U.S. stocks swoon for fourth day as commodities hit

U.S. stocks on Friday fell for a fourth day in what panned into the worst week for the Dow Jones Industrial Average (DJI) since January.

There were a number of catalysts in play, including weak manufacturing data out of Europe and China, along with ongoing losses in crude oil, which dropped into a bear market this week, down more than 20 percent off highs hit in early May to near $48 a barrel. Domestic data also weighed, with new home sales declining for a third month.

But the biggie was the accidental release of Federal Reserve staff projections prepared for the June 16-17 policy meeting showing policymakers have penciled in a single rate hike for 2015 in September. The release was a mixed bag for investors, as the Fed's Summary of Economic Projections -- or the "dot plot" -- still suggest two rate hikes this year.

Yet a September liftoff is well ahead of where the market is, so the takeaway was considered hawkish especially in light of projections showing inflation will remain below the Fed's two percent target through 2020.

Investors also fretted weak second-quarter revenue growth and falling industrial commodities.

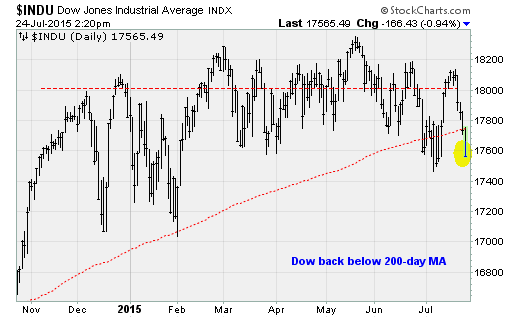

The Dow industrials fell back below its 200-day moving average -- a critical measure of medium-term trend strength -- off 600 points from Monday's highs as the euphoria over Greece reaching an accord with its creditors fades.

There were a few bright spots among corporate results, including a big surprise beat by Amazon (AMZN). But the losses stung harder, with Apple (AAPL) reporting underwhelming iPhone sales and IBM (IBM) reporting revenue below estimates. McDonald's (MCD) reported another comparable-store sales drop and Caterpillar (CAT) tallied a 13 percent drop in revenues.

In China, a private gauge of manufacturing activity slid to 48.2 from 49.4, indicating a fifth monthly contraction. In Europe, new business activity expanded at its slowest pace in five months as manufacturing growth slowed.

In the week ahead, the Fed on Wednesday wraps up a two-day policy meeting before its September gathering, while the Bureau of Economic Analysis is scheduled to release its estimate of second-quarter economy growth on Thursday. Deutsche Bank economists project GDP growth of 2.5 percent in the most recent quarter and a 3 percent rise in real consumption versus a 0.2 percent contraction in the first quarter.

The BEA will also release its annual revision to the GDP time series with possible seasonal adjustments to persistently weak first-quarter results expected.

Second-quarter earnings on tap include scheduled reports from UPS (UPS), Ford Motor (F) and Exxon Mobil (XOM).

The reports come with stocks at risk of returning to their January lows.