Money Management: The Best Online Personal Finance Sites

This article was updated on December 3, 2009.

Personal finance software has come a long way since the days when you had to manually enter your credit card transactions in Quicken. Whether you are saving for college, trying to figure out where your cash is going, or making a New Year's resolution to save money, the new generation of money management Web sites can help you take control of your financial life. And they'll do all of that for free: You don't have to buy software or pay monthly fees, though you may have to wade through a few advertisements.

But are the sites safe? Is it worth the time and effort to sign up and overcome the inevitable bugs? And if so: Which site is best? I attempted to figure that out by plugging in my own financial data to see how well they work.

After taking five sites out for a spin — Mint, Buxfer, moneyStrands, Wesabe, and Thrive — I found stunning differences in their usefulness. (I didn’t test Quicken because its parent company, Intuit, plans to merge that site into Mint.com, which it recently bought.) Mint earned an impressive 4.5 stars on my five-star scale, three sites were pretty good, and one turned out not to be free after all.

These sites are supposed to work pretty much the same way: After you pull in financial info from your banks, brokers, mutual funds, and retirement plans, they sort the data into categories to show you how you’re managing your money, so you can do a better job. At some sites, you can also get a running tally of your net worth. Although you can’t move money between your accounts, you can (theoretically) get a snapshot of your entire financial life by seeing every transaction, from the $40 you put on your debit card for dry cleaning to the $2,200 you charged on your last vacation. The sites pick up every transaction you make with plastic, but you’ve got to fill in the details on how you spent cash. The sites also help you set goals and host online communities of like-minded budgeters offering advice and encouragement.

You needn’t worry about the sites draining your bank accounts. Typically, they use “screen scraping” technology to see, but not touch, your financial transactions. You go to the sites of your banks, credit card issuers, and investment companies, plug in your passwords and screen names, and the money management sites then pull in the data and categorize everything. Since the sites can only gather info from accounts where you have online access, if you haven’t set up passwords and sign-ons with your financial partners, you’ll need to do so.

One caveat: Your ability to use the sites effectively depends on the technology of your banks and brokers. Some let you easily download data onto any site; others don’t. And you might not be able to download your 401(k). So it’s not a bad idea to test a couple of money management sites to see how well they work with your finances.

Now for the scores ...

Mint

What’s Good: This was far and away the most sophisticated and comprehensive site. It was also exceptionally easy to use. (No surprise that MoneyWatch Family Finance blogger Stacey Bradford is also a huge fan.) Seconds after you type in your bank sign-on and password, your account information appears on Mint’s screen. While most money management sites pick up just one to three months’ worth of account information, Mint snagged nearly a year of data from several of my accounts. So Mint averages your spending over a longer stretch, taking into account semiannual and annual payments that look excessive in the short run, but ordinary with a longer view.

All the data creates the framework for Mint’s overview page, which notes how much you have in cash, debt, investments, and net worth, plus how your investments fared over the previous week. Each time you sign on, Mint automatically updates your accounts. Yesterday’s credit card purchases jump onto the screen, providing debt warnings when necessary. My favorite feature is the widget that lets you see trends. Click on it and up pops a full-color pie chart showing details of your spending, assets, debts, or net worth.

As expected from any Web site that wants to hang out with the cool kids, Mint offers an iPhone app. It lets you see the status of your bank account at any moment, so you won’t get socked with a $25 overdraft fee when using a debit card to pay for a $1.91 cup of coffee at Starbucks.

What’s Not So Good: The initial setup will take at least an hour (maybe more) — not the 10 minutes founder Aaron Patzer claims. And some of Mint’s automatic categorizations may be inaccurate. Mint didn’t know what to do with the income I earned from media companies, for example, which it listed as “subscriptions.”

The automatic alerts can drive you slightly batty, since they pop up when Mint thinks you’re doing something unusual, even when you’re not. For instance, I pay auto insurance once a year, so when I recently made the payment, Mint nervously rushed a “spending alert” to my e-mail. The site will also automatically put you on budgets for a handful of things — gasoline and dining out, for example — and will alert you anytime you exceed their thresholds. If you want them to stop nagging you over spending you consider normal, you’ll have to manually set those targets.

Mint is supported by advertising, which would be fine, except the promotions are often insidious and sometimes inappropriate. Before plugging in my credit score, I saw an ad for FreeCreditReport.com, a cleverly disguised $14.95-a-month credit monitoring service. Mint also recommends particular credit cards, bank accounts, and investment sites under its “ways to save” heading. Patzer says they’re based on running your spending through Mint’s computer models, but the site may lack enough information to offer an accurate view of your true potential savings, or lack thereof.

Rating: 4.5 stars

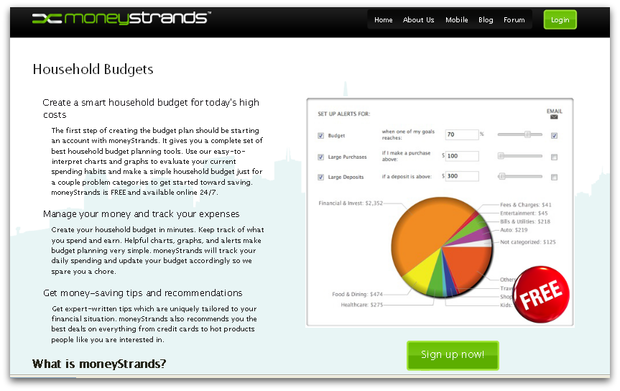

moneyStrands

What’s Good: Seven-month-old moneyStrands does many of the same things as Mint, but categorized transactions more accurately, so I didn’t have to do it manually. It also has a community tab that shows how your income and expenses stack up compared with moneyStrands’ “community average” (though you don’t know much about who’s in the community). If you travel overseas a lot, this site — originally designed for a Spanish bank — offers pretty nifty currency conversion features.

What’s Not So Good: Many of my accounts wouldn’t load. That’s why moneyStrands vice president of consumer products, Atakan Cetinsoy, says the site offers a “manual uploader.” You can download all your information from your financial institutions’ sites and then come back to moneyStrands and upload them. If I wanted to go to all that trouble, I’d upload my numbers to an Excel spreadsheet and do my money management offline. But when in comes to software, 2009 beats 1995.

Like Mint, moneyStrands supports its site with advertising, but the products here are largely unrelated to finance. So if you want free money management help, you’re going to have to put up with a few ads from Bath & Body Works.

Rating: 3 stars

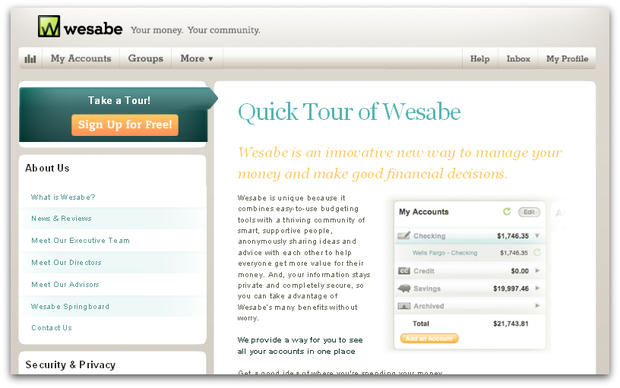

Wesabe

What’s Good: Like Mint, Wesabe has a useful, attractive home page summarizing your accounts and providing a graphical look at your spending.

Although you must categorize your transactions yourself, Wesabe makes this process relatively pain-free by saving all your previous tags, so you can type just one letter of a repetitive tag and click to get it categorized.

The site supports uploads from financial management software, such as Quicken, which means you can import all the already-categorized data you’ve accumulated in the software. This is a capability Mint doesn’t yet have, but is working on.

What’s Not So Good: The site doesn’t easily hook up to many financial institutions, leaving you with the moneyStrands dilemma of either going without some data or downloading it yourself. CEO Marc Hedlund says this is partly a security measure, because his site doesn’t contract with third parties to get access to customers’ financial information the way competitors do.

Although Wesabe boasts about its discussion groups (Hedlund says if you ask a question, you’re likely to have 10 responses within 48 hours), getting financial advice from random people may not be such a great idea. When I checked out the site’s “work at home moms” group, I found users recommending sketchy “opportunities” that charge you to get started. These are just the sort of scams the Federal Trade Commission warns consumers against.

Rating: 3 stars

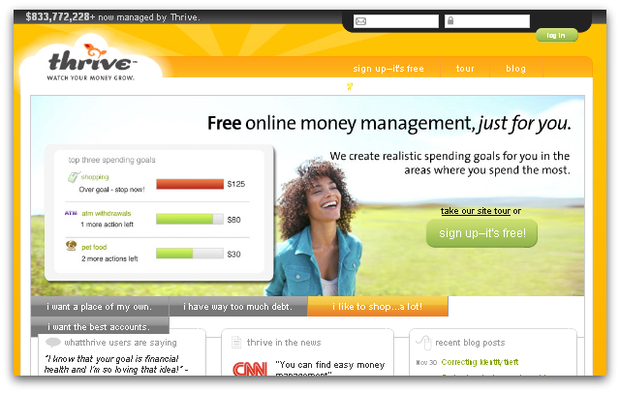

Thrive

What’s Good: Lending Tree’s Thrive (identical to sister site MoneyRight) offers easy downloading and a clean home page that greets repeat visitors with encouragements such as: “You’re meeting your spending goals — keep at it!” When you pull up details on where you’re spending your money, Thrive uses cute little icons — like a gas can or apple — that give the page a friendly look.

Thrive’s phone support was excellent. When I called because some of my accounts wouldn’t load, a helpful staffer gave me useful advice. “Customer service is very important to us,” says Lending Tree chief scientist Matt Wallaert.

What’s Not So Good: Thrive won’t let you see your net worth. Wallaert says the site doesn’t want to focus your attention on illiquid assets, when you should be concentrating on the money you can spend.

Thrive doesn’t count the cash in your checking account when totaling your rainy-day fund money. That’s because its studies show you’ll be more likely to keep your mitts off the dough if it’s in a savings account. Hey, Thrive: My mother used to call me “contrary” when I was a kid, and having a Web site boss me around as an adult makes me feel downright petulant.

Giving financial planning advice is supposed to be Thrive’s signature feature. But I couldn’t access its tools for getting out of debt, planning for retirement, and budgeting. Wallaert concedes the site is having some “technological issues” that he expects will be fixed soon. When Thrive repairs the technological glitches, it’ll be a contender for Mint’s top slot, particularly if the site keeps up its great customer service.

Rating: 2.5 stars

Buxfer

- Retirement Calculator Report Card: Are You Saving Enough?

- Dumbest Things You Do With Your Money

- How to Track Your Expenses Online

- 6 Reasons Debit Cards Are Dangerous

- Budget for Owning a Home

- Eco-Friendly Budgeting

What’s Good: It’s fast, well designed, and fairly easy to use — like Mint. Buxfer categorizes your expenses automatically and generally appears to do this pretty accurately.

What’s Not So Good: If you want to include your investment accounts, you must upgrade from the free service to one charging $3 or $4 per month. Admittedly, that’s less than $50 a year, but Mint does the same stuff for free. Since it’s important to review your investments when managing your money, I never got past the point of having to upgrade. It just didn’t seem worth it.

Rating: 2 stars

More on MoneyWatch: