Wall Street fears a run on junk bonds -- and worse

Fasten your seat belts, investors. We may be in for a bumpy ride.

Large-cap U.S. stocks suffered their worst one-day loss since September last Friday as many popular big-tech stocks -- such as Amazon (AMZN) and Facebook (FB) -- rolled over. And it looks like the stock market's bears are about to run amok with the Dow Jones industrial index back below its 200-day and 50-day moving averages, falling into a confirmed downtrend for the first time since August.

Tremors also are being felt across credit, commodity and currency markets, as the Federal Reserve decides on Wednesday whether to raise interest rates for the first time in nearly a decade. Corporate profits are under pressure. Crude oil has already returned to its 2008 and 2009 financial panic lows, with no support in sight.

And now, bond funds are being hit in a way that reminds many of the mortgage-backed troubles of early 2007 as the housing blowup was starting. To cut to the quick: Regular investors should use this time to reevaluate their risk exposures, consider trimming where necessary and prepare for a potential rough patch in the stock market through the end of the year and into 2016.

We had a preview of sorts back in August, when stocks suffered their most violent pullback since the Washington debt-ceiling standoff of 2011. The summertime catalyst was currency and bond market volatility, mainly out of China and primarily related to fears surrounding the implications of the Fed raising interest rates.

Share prices rebounded but have been unable to push the Dow back over the 18,000 mark to new highs. Breadth, or the number of companies whose shares are participating in any upswing, has also been weak. All of this, along with evidence of stock market outflows and what's set to be the third consecutive quarter of negative S&P 500 earnings growth, is a big red flag that trouble is coming.

Because while the Fed is widely expected to raise interest rates from near zero to just 0.25 percent, this seemingly small policy change is likely to have wide ramifications across global markets. Never before has the Fed waited this long into a business cycle to start tightening monetary policy. Never before have interest rates been held this low for this long.

And the last time the Fed prematurely raised interest rates amid competing signs of economic vulnerability -- such as waning U.S. manufacturing activity -- was the policy mistake of 1936 that prolonged the Great Depression.

So many cross linkages now exist between interest rates, credit markets, commodities, currencies, global fund flows and U.S. stocks, no article of this length can cover them all. Perhaps it's easier to just imagine a house of cards, delicately balanced, and overly reliant on the continued flow of cheap dollars from the Fed. The removal of one support threatens to bring the whole thing down.

For instance, the Bank of International Settlements recently warned that the global debt binge of recent years is at risk of higher rates from the Fed because it will push up overall worldwide interest rates and threaten the record $9.6 trillion in offshore borrowings in U.S. dollars. Of this, $3 trillion has gone to emerging market economies that are already reeling from the collapse in commodities prices related to the slowdown in China and the oil price war pitting OPEC against U.S. shale producers.

Any strengthening in the dollar coinciding with a Fed rate hike (because of relative policy tightness compared to the Bank of Japan and the European Central Bank) will further add to the cost of servicing this debt.

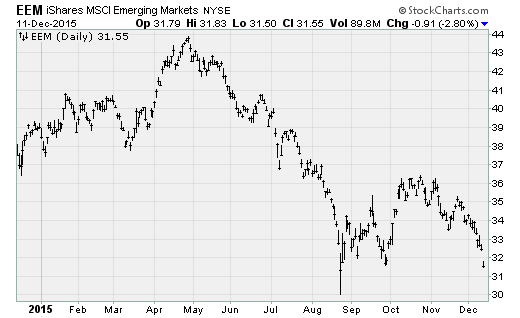

No wonder then that the iShares Emerging Markets (EEM) fund -- an exchange-traded fund that tracks the performance of emerging markets equities -- is testing its August closing low (chart above). It's down nearly 30 percent from the high hit in the summer of 2014 (when energy prices also peaked, by the way). A break below the August low would violate the EEM's entire post-recession trading range and set up a test of the 2008 and 2009 financial crisis lows.

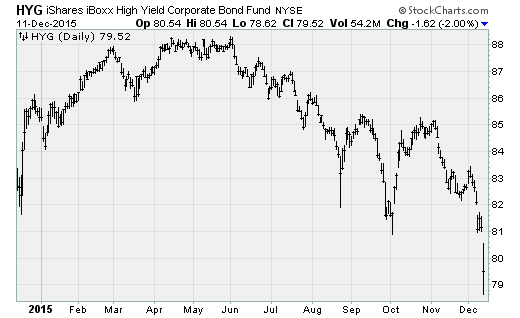

U.S. corporate bonds are also under pressure. Last Friday, the iShares High Yield Corporate Bond Fund (HYG) fell to levels not seen since 2013 and suffered a 3.8 percent decline for the week (chart above), its worst performance since 2011. This came after Third Avenue Management's junk-bond fund barred investor withdrawals while it liquidates -- attracting attention to the long simmering problem of ultralow trading volumes in many areas of the corporate bond market after years of near-zero interest rates from the Fed.

Stone Lion Capital, a distressed debt fund with approximately $1.3 billion under management, also announced it would be suspending redemptions after receiving a flood of client fund-return requests following investment losses.

High-yield bonds are being hit by the anticipation of rising interest rates from the Fed (which will hurt bond prices because of the inverse relationship between price and yield, with falling prices pushing yields higher). Also squeezing junk bonds are the impacts a stronger dollar and low commodity prices are having on corporate earnings growth. Corporate default rates are expected to rise.

In fact, speculative-grade bond prices have fallen so far that yields hit 17.24 percent on Friday -- up two percentage points over the last two weeks -- returning to levels last seen just before the weekend Lehman Brothers filed for bankruptcy in September 2008.

It's possible that the Fed delivers a shock and holds off on a rate hike this week. In which case, many of these negative dynamics could turn around. So, it's worth remembering that the Fed surprised many when it held off on any rate hike at its Sept. 17 policy announcement, during which it was revealed that at least one Fed policymaker believes interest rates will need to fall into negative territory next year. Investors were spooked then by the Fed's apparent lack of confidence in the economy.

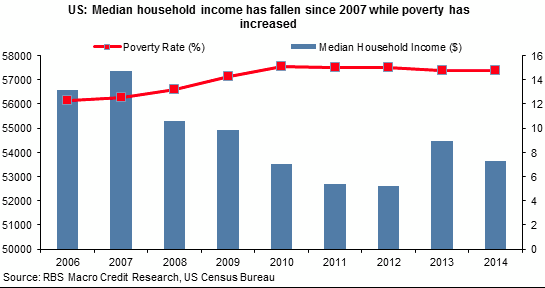

But it also indicates that with household incomes lower now than in 2007 amid a higher poverty rate (chart above), maybe all these years of ultracheap money from the Fed has been for naught. Perhaps it has merely enriched the investor class while creating financial instability and sowing the seeds of the next financial crisis.