Lessons from the top 11 mutual fund families of today and 1989

(MoneyWatch) Last October at the Bogleheads meeting, John C. Bogle showed a fascinating slide of the largest fund families of today and 1989. Here are the top 11 fund families then and now.

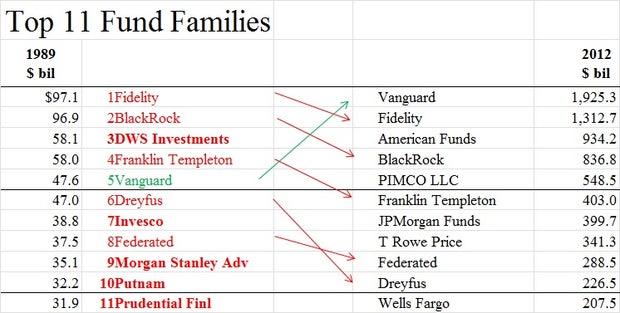

Falling out of the top 11 were DWS, Invesco, Morgan Stanley, Putnam

and Prudential. Dreyfus barely survived, at least for the time being,

as the once-mighty lion suffered from putting corporate profits ahead of

shareholder interests. What did these families have in common? High

fees. High fees are associated with lower performance. With

performance data now far more readily available from the likes of

Morningstar, consumers said goodbye.

- Misleading mutual fund advertisement?

- Lessons from the 10 most valuable companies

- Retirement gamble -- a critical review

Related to high costs, the six companies are owned by a publicly held company. Putting their shareholder interests ahead of the fund owners produced short-term profits while losing market share.

Newcomers to the list were American Funds, PIMCO, JP Morgan, T Rowe Price and Wells Fargo. Of those, American rose to No. 3 and is perhaps the lowest cost-loaded fund family distributed by advisers. PIMCO, T Rowe Pric, and Blackrock also have very low costs. Blackrock bought iShares, the largest family of ETFs. I'd guess Fidelity stayed in the top two by introducing some very good index funds to go with its expensive adviser-distributed funds.

Vanguard, the low-cost leader, skyrocketed to an easy No. 1 on the charts. But it wasn't impossible for high-cost families to break into the charts, as JP Morgan and Wells Fargo demonstrated. It's possible that they used their banking network to effectively cross-sell products. Still, I think the trend of consumers' wanting low costs will continue and suspect these two high-cost families won't be on the list in another decade.

Why I chose the top 11

Well, 10 is an arbitrary number, and I like to think outside the box, but I chose lessons for the top 11 fund families because I wanted to illustrate a point by including Prudential. Once at the 11th spot, Prudential dropped to No. 33 on the list, perhaps falling further than the high costs and misleading marketing materials might have predicted.

I think the answer as to why they plummeted on the list came a couple of weeks ago in the PBS "Frontline" episode on "The Retirement Gamble." In an interview, Christine Marcks, president of Prudential Retirement, was asked about the overwhelming evidence that exists on indexing beating expensive active investing. Her rather startling response was, "Yeah, I haven't seen any research that substantiates that. I mean, it -- I don't know whether it's true or not. I honestly have not seen any research that substantiates that." With that kind of obliviousness, I'm surprised Prudential didn't fall farther down the list.

And Prudential isn't alone with its head in the sand. The lesson here is that though many investment professionals are still ignorant of the impact of costs on performance, consumers aren't.

Lessons learned

When you choose a mutual fund, don't go for today's shiny stars, as they tend to flame out quickly. Look for low-cost funds from fund families with reputations of putting their fund owners first. Stay away from a fund family owned by a publicly held company, as they must put their shareholders ahead of the fund owners.