How long will your retirement savings last?

One of the worst retirement planning mistakes you can make

is withdrawing too much, too quickly from your savings in

IRA, 401(k) or other accounts. If you spend down your savings while you're retired

but could have worked and then run out of savings at an age when you can no

longer work, you’ll be kicking yourself in later years. In short, it's imperative to avoid the “money death” that can happen before your actual death.

Nobel Laureate economist William Sharpe and a recent report from the Stanford Center on Longevity provide valuable help with this critical retirement planning task.

One way to avoid running out of money before you die is to buy an annuity from an insurance company, which then guarantees you a monthly payment no matter how long you live and no matter what happens in the economy. Unfortunately, many people don’t buy annuities, but instead keep their savings invested in the stock market and make withdrawals to cover their living expenses.

Another mistake is not having a formal plan for withdrawing money from your savings to insure you have a good chance of making your money last as long as you do. Instead of a plan, many people simply withdraw what they need to cover their current living expenses, and they often withdraw at an unsustainable rate.

One method that was devised to give retirees guidance on how

much they could withdraw from their savings was the so-called “4 percent rule.” This method helps insure that your savings will generate a retirement

paycheck that lasts for life.

With a strict application of the 4 percent

rule, you invest your savings in a portfolio balanced between stocks and bonds,

ranging from 50 percent to 75 percent in stocks and the rest in bonds. In your

first year of retirement, your annual paycheck would equal 4 percent of your

retirement assets. Each year, you give yourself a raise equal to the rate of

inflation as measured by the Consumer Price Index.

Research supporting the soundness of the 4 percent rule shows there’s a good chance that your savings would continue to generate a retirement income for at least 30 years.

Lately, however, this axiom has drawn criticism for several reasons. First, interest rates were a lot higher when the 4 percent rule was first devised; today, your bond investments generate lower interest earnings and hence a lower retirement income.Second, the 4 percent rule assumes your investment returns (net of expenses) equal historical averages for stocks and bonds. But if you’re paying a substantial fee from your savings for investment management and/or financial advice, such as 0.50 percent per year or more, you might increase the odds of outliving your money. Many mutual funds and investment managers charge 1 percent or more of your retirement assets.

Sharpe’s new post on retirement income illuminates the flaws with the 4 percent rule. He advocates that any rule for spending out of a retirement account should depend on how much money you have and how long you're likely to need it. The 4 percent rule or its variations meet this criteria when you initially retire. Thereafter, the rule fails this criteria because it ignores the investment gains or losses that have happened since you retired and the fact that you continue to be alive.

On this last point, imagine what would happen if you use a rule that generates a retirement paycheck for just 30 years. In your 29th year, if you’re still alive and healthy, you’d start getting very nervous.

Ideally, any spending rule will make adjustments in your retirement paycheck along the way to reflect how much money you have left and how long you expect to live given that you’re still alive.

One way to make these adjustments yourself is to recalculate your annual retirement paycheck each year using the amount of assets remaining at the beginning of the year. Pick a period of remaining years that you expect to live based on your expectations for your life expectancy. (For help, see my previous post that helps you project your life expectancy and that of your spouse or partner.)

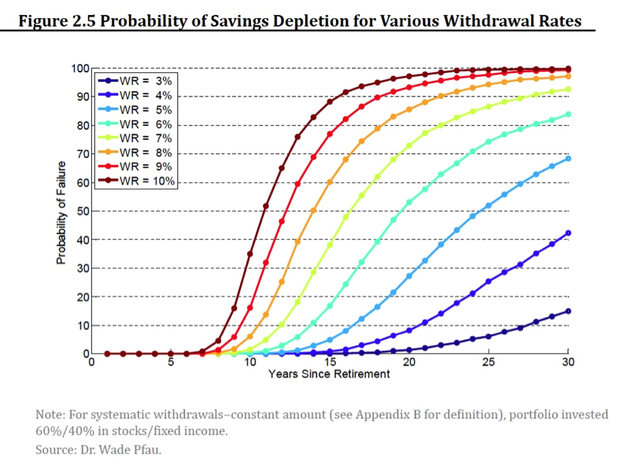

The Stanford Center on Longevity, together with the Society

of Actuaries, recently released a report that contains a chart that can help

you with this annual adjustment. This chart shows the odds of running

out of money for various withdrawal rates and periods of retirement. Each line

represents the odds of failure for a given withdrawal rate and period of

retirement for a portfolio invested 60 percent in stocks and 40 percent in

bonds. The horizontal axis shows the number of years remaining in retirement,

and the vertical axis shows the odds of failure.

The left-most dark red line represents the odds of someone exhausting their retirement savings with a 10 percent withdrawal rate. It shows very low odds of failure for periods of remaining retirement lasting up to seven years, but then the odds of failure climb quite dramatically. The odds are about 50-50 that the portfolio would fail at 10 years, and the odds are over 90 percent that the portfolio would fail after 15 years.

On the other hand, the right-most black line represents a withdrawal rate of 3 percent, and the odds of failure are quite low, even for periods of retirement remaining up to 30 years.

It may take some time for you to fully understand the issues

that come with generating retirement income from your savings, but you’ll

appreciate the time you invest in your planning when you reach your 80s and 90s

with your retirement savings still chugging along.