What to look for at this week's Fed meeting

Talk about being emotionally volatile. Investors have been all over the place lately as worries about oil prices and stalled economic growth mix with fears over both negative interest rates (in Europe and Japan) and higher interest rates (here at home).

And it's about to get worse with the Federal Reserve meeting this week on March 15 and 16.

It's enough to make you reach for the antacid just thinking about it.

There was certainly plenty of angst on Thursday following the aggressive new stimulus push by the European Central Bank, which included an interest rate cut, an expansion of its bond-buying program (both in terms of purchase pace and in terms of what the ECB is buying) and a new bank lending program. Policy makers are pretty much throwing the kitchen sink at the eurozone's stagnant growth.

Still, investors were taken aback by comments from ECB chief Mario Draghi that the central bank wasn't likely to cut interest rates again given concerns over structural issues with negative interest rates. That fueled fears that monetary policy stimulus is both reaching its limit and has become ineffective.

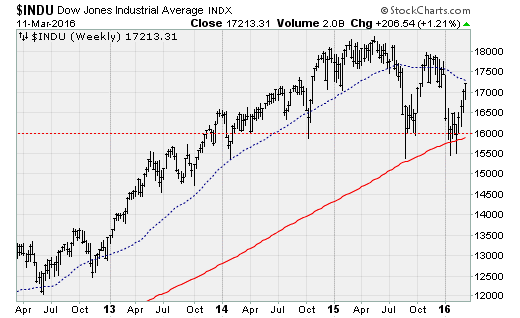

Yet on Friday, investors apparently reevaluated the package and decided the shift away from negative rates (which are bad for bank earnings) and an embrace of unconventional tools (so-called "helicopter" money was even discussed at Draghi's press conference) were good things. In the end, the Dow Jones industrials index gained 1.3 percent on Friday to cross its 200-day moving average for the first time since December (chart below).

What will the Fed's decision bring?

Looking ahead, all eyes are on the Fed's Summary of Economic Projections, or "dot plot," update. The consensus is that despite a recent rise in core inflation -- driven by rental rates -- Fed officials are likely to wait until June to hike rates again as wage growth for American workers remains tepid.

In December, the Fed revealed an expectation for four quarter-point hikes in 2016, whereas the futures market expects only a single hike.

Moving their official forecast nearer to where the market is would do much to boost stock prices on expectations of an earnings rebound -- because a more dovish Fed is bearish for the dollar (which is good for foreign earnings) and bullish for commodities (because of economic growth expectations, inflation expectations and currency effects from a weaker dollar).

This is far from a slam dunk, however, with ongoing labor market tightening and evidence of rebounding core inflation giving plenty of justification and rhetorical ammunition to the policy hawks at the Fed eyeing a 2 percent inflation target.

Indeed, Bank of America Merrill Lynch economists see the core consumer price index inflation rate -- excluding food and fuel -- to hit 2.2 percent at the end of the year, while the Fed's preferred inflation measure -- the core personal consumption expenditures deflator -- hits 1.7 percent.

A number of important economic data points are also on deck, including February retail sales and an update on the inflation rate. We'll also see the latest Job Opening and Labor Turnover Survey data, which is well known as one of Fed Chair Janet Yellen's favorite reads on the job market.

So, while the Dow was able to cross the 200-day moving average on Friday, it's still contending with downtrend resistance from a two-year "topping pattern." The bulls aren't running in the clear just yet.

And with the Fed's policy path far from settled, expect the nervous and volatile trading environment to continue -- potentially resulting in another test of critical support down near the Dow's 16,000 level.