This group loses big under GOP Social Security plan

How to tackle the Social Security funding gap is the subject of renewed attention now that the GOP has made an official proposal. According to a bill recently introduced by House Ways and Means Social Security Subcommittee Chairman Sam Johnson, R-Texas, the retirement benefits program’s yawning deficit would be eliminated by large benefit reductions accompanied by tax cuts on affluent retirees, but with no rise in revenue to the system through tax increases.

The most significant benefit reductions include restructuring the formula that calculates the monthly benefit, increasing the retirement age and reining in cost-of-living adjustments (COLAs) for current retirees. The proposed benefit reductions would be phased in gradually, hitting the youngest workers the hardest compared to older workers who are approaching their retirement date.

And that raises a key question for those younger workers, in particular millennials: How much could they lose under this GOP proposal?

As a group, they could see an estimated 25 percent benefit reduction, compared to an estimated 21 percent across-the-board cut in 2034 if the system isn’t reformed by then. That means millennials could be worse off under the GOP proposal compared to if the Social Security trust fund were simply allowed to be exhausted and benefits were reduced across-the-board.

Keep in mind that the estimated 25 percent benefit cut is a rough average, and the reduction for some millennials could be larger than 25 percent, while it could be less for others.

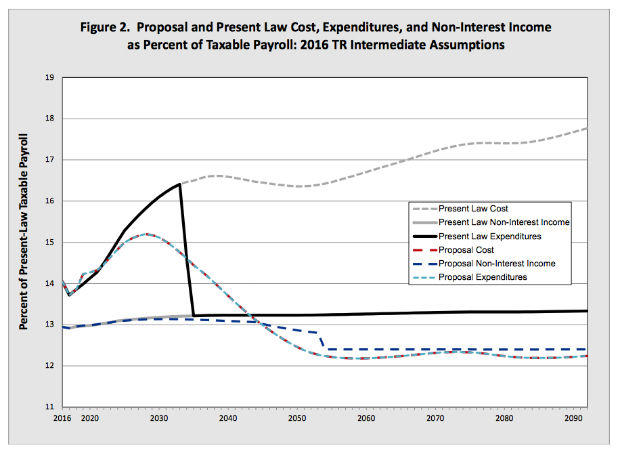

The graph below illustrates these results by projecting benefits paid by Social Security and revenue paid into the system from taxes and other sources. Social Security’s Office of the Actuary prepared this graph as part of its analysis of the GOP proposals. When looking at this graph, keep in mind that the vertical axis -- benefits paid and revenue as a percent of payroll -- does not start at zero. As a result, the visual distance between the various lines and the horizontal axis is not to scale.

Here’s an explanation of the lines in this graph:

- The top dotted line projects benefits paid from Social Security if no changes are made to the system and if benefits aren’t reduced in 2034 when the Social Security trust fund is projected to be exhausted.

- The solid black line projects benefits paid if the across-the-board reductions take place in 2034. Note that after 2034, this solid black line also represents revenues paid into the system under the current law.

- The dotted dark blue line (second from the bottom after 2050) represents revenue into the system under the GOP proposals. This line shows that projected revenue under the GOP proposals is lower than the projected revenue under current law, because the GOP proposal includes income tax reductions on affluent retirees.

- The red and light blue dotted line (bottom line after 2050) projects benefits paid under the GOP proposals. This line illustrates that estimated benefits after roughly 2045 are lower under the GOP proposal compared to projected benefits under current law after the projected across-the-board reduction (shown by the solid black line).

Why are millennials’ projected benefits under the GOP proposal lower than projected benefits after an across-the-board reduction under the current law? To keep the system solvent, the GOP’s benefit cut for millennials helps pay for the income tax reduction for affluent retirees and helps pay for phasing in benefit reductions for older workers instead of abruptly decreasing their benefits.

Of course, the GOP’s proposals may not be enacted or could be significantly altered. And Congress could enact other methods of eliminating Social Security’s funding gap, the most notable of which increases Social Security taxes by raising the wage base.

If the current Republican plan were to become law, how much would millennials need to save to make up for their slashed benefits?

Retired actuary Ken Steiner recently prepared one example for a 30-year-old unmarried woman, who currently plans to retire at age 69 and is targeting a retirement income equal to 75 percent of her preretirement salary.

Steiner estimated she could reach her goal if she saves 8 percent of her pay, assuming that she receives Social Security benefits under the current law and that she realizes all the assumptions made for her calculations. But to make up for the benefit reductions under the GOP proposal, Steiner figured she would need to increase her savings by 50 percent, raising her set aside from 8 percent of her pay to 12 percent.

The increases in needed savings would be much higher if she needs to retire before age 69, either due to a layoff or reduction in hours.

Clearly, Americans of all ages will want to carefully follow the debate on methods to address Social Security’s funding challenges.