tax increase, and another tax hike is on the table (required because of Japan's massive government debt load).

Combined with a deepening slowdown in China where electric power generation is falling for the first time since 2009 (and, therefore, industrial output as well), it adds up to a grim outlook.

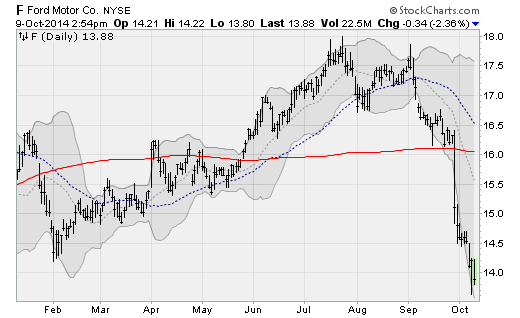

Should all this continue, corporate profits will come under pressure as well. Ford (F) was slammed lower this week on a warning that weakness overseas will pinch results. Even the Fed has acknowledged that one of the consequences of the relative strength of the U.S. economy vs. global peers -- the recent strength of the U.S. dollar -- could have negative consequences, including a lowering of corporate profitability as U.S. exports get more expensive in a world economy that's struggling.

Already, on one measure, corporate profits are already sliding at a pace not reached since the recession.

At the end of the day, the cornerstones of this bull market -- Fed stimulus, foreign economic strength and corporate profits -- are all in jeopardy. And that means the turbulence hitting the stock market could very well continue through the end of the year and into 2015.