Fed optimism could cost the economy dearly

Is the Fed overoptimistic about where the economy is headed? If so, that could cause the central bank to raise interest rates too soon, a policy error that could leave the economy stuck in a "deflationary trap" and remain at subpar growth levels for an extended time period.

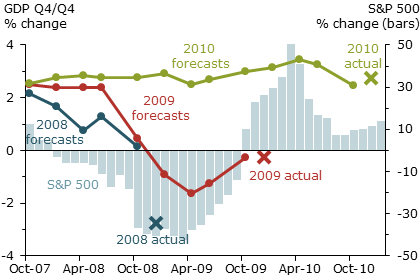

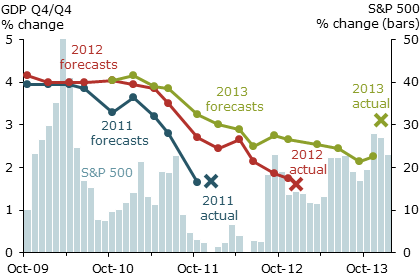

The answer to that question is yes. The Fed's tendency to be overly optimistic about the economy is documented in a recent Economic Letter from the San Francisco Fed. In the Economic Letter, Kevin Lansing and Benjamin Pyle note that the Fed's economic forecasts "(1) did not anticipate the Great Recession that started in December 2007, (2) underestimated the severity of the downturn once it began, and (3) consistently overpredicted the speed of the recovery..."

The following two charts presented along with the researchers' findings show how far off the Fed's projections for the economy have been:

This had consequences. Although the central bank's monetary policy was much better than Washington's fiscal policy, the "green shoots" the Fed saw around every corner often caused policymakers to be too slow to put new policy in place (e.g. to turn from interest rate policy to quantitative easing, and then to new rounds of quantitative easing), and to be less aggressive than needed.

As forecasts were revised over time the Fed eventually did better, though many observers don't believe the Fed was aggressive enough at any stage.

The risk now is that the Fed will repeat these mistakes. There's a long time lag between when the Fed changes interest rate policy and its impact on the economy, so the Fed must rely on forecasts of future inflation and economic growth when setting policy.

If the Fed is overly optimistic yet again -- as it has been throughout the Great Recession and subsequent recovery -- and if it fails to recognize its tendency to wear rose-colored glasses, it could raise interest rates too soon. That would slow the recovery and perhaps even create a stall as the economy gets caught in a deflationary spiral.

Why has the Fed been too optimistic? The researchers find that "Overall, the evidence raises doubts about the theory of 'rational expectations.' This theory, which is the dominant paradigm in macroeconomics, assumes that peoples' forecasts exhibit no systematic bias towards optimism or pessimism. Allowing for departures from rational expectations in economic models would be a way to more accurately capture features of real-world behavior."

This research is a sign that perhaps the Fed is finally learning its lesson. Inflation has not been a problem, in fact it's far below target, and economic growth has not lived up to the Fed's expectations in the past.

The question is whether the Fed will believe its forecasts this time and begin raising interest rates later this year, or whether it will recognize past errors and be more cautious. The risk of taking a cautious, patient approach is that inflation may be elevated for short period of time. The risk of raising rates too soon is that it could slow the economy for years.

Thus, most observers believe that the risks involved with raising rates too soon are much larger than the risks of patience (though not all members of the Fed would agree). When the asymmetric risks are combined with the Fed's tendency to be overly optimistic, the argument for a cautious, patient approach gets stronger.