In search of the perfect value fund

(MoneyWatch) So-called hindsight bias is the inclination to see past events as if they were predictable. Behavioral research has found a strong human tendency to be subject to this bias. Studies have also found that people tend to remember their own predictions as being more accurate than they really were -- in short, they're biased by what has actually occurred.

Hindsight bias has been found in many endeavors, including sports, politics, and even medicine. Keep this in mind as you consider the tale of "The Perfect Value Investor," the title of a 2006 article by investment manager James Montier (now with GMO). Montier noted that Bob Goldfarb, CEO of the legendary Sequoia Fund, was asked by Columbia University professor Louis Lowenstein "to select 10 dyed-in-the-wool value investors who all followed the essential edicts of Graham and Dodd." Goldfarb named nine, eight of which are listed in the table below. Montier used that list to draw out some of the characteristic behaviors of top value investors. Here are the traits he identified:

- Highly concentrated portfolios

- No need to know everything

- Don't get caught in the "noise"

- A willingness to hold cash

- Long time horizons

- An acceptance of bad years

- Prepared to close funds

It's important to note that in selecting the great value managers, Goldfarb had the benefit of hindsight -- he knew their performance. That's important because there may very well have been many value managers with the same characteristics who performed worse.

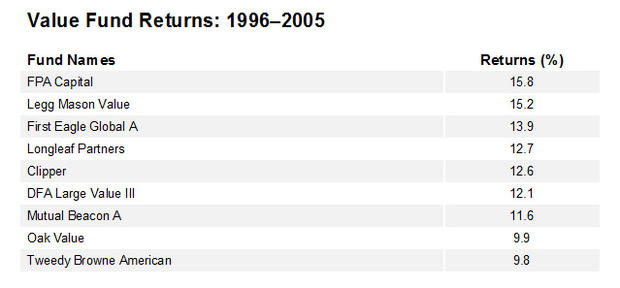

I wrote about the performance of these funds in 2006, comparing their 10-year annualized returns to the passively managed large-cap value fund from Dimensional Fund Advisors. Here's what I found.

Note that even with the benefit of hindsight, three of the funds underperformed the DFA fund. Investors ran almost a 40 percent of underperforming a passive strategy. We can only guess what the odds would have been without the benefit of hindsight. Note that the average return of the eight actively managed funds was 12.69 percent, an outperformance of just 0.63 percent compared to the DFA fund.

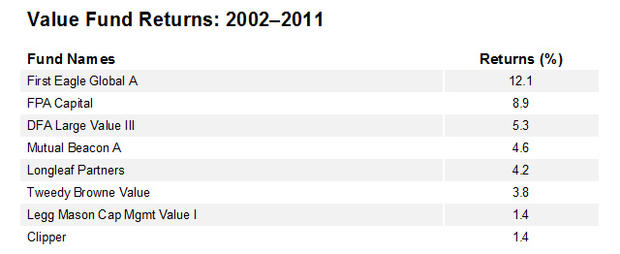

I also updated the data to include look at the out-of-sample results. The following reflects the returns for the 10-year period ending in 2011.

Only two of the seven remaining "perfect value managers" managed to outperform the passively managed DFA Large Value Fund (29 percent chance of success). The average return of the seven was 5.2 percent. You'll see that the Oak Value Fund is missing from this list. In 2010, the fund, with just $85 million in assets remaining, was sold to RS Investments. Thus, it's likely we have survivorship bias in the data.

Characteristic behaviors of the best value investors

Montier listed six common behaviors of great value investors. Passively managed funds exhibit four of those seven traits:

- They have long horizons

- They don't need to know everything

- They don't get caught in the noise

- They accept bad years

One trait that passively managed funds don't have in common with the top-performing value managers is that they don't concentrate portfolios. Instead, they broadly diversify. One of the major tenets of modern portfolio theory is that diversification reduces risk without reducing expected returns. So broad diversification is a good trait. This is what the Uniform Prudent Investor Act says about diversification: "Because broad diversification is fundamental to the concept of risk management, it is incorporated into the definition of prudent investing."

Passively managed funds also don't hold cash. One study found that nonequity holdings reduced returns for the average actively managed equity fund by 0.7 percent per year. In addition, if an actively managed fund holds cash, investors have lost control over their asset allocation -- the determinant of the majority of risk and expected return of a portfolio.

The last trait of the great value investors -- the need to close new investors -- is unlikely to impact a passively managed fund. The reason is that passively managed funds don't concentrate portfolios. The moral of this tale is that active management is a loser's game. Don't play.