Last year's losers are winning this year

Over the long run, investment returns tend to revert to a mean. The problem is that we don't know what that mean really is, and the path to mean-reversion occurs randomly.

For example, speculative bubbles cause assets to reach unsustainable levels, even for long periods of time. Bear markets like the one investors in Japanese stocks have dealt with since 1990 also can last beyond many investors' horizons.

Although reversion to the mean isn't guaranteed, far too many investors ignore that market tendency and focus instead on the recent performance of their investments. The recency effect causes investors to buy yesterday's winners (high) and sell yesterday's loser's (low). On the other hand, investors that have a simple buy, hold, and rebalance approach purchase yesterday's losers (low) and sell yesterday's winners (high).

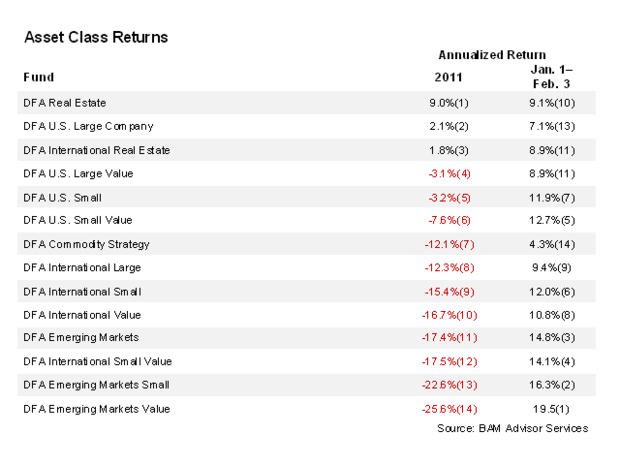

Market results in 2012 illustrate how quickly last year's dogs can turn into this year's winners. The table below shows the 2011 and year-to-date returns (through Feb. 3) of domestic and international asset classes (represented by Dimensional Fund Advisors mutual funds).

Note how the four worst performers of 2011 are the four best performers so far this year, while the top two performers are among the worst.

Another important point to observe in the data: Much of the returns provided by equities occur over short and unpredictable periods. From its inception in May 1998, the DFA Emerging Markets Value Fund (DFEVX) has returned 14.3 percent per year. This year, the fund has returned 19.5 percent. (Note that the annual average return since 1999 was 24 percent.)

The lesson is that to earn the returns that the capital markets provide, you have to be a patient and disciplined investor, not a returns-chasing investor.