What low interest rates mean for stocks

(MoneyWatch) Federal Reserve Chairman Ben Bernanke emphasized Tuesday in Senate testimony that low interest rates are here to stay for the foreseeable future. Many investors are concerned about how such a current low interest rate environment affects their bond holdings. As if they needed something else to worry about, a recent paper states that such an environment may also provide a drag on stock returns.

- How to invest with interest rates so low

- Is the gold rally over?

- Who are the most (least) accurate stock gurus?

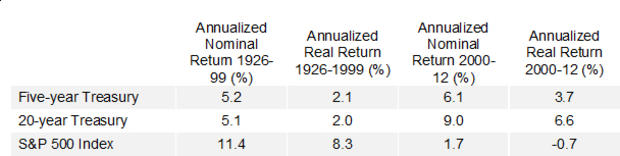

The table below shows that bonds have outperformed stocks since 2000, in sharp contrast to the 74 years before the start of the period.

The important issue raised by such data is that you have to be very careful about projecting historical returns into the future. For example, the strong bond returns for the past 13 years are a result of the sharp drop in interest rates. Today, we have both nominal and real bond yields at the lowest rates in at least 50 years. Since the best predictor of future bond returns are current yields to maturity, it's foolhardy (and costly) to extrapolate the returns of the last 13 years into the future.

When it comes to stocks, valuations also matter. It was foolish in 1999 to continue to project the 11.4 percent returns of the S&P 500 into the future. The reason was that a significant part of that return was due to the price-to-earnings (P/E) ratio ending the period at about twice its historical average. With the P/E ratio at about 30, future stock returns were virtually doomed to be well below their historical average even if the P/E didn't revert to its historical mean -- which in fact it did.

The "Triumph of the Optimists" authors Elroy Dimson, Paul Marsh and Mike Staunton, looked at whether today's low level of real interest rates tells us anything about future returns. They surmised that since the expected return to stocks is composed of the rate of return on the risk-free asset (one-month Treasury bills) plus a risk premium, if the risk-free rate has fallen, it follows that "other things equal, a low real interest rate world is also a lower-return world for equities." This would be pretty significant, given that the risk-free rate is now effectively zero.

To investigate whether history supports this theory, they examined the data from 20 countries covering 113 years. They found that "there is a clear relationship between the current real interest rate and subsequent real returns for both equities and bonds." Specifically, they concluded that investors should expect a stock premium (relative to one-month Treasury bills) of around 3 percent to 3.5 percent on a geometric (annualized) basis and, by implication, an arithmetic mean (annual average) premium for the world index of approximately 4.5 percent to 5 percent.

AQR Capital co-founder Cliff Asness provided further support to the idea that expected stock returns are now much lower than the historical average. Asness reviewed the historical data using what is called the Shiller PE 10 (using 10-year average real earnings) and found that when it was between 18.9 and 21.1, the following 10-year real return averaged 3.9 percent. It's now a bit over 23. All of this data helps show that the risk premium for investing in stocks isn't constant. It can change over time.

Real bond returns are almost certainly going to be very low (if not negative). And if Dimson, Marsh and Staunton are right about future stock returns, they too will be well below their historical average. While no one has a perfectly clear crystal ball as to future returns, it does appear that many investors are making unrealistic assumptions about future returns. While the average expected return for pension plans has fallen from 9.1 percent a decade ago, it's still 7.6 percent. Given current bond yields, these plans must achieve stock returns of about 12 percent in nominal terms, or about 10 percent in real terms given expected inflation of 2.3 percent.

As the authors note, "optimistic estimates of future returns are dangerous, not only because they mislead, but also because they can mask the need for remedial action." Does your plan have realistic expectations of future returns? Does it at least incorporate the possibility that returns could be below historical averages? Does it should also contain the steps you will take if that turns out to be the case? If the answers to any of them are no, it's time to revisit your plan.

Image courtesy of Flickr user Tax Credits.