Why home prices may be ready to lift off

The housing market has dropped off the radar in recent months as sales and price gains slowed. Instead, the focus was on things like the holiday shopping season, the Super Bowl and Ebola.

That's set to change, however, as the data suggest home price increases are about to accelerate.

On Tuesday, the S&P/Case-Shiller Home Price Index, on a month-over-month nonseasonally adjusted basis, posted an increase for the first time since August. Winter's chill is beginning to thaw. On a seasonally adjusted basis, the index posted its best price gain since 2014. Prices, however, are still more than 16 percent below their prerecession peaks.

A few things have been holding housing back lately. For one, inventories have dried up a little, limiting choices. The National Association of Realtors (NAR) notes that families are staying in their homes longer, an average of 10 years vs. the long-term norm of seven years. Wages gains have also been tepid so far in the recovery, which is hampering first-time buyers. And evidence shows that student loan debt is limiting the ability of many Millennials to get a mortgage.

Yet positives are appearing.

The household formation rate has increased to its highest level since the housing bubble. New-purchase mortgage applications are inching higher, thanks to the recent decline in home loan interest rates. New first-time homebuyer affordability, according to the NAR, has returned to early 2014 levels. And thanks to deleveraging efforts -- defaults, short sales and the like -- household mortgage debt has returned to 2001 levels, according to data from the Federal Reserve.

Bank of America Merrill Lynch economist Michelle Meyer is optimistic about housing this year, in large part because of a bounce in household formation as young adults -- many admittedly saddled with debts from higher education -- finally start moving off mom's couch en masse again.

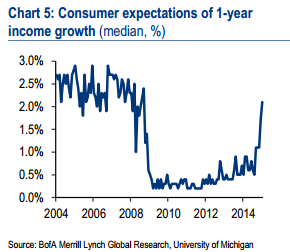

Job-seekers are looking at the prospect of higher wages amid the best run of job creation since the 1990s and are taking the plunge: According to the University of Michigan's consumer survey, Americans now see income growth of 2 percent this year vs. 0.5 percent just six months ago.

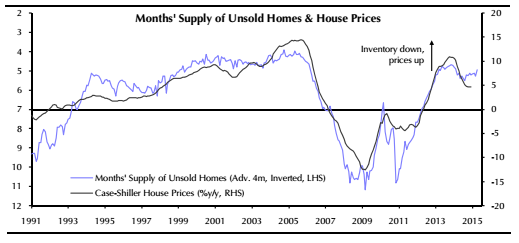

While some hurdles remain, including relatively tight mortgage credit conditions, home price gains look ready to accelerate as winter -- which has been brutal in much of the country -- gives way to the summertime peak in housing activity. Plus, this year prices could get a boost because relatively fewer homes are available. The chart above from Capital Economics illustrates an important dynamic. As home prices rise, new construction activity will follow, providing a lift to U.S. economic growth later this year.