Your Social Security benefits at ages 62, 66 and 70

You can claim Social Security benefits at any point after reaching age 62, but the most commonly discussed ages for claiming benefits are 62, 66, and 70. Claim at age 62 and you’ll receive a smaller amount than you’d get at 66, but if you can wait until age 70, those delayed retirement credits will net you the biggest check. Here’s how much the average American is receiving in Social Security income at each of those ages.

How Social Security works

You can collect Social Security if you’ve accumulated 40 work credits. Typically, if you’ve paid into Social Security over a career lasting at least 10 years, you’ll qualify for the program.

Once you begin collecting Social Security , those benefits are paid by payroll taxes that are collected from current workers’ paychecks. Generally, the program is designed to replace about 40 percent of your pre-retirement income, but the amount you receive in benefits depends on a complex calculation that’s based on up to 35 years of your inflation-adjusted monthly earnings.

Early, on time, or late?

If you qualify for Social Security, you can claim benefits as early as age 62. However, the age at which you can receive 100 percent of your benefit is your full retirement age, and that age varies depending on your birth year. For example, if you’re turning 62 this year, your full retirement age is 66 years and two months. If you decide to hold off on claiming your benefits, you’ll get delayed retirement credits that increase your payment for every month you delay, up until age 70.

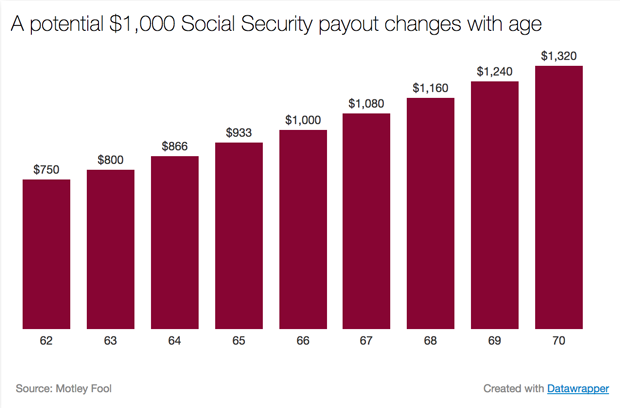

The following table shows how much a person with a full retirement age of 66 would collect at different ages, if their full retirement age benefit is $1,000.

Now that you understand how claiming benefits at different ages can impact your Social Security income, let’s take a closer look at what people are currently receiving in average benefits at various ages.

In February, the Social Security Administration awarded benefits to more than 243,000 retired workers, and on average, those recipients got $1,425.63 per month.

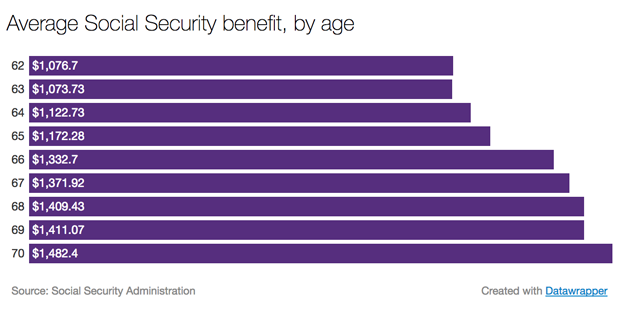

As of December, the average benefit that’s being paid out to recipients who are age 62 is $1,077. Individuals who are age 66 and age 70 are receiving an average of $1,333 and $1,482, respectively. The following table shows the average amount that’s being paid out to people between the ages of 62 and 70.

As you can see, the average 70-year-old is getting 37.6 percent more in Social Security income than the average person aged 62. That’s a big difference, and it suggests that it might make the most sense to wait until 70 to claim benefits.

Of course, you should also remember that delaying means forgoing years of payments, and those years of payments can add up. Claiming your benefits early, investing them (rather than spending them), and consistently earning a high return on the investment -- a big if, depending on the quality of your investment picks -- could in some cases increase your benefits comparably to the increase you could expect to see if you wait to claim them.

Don’t rush in

Everyone’s situation is different, and deciding when to claim benefits is a very personal decision that will depend heavily on your retirement goals, finances and health. There can be important tax consequences associated with Social Security income, so regardless of when you plan to claim, make sure you do your research first and explore all the strategies that are available to you.