The Fed teases a September hike, but will it chicken out?

Interest rates could be going up in as soon as two months.

That's the takeaway from the Federal Reserve's policy statement on Wednesday. While the Fed took took no action -- and none was expected -- officials acknowledged ongoing strength in the labor market, Britain's vote to leave the European Union and ongoing evidence of firming inflation. The highlight: That near-term risks to the economic outlook had "diminished."

While the Dow Jones industrials and S&P 500 index rebounded following the news before closing nearly flat, the rest of the market seemed to indicate disappointment with the hawkish turn of sentiment. Gold and Treasury bond prices rallied, while the U.S. dollar declined. This suggests many believe the Fed's confident outlook could result in a premature tightening and an outright policy mistake.

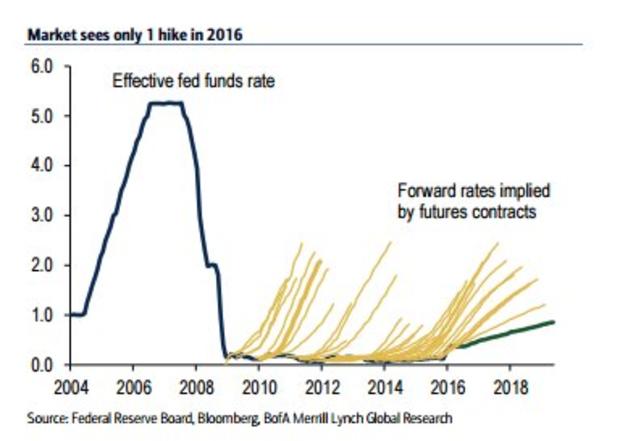

That's not surprising, given that investors are still very dependent on the flow of cheap-money stimulus and simply aren't excited about the prospect of rate hikes in September and December, if the Fed's "dot-plot" interest rate forecast from June is to be believed. (The futures market doesn't assign better-than-even odds of a rate hike until December.)

The temptation will be to give the market what it wants, a pattern the Fed has repeatedly followed. The 2013 "taper tantrum" is a perfect example, with the Fed backing away from plans to end the QE3 bond-buying program. The September 2015 surprise "no hike" decision is another. Call this the dot drama.

The liquidity junkies are clearly still in charge.

After all, the historic rally out of the late-June, post-Brexit low was driven by nonspecific hints of an epic "helicopter money" drop of coordinated fiscal and monetary policy support from Japan. And globally, the pace of central bank asset purchases has never been higher as the European Central Bank and the Bank of Japan gobble up bonds, equity funds and other assets in a bid to boost their economies.

With inflation rising but still low, the Fed has the luxury of being able to err on the side of an easier policy stance. But with ongoing tightening in the labor market and whiffs of inflation coming from the housing market (where shelter and rent costs are rising fast), this luxury might not last much longer.

Goldman Sachs believes there's only a 30 percent chance of a September hike, but a 70 chance the Fed will hike before year-end. It was also notable that the lone dissenter in the July policy decision, Kansas City Fed President Esther George, voted for an immediate rate hike.

We'll know more when Fed Chair Janet Yellen speaks at the central bank symposium in Jackson Hole, Wyoming, in August.