How the Fed cried wolf (again) on interest rate hikes

Reading the tea leaves over at the Federal Reserve has become something of a pastime for Wall Street. For investors, the focus is on the ebb and flow of cheap money, or the timing and pace of interest rate hikes. And what of those so-called fundamentals, like corporate profits and U.S. economic growth? Yawn.

So it was with great interest that traders dissected this week’s release of the Fed’s account of its July policy meeting. The good news: Policymakers remain worried about downside risks to the economy and tepid inflation, lowering the chances of any rate hikes this year.

The bad news: Echoing former Fed chairman Alan Greenspan’s dot-com era warning of “irrational exuberance,” a number of central bank officials are growing concerned about the risks of leaving interest rates too low for too long, seeing signs of overvalued stocks and a risky “reach for yield” by bond investors.

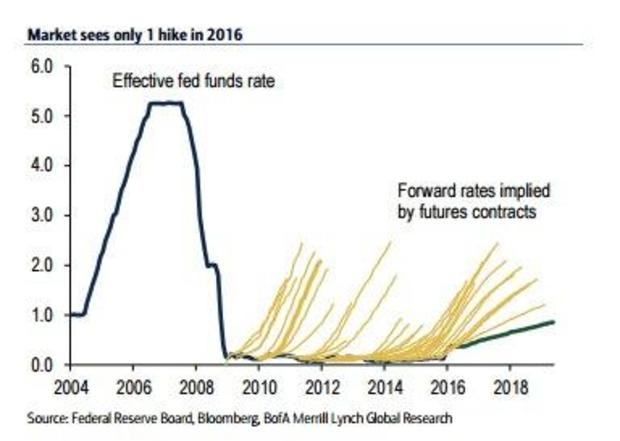

None of this is exactly new. The chart above makes clear that the Fed has a long history of saying it’s going to raise interest rates only to find a new excuse to delay.

Last September, when the world was prepared for the first rate hike since 2006, the Fed surprised financial markets by delaying liftoff until December. At the start of the year, policymakers triumphantly predicted they would raise rates another four times this year. Today, however, the futures market does see better-than-even odds of a rate hike until March 2017.

Yet, officially, the Fed’s current “dot-plot” Summary of Economic Projections suggests two quarter-point rate hikes are coming before the end of the year. This is hardly likely. Economist Ed Yardeni notes the Fed has a history of not changing rates just before a presidential election, likely taking a hike at the bank’s next policy meeting in September off the table. And with U.S. GDP on track to grow only around 1.5 percent this year, according to Gluskin Sheff economist David Rosenberg, down from 2.6 percent in 2015, it’s hard to see a move in December as well.

Not that this is stopping Fed officials from trying to keep their options open.

New York Fed President Bill Dudley, a key policy maker who typically lines up with Fed Chair Janet Yellen, said Tuesday that the time for a rate hike is drawing nigh and that a September rate hike was possible. He added that the futures market was underpricing the likelihood of higher interest rates. The same day, Atlanta Fed President Dennis Lockhart said he was open to at least one rate hike this year, citing evidence of nascent wage inflation and a tightening labor market.

On Thursday, Dudley added in a speech that fears of a stalling labor market have eased after two strong jobs reports in June and July.

All eyes are now on Yellen’s speech to the Jackson Hole central bank symposium on August 26 for confirmation that the center of power at the Fed remains cautious about hiking interest rates.

And for good reason. Rosenberg notes that the broadest measure of unemployment, including discouraged workers who have stopped looking for a job, stands at 9.7 percent and hasn’t declined since February. Inflation also remains stuck well below the Fed’s 2 percent target, while economic growth has slowed markedly amid weakening demand.

“Two years ago, the Fed believed the economy would expand 2.75 percent this year. A year ago, they were looking for 2.5 percent. Now, it’s 2.0 percent. The underlying pace is 1.5 percent,” he said.

Moreover, while June’s Brexit vote didn’t result in much of a financial or economic drag, the Fed is facing new headwinds in the form of tightening lending standards, the likelihood that inflation won’t hit 2 percent until 2018 at the earliest, and fresh thinking from the likes of San Francisco Fed President John Williams that the “neutral” interest rate could remain very low for a long time.

As I’ve said for years, until inflation is a clear and present danger, it’s best to dismiss the Fed’s occasionally hawkish proclivities and prepare instead for a continuation of its ultra-low interest rate policy. Like the boy who cried wolf too many times, the Fed is losing its credibility.