Wall Street's record rally has its skeptics

U.S. large-cap stocks finally broke their winning streak on Thursday, but not until after hitting new highs again on Wednesday. That capped the ninth-straight daily gain for the Dow Jones industrials and the 14th in 16 sessions. It was the longest winning streak since 2013, fueled by nonspecific hints out of Britain and Japan of more cheap money stimulus.

Still, even with Thursday's pullback, disbelief reigns. Many Wall Street pros are nervous and are holding large cash positions.

They fear "dumb money" is fueling the rally, assisted by aggressive short covering (traders who bet on shares falling being forced to buy borrowed shares) and the steady bid of companies repurchasing their own stock. But that disbelief could be just the thing to create a nice buying opportunity for investors waiting to jump in ahead of further gains.

I can't say I blame the skeptics. The stock market's obsession with monetary morphine looks increasingly dangerous. All other catalysts, from weak corporate earnings to eye-watering stock valuations and the fact that the market rebound has in fact made fresh central bank easing increasingly unlikely, doesn't seem to matter.

Nor has narrowing breadth: As the market has climbed to new records, it has been doing so on the back of fewer and fewer stocks. In fact, more stocks were rising when Wall Street were topping back in April than there are now. Very odd.

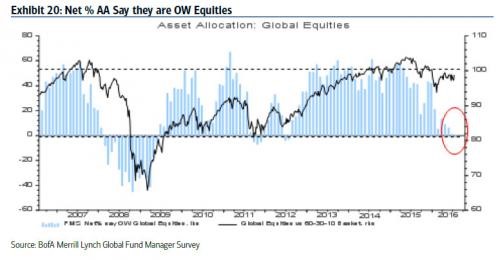

The latest Bank of America Merrill Lynch Fund Managers' Survey finds that July cash levels are at 5.8 percent, up from 5.7 in June, to the highest level since November 2001. Many survey respondents are also taking out protection against a sharp decline in stocks, with more worries about a downside surprise than in late 2008 in the midst of the financial crisis.

The result of all this is the first industry equity underweight positioning in four years (chart above).

Jason Goepfert at SentimenTrader uses his own measure of "Dumb Money vs. Smart Money" sentiment -- which compares indicators such as commercial hedging positions in equity index futures to small speculators in equity futures -- to see how the big guys are feeling compared to the small fry.

Through Tuesday, the dumb money is 76 percent confident in the rally, while the smart money's confidence is at only 18 percent. Historically, gaps as large as this have been a bad sign for stocks: Every time in the last 20 years, further short-term stock market gains were erased during the subsequent pullback.

Any such pullback could be a buying opportunity, however, before the skeptics on Wall Street are forced to buy into a market that's leaving them behind.

Goepfert highlights that the S&P 500 has been above its five-day moving average for three weeks, an incredible show of persistent buying strength. In the past, this has presaged some impressive medium-term gains. Since 1928, there have been 15 other melt-ups to new highs similar to the current situation. The average return one year later was 12.7 percent vs. an 8.1 percent gain for any random day.

The most likely area of interest, based on recent underperformance (and thus, presenting a modicum of value): Bank stocks.