Hurricanes and tropical storms are damaging homes. Here's how to deal with your insurance company.

For many people whose homes are battered by a hurricane or tropical storm, the trauma is soon followed by another major source of stress: dealing with their insurance company to file a claim.

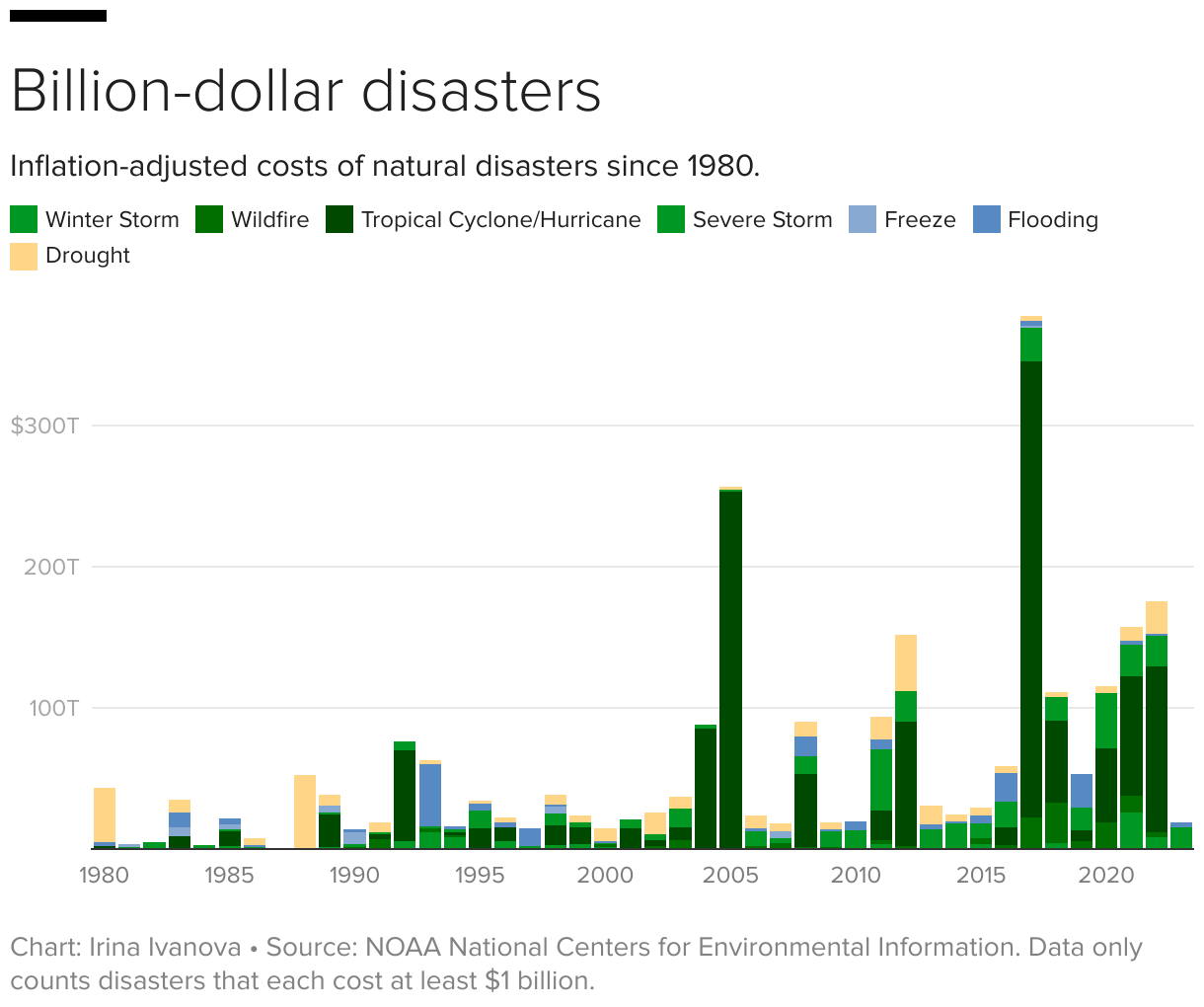

The U.S. suffered 20 separate billion-dollar weather and climate disasters in 2021, with a total cost of $145 billion, according to the National Oceanic and Atmospheric Administration. Individual homeowners whose properties are hit by a hurricane can suffer tens of thousands of dollars in damage, or even more, depending on the severity of the storm.

And the remnants of Tropical Storm Hilary delivered record-breaking rainfall to Southern California this week, flooding roads and causing mudslides, and could also cause flooding in Oregon and Idaho.

Knowing the basics about homeowners insurance and filing a claim can help avoid some pitfalls if disaster strikes. For instance, such insurance will typically cover damage from strong winds, but some policies don't cover windstorms. Typically, property owners will have a separate deductible for hurricanes, so it pays to check what your policy covers — and, equally important, what it doesn't — before a storm hits, experts say.

"It's smart to look it over when you renew," Vince Perri, founder and CEO of Elite Resolutions and a public insurance adjuster, told CBS MoneyWatch.

- The "100-year storm" could soon hit every 11 years. Homeowners are already paying the price.

- Here are the 15 most destructive hurricanes in U.S. history

- Hurricanes and climate change: What's the connection?

Here's what to know about hurricane insurance and how to deal with your insurer after a disaster.

Check your hurricane deductible

Hurricane deductibles typically amount to between 2% and 10% of the total value of your home. But in hurricane-prone regions like Florida, where Perri is based, he recommends getting a lower deductible because of the risk of facing high out-of-pocket costs in a disaster.

"Someone sent me a policy to review and he was going to go with 10% — I told him, 'Don't do that, because unfortunately we get hurricanes all the time'," he said.

For instance, a home worth $400,000 with a 10% deductible could face out-of-pocket costs of $40,000 if the property were wiped out. Going with a lower deductible may reduce incremental costs, but lead to financial disaster in case of serious damage.

"You want a 2% deductible when it comes to hurricanes," Perri advised.

Document your home before the storm

Once a year, homeowners should walk around their property and take photos to document their home's condition, Perri recommended. Taking this step will help you after a storm because you'll be able to demonstrate to your insurer that the damage was actually caused by the hurricane.

"If there is a storm, the insurance company may want to say the damage they are seeing is not as a result of the hurricane but is pre-existing," he noted. "If you have proof, that could help you tremendously."

Take photos immediately after a hurricane

After a storm, take photos of the damage as quickly as possible to document the immediate aftermath of the hurricane. Under a provision in homeowners insurance called "Duties After Loss," this is typically part of a homeowner's responsibility after a disaster.

Other steps you'll need to take under this clause may include filing a claim promptly, protecting the property from further damage and authorizing the insurance company to inspect your property. Check your policy to make sure you understand your duties in case of a storm.

File your claim quickly — and follow up

Some insurance policies require you to file your claim in a timely manner, but most homeowners are likely going to want to file as soon as possible in order to expedite payment. To that end, make sure to follow up with your insurance company at least every seven days after filing a claim, Perri recommends.

After a hurricane or other disaster, "They have got hundreds of thousands of insurance claims, so if you don't follow up, you could get forgotten," he added. "The squeaky wheel gets the grease."

You don't have to accept your insurance company's first offer

An insurer will either deny a claim, or accept it and make a payment — but it might not be an amount that you believe is enough to repair the damage to your home. In that case, you can file an appeal.

To do that, you can ask for estimates from contractors and submit those as proof the proposed payment is too low, or hire a public insurance adjuster who works for you, the homeowner, rather than the insurance company. Public insurance adjusters generally charge a fee of between 5% and 20% of the insurance claim.

"Hire somebody that puts these estimates together that you can use to appeal," Perri said.

If you use a contractor, make sure the estimate is extremely detailed, down to the number of coats of paint they will use to restore your house to its former state, he advised. "Documentation is king," Perri added.