What could come after the rate-hike rally

Wall Street's response on Wednesday to the first Federal Reserve interest rate hike in nearly a decade was a bit anticlimactic. And something of a letdown after all the buildup in recent times about the looming end of the near-zero interest rate policy that has been in place since 2008.

Alas, the 0.25 percent increase in the federal funds rate lifted stocks, boosted gold and left the dollar unchanged. Crude dropped on inventory worries. And high-yield, aka "junk bonds" -- the site of some consternation last week -- continued a relief rebound.

Investors were apparently pleased with the Fed's commitment to a "gradual" pace of subsequent rate hikes. But this on-the-surface analysis misses a number of important details suggesting recent market volatility could well continue, such as the fact that it's an options expiration day on Friday. The true reaction to the start of the first policy tightening campaign since 2006 may not be so benign.

Stocks remain vulnerable in the near term because measures of breadth remain extremely weak. That's a sign investors are focusing on a narrow list of popular momentum trades such as Netflix (NFLX), indicative of limited buying demand. In fact, with large-caps trading roughly where they were in late October, just 56 percent of the stocks in the S&P 500 are in uptrends now vs. more than 72 percent in early November.

As for the bond market, we'll know more on Friday morning. That's when Societe Generale economist Aneta Markowska noted that the nuts and bolts of the Fed's policy change will first start hitting the cost of overnight, interbank lending. Keep an eye on those high-yield corporate issues.

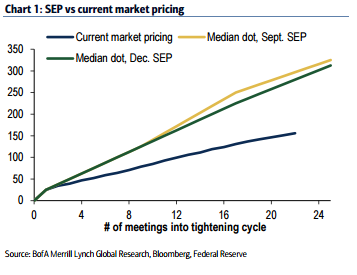

Bank of America Merrill Lynch analysts suggest the outcome of the Fed announcement wasn't as dovish as many had hoped because the futures market continues to expect only two rate hikes next year. Already, the Fed's expectation for four rate hikes next year is just half of the average tightening pace of the last three tightening cycles. The more this hawkish outlook is reinforced by steady job gains and an upward progress in inflation, the more high-yield bonds and equities will come under pressure.

Investors have been pleased with rebounds in oil and junk bonds this week. But both are vulnerable to renewed downward trends in response to the Fed's actions on Wednesday. Oil will feel the dampening effect higher rates will have on economic growth and the lift it will give to the dollar (in which oil is priced). Bonds will feel the negative impact weaker energy prices and a stronger dollar will have on corporate earnings growth.

As the calendar flips into 2016, Alberto Gallo at RBS worries that the Fed will have a tough time living up to its four-hike forecast amid monetary policy divergences with the likes of the Bank of Japan and the European Central Bank and the currency and bond market volatility that's likely to result.

Ultimately, Societe Generale's Markowska is looking for just three rate hikes next year, a more aggressive pace in 2017 and the end of the economic expansion in 2018 or so. By then, interest rates should be running upwards of 3 percent. The next recession will likely see the Fed cut back to zero percent, in her view.