Stocks party like its 1999 even as risks mount

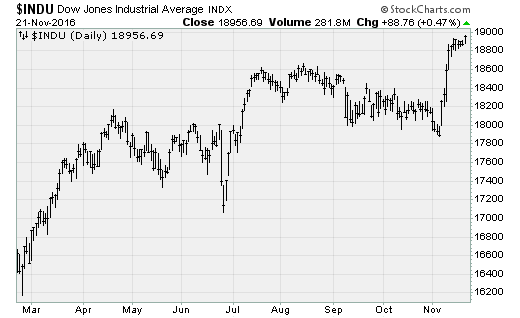

U.S. equities kept their post-election party in full swing on Monday, pushing all three major stock market indexes to new record highs together for the first time since Dec. 31, 1999.

Investors continue to view the incoming Trump administration and its plans for big tax cuts and spending increases as a huge tailwind for the economy. We’re also in a period of seasonal strength for the stock market (the oft-mentioned “Santa Claus” rally). Helping the latest bull run was some positive moves in the energy market as OPEC inches toward finalizing a deal to freeze production.

But the risks of chasing the rally from here are growing amid fundamental headwinds, looming interest rate hikes and evidence of narrow buying demand.

Energy has benefited from optimism surrounding OPEC’s ability to hammer out the details of the rough production agreement the cartel sketched out in Algiers in September. The Wall Street Journal cited comments from Iran’s oil minister saying it was “highly likely” a final agreement would be reached at the upcoming Nov. meeting. Headlines out of the “technical” OPEC meeting in Vienna highlighted progress as well, and oil rallied in early New York trading on Tuesday by nearly 4 percent, to $47.48 per barrel.

Moreover, Russian President Vladimir Putin said he sees no obstacles to a deal being reached and reiterated that if OPEC comes to an agreement, Russia (which isn’t a cartel member) would freeze production as well.

No surprise then that energy stocks led the way higher on Monday, up 2.2 percent as a group.

While the upside progress in stocks overall is awesome to see, one wonders if some irrational exuberance is materializing.

Breadth remains dangerously narrow despite energy’s turnaround, with just 62 percent of the stocks in the S&P 500 in uptrends vs. more than 75 percent in September and 80 percent back in April. Just 55 percent of NYSE issues are above their 50-day moving average vs. more than 80 percent in July.

Eric Bush of Gavekal Capital noted that more than one in five developed market stocks and more than two in five emerging market stocks are in a bear market, defined as a decline of 20 percent or more from their high in the past 200 days.

Looking at developed market stocks alone, the percentage in a bear market has doubled from 11 percent to 22 percent since late September.

Also, the futures market is now nearly certain the Federal Reserve will raise interest rates in December -- something that could magnify the recent selling pressure in bonds and bond-like stocks. On Friday, the U.S. 10-year Treasury yield hit levels not seen since last November. Higher borrowing costs could cause the housing market, auto sales and consumer confidence to hit the brakes.

This binary performance divergence has resulted in some aggressive fund movements as investors try to chase the winners. The latest Flow Show report from Bank of America Merrill Lynch shows that $28 billion has flowed into stocks (the largest inflow in two years), while $18 billion left bonds (the largest outflow in three-and-a-half years).

This gap between stock inflows and bond outflows is the largest ever.

Moreover, Jason Goepfert at SentimenTrader noted that in some cases, the pile-on might not be supported by the fundamentals. For instance, financial stocks have rallied despite a tightening of financial conditions as interest rates rise.

Again, the justification is that higher long-term interest rates are good for bank stocks because they widen banks’ profit margins. But higher rates also tend to reduce the demand for mortgage and auto loans.

Historically, financial stocks and financial conditions tend to move in unison. When they don’t, such as back in 1992 and in 2015, bank stocks tend to correct to the downside.

There is no other way to say it: The rally to new highs feels incredibly hollow and dangerous for investors looking to chase the move toward Dow 19,000 and beyond.