One man’s $100,000 journey through arbitration

As Daniel Dempsey recalls it, every time he paid another $5,000 for costs related to his arbitration with Citibank (C), he thought it would be his last.

“It keeps getting dragged out,” the Arizona businessman said of his six-year-long dispute with Citibank over a checking account. “What I’ve learned is that I’m really bad at estimating what it will cost.”

Dempsey estimates he has spent about $100,000 so far in arbitrating his case with Citibank, a sum that has caused him and his fiancée, Elizabeth Wiseman, to delay their wedding from this fall until 2017. While he recently received a ruling in his favor from the arbitrator, who found that Citibank “willfully violated” the Fair Credit Reporting Act in its dealings with Dempsey, Citibank has appealed the decision. Dempsey said he believes he’s likely to face thousands more in legal fees because the case is moving into round two.

The original amount of the dispute? Less than $150 in fees.

The financial services industry bills arbitration as a “prompt and inexpensive means of resolving issues.” Yet for consumers who go through the process, it can end up far more expensive and time-consuming than one would expect from that description. The Financial Industry Regulatory Authority, a self-regulatory agency, said arbitration cases this year through September have had a turnaround time of 15 months. A majority of cases don’t complete the arbitration proceedings. FINRA noted that about six out of 10 cases are settled, while another 9 percent are withdrawn.

“There is no evidence that arbitration gives you better outcomes than going to court for individual cases,” said Thaddeus King, officer with The Pew Charitable Trusts’ consumer banking project, which has studied arbitration issues. “It’s difficult to find people involved in arbitration. Arbitration keeps these cases from existing in the first place.”

The Consumer Financial Protection Bureau (CFPB) earlier this year proposed new rules that would prohibit mandatory arbitration clauses, which it called “contact gotchas.” Its proposals include barring arbitration clauses that prevent class actions, which King said would give consumers a better option for pursuing legal recourse.

That’s because consumers typically are disputing small-dollar amounts, such as late fees, which makes it less likely they would hire an attorney to pursue a case, King said. He added, “You have to have a way to allow consumers to go to court when their disputes are small, and class action is really the only way.”

Arbitration isn’t an issue just in the financial services industry. Ride-hailing company Uber is currently fighting challenges to its provisions that block its drivers from joining class actions. And Airbnb, the home-rental service, recently was handed a victory when a judge upheld its mandatory arbitration clause.

Dempsey’s fight with Citibank started small. His dispute concerned an overdraft line of credit that was supposed to transfer money into his checking account if it became overdrawn. The bank allegedly waited until his balance was withdrawn by more than $25 to transfer the money, prompting several late fees in 2010.

Citibank also reported Dempsey late on his payments, leading to his credit score to drop from about 700, a level viewed as good, into the 500s, or the subprime range.

“What I was after was to fix my credit. That’s all I wanted,” Dempsey said. “I wasn’t interested in being a crusader against Citibank.”

Most consumers are unaware that they’ve signed what are called pre-dispute (or mandatory) arbitration agreements with their financial institutions. The clause is called “pre-dispute” because consumers are agreeing to go into arbitration before any dispute arises, effectively giving up their day in court.

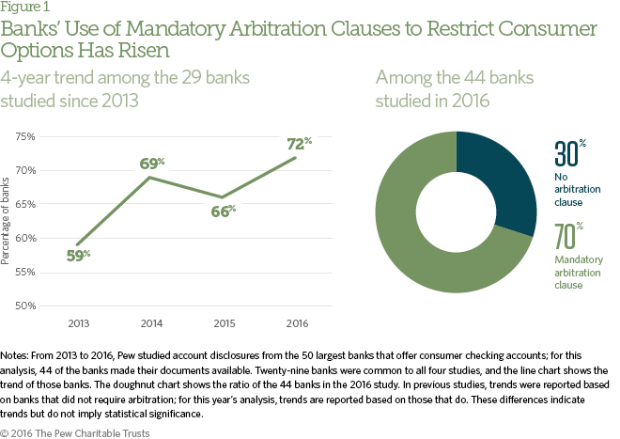

Arbitration clauses are now the norm in financial services agreements. The Pew Charitable Trusts found that 72 percent of banks now include mandatory arbitration clauses, up from 59 percent in 2013.

When the initial dispute arose, Dempsey proved to be ahead of the curve because he noticed what’s called a “small claims carve-out” in his Citibank agreement. “I thought it would be quick” to resolve the issue in small claims court, he said.

The small claims carve-out is fairly common in arbitration clauses, the CFPB found in a 2015 report. It noted that credit card issuers were “significantly more likely to sue consumers than the other way around” in small claims court.

Dempsey said he never got his day in court, however. “Citibank motioned to move it to a higher court. They also demanded arbitration,” he said. “They proved their contract to be lie. I never had a right to small claims court.”

Then arbitration process started, and the fees began to pile up. Dempsey said Citibank objected to four arbitrators in a row, requiring seven months to settle on an arbitrator. “They constantly filed motions to dismiss,” he said. “Every time Citibank filed something, we had to respond, and that’s not cheap.”

Dempsey hired legal counsel as well as expert witnesses, who he said charged between $200 to $300 an hour. To keep costs down, Dempsey said he pitched in on the case. “It sounds exaggerated, but I’ve spent 1,000 hours over the last six years,” he said. “It’s time stolen from my family, my businesses. And I don’t get compensated for it.”

Citibank said it tried “very early in the process to resolve the dispute and avoid arbitration or further proceedings by offering Mr. Dempsey an amount in excess of the fees in question which he declined.” The bank also said Dempsey “made repeated filings to avoid arbitration which generated attendant costs and once the case moved to arbitration, he filed motions to postpone at least twice as he changed counsel.”

Dempsey disagrees with Citibank’s characterization of the case. “I wrote to them for 18 months before I filed in small claims court, and they didn’t do anything,” he said. “They refused to acknowledge my letters. If anyone tried to resolve it, it was me.”

He added that settlement discussions with Citibank were fruitless since the bank was offering far less than what he had spent so far. “If I had spent $5,000, they offered me $200 or $300. It never made sense,” he said.

The arbitrator chided Citibank for its failure to respond to Dempsey in his initial attempts to fix his credit score. “Despite multiple attempts by claimant to get respondent’s mistakes corrected, including proper reporting to the credit bureaus, respondent did nothing,” the arbitrator’s interim judgement noted.

While the arbitrator sided with Dempsey, the ruling proved to be something of a Pyrrhic victory. The decision awarded Dempsey more than $20,500 in actual and punitive damages, as well as $30,000 in attorney fees, or about one-third of Dempsey’s legal costs. Since Citibank has appealed the ruling, Dempsey is now preparing for another round.

“We assert that all fees and charges assessed were proper,” the bank said in a statement.

One of Dempsey’s attorneys, Ryan McBride, said the victory was a validation. But he added, “I was disappointed with the numbers. I don’t think they were comparable to what would have been fair in this case.”

Dempsey may be unusual because he opted to fight Citibank rather than settle. Amanda Werner of Americans for Financial Reform, a nonprofit that advocates for financial reform, and Public Citizen, said many consumers decide against pursuing arbitration.

Said Werner: “The moment they see the cost, the amount it would take, the hours they would have to take off from work, a lot of people would give up at that point.”