Good news, workers -- wage gains are coming

By most measures, we're in the later innings of this economic cycle. Corporate profits are cooling. Commodity prices are collapsing. Fifteen central banks globally have lowered interest rates this year to combat economic stagnation throughout Asia and Europe.

And yet for the average U.S. worker, one key trend has yet to materialize: A significant bump in pay. Sure, job-creation is running at its best pace since the dot-com boom, and the nation's unemployment rate has dropped to 5.6 percent. But wages have barely budged.

That's about to change.

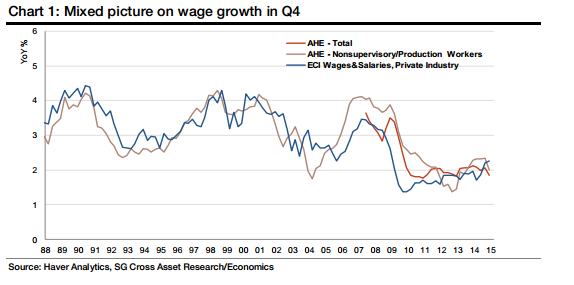

As the chart below shows, wage growth was mixed in the fourth quarter of 2014. The Employment Cost Index released on Friday rose slightly to an annualized growth rate of 2.2 percent. Wages and salaries growth was more tepid at 2.1 percent, compared with 1.9 percent in 2013. Average hourly earnings came in at 1.7 percent year-over-year.

In short, nothing to write home about. In a typical post-recession recovery, wages should be growing closer to 4 percent per year.

The lack of wage growth has many wondering why the Federal Reserve seems committed to raising interest rates sometime this summer -- something it hasn't done since 2006. On the surface, such an action seems a tad premature.

But according to economist Aneta Markowska at Societe Generale, the data suggests the Fed is correct in holding firm on this timing.

That's because she expects wage gains to accelerate later this year as pent-up wage deflation -- something that Fed chairman Janet Yellen discussed at last year's Jackson Hole symposium -- dissipates. Wage deflation arises from the difficultly employers have in cutting pay during recessions for fear of angering workers and harming productivity. Instead, wages hold steady. As the economy recovers, firms find that they do not need to raise wages to attract new applicants.

Eventually, as the pool of available workers dries up and this wage deflation reserve disappears, history suggests wages will rise rapidly. Like so much in economics, the reasoning behind why these things happen is murky. We only observe that they do;thus, expectations are set based on prior patterns.

Both Yellen and Markowska seem have a similar outlook: That wage gains have merely been delayed, not denied. Something similar happened in the 1990s and the mid-2000s. Yet the depth of the job implosion during the housing bust has made the wage deflation reserve in this cycle much deeper. As a result, the wait for higher wages has been much longer.

As a rough guide, the hole in the labor market was about 150 percent larger during the Great Recession than in the dot-com bubble. This is why the Fed has been more patient holding interest rates near zero percent in this cycle as the unemployment rate has tumbled and the slack in the labor market has dried up. Now, it appears that the deflation reserve is the only thing holding wages back.

Waiting to hike interest rates until wage gains actually appear "may be imprudent for the Fed," according to Markowska. That's because once labor market tightens and the unemployment rate falls near its "natural" rate -- as it's on the verge of doing now -- wage deflation quickly disappears.

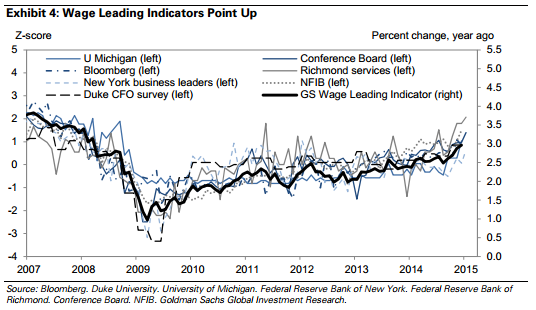

Analysts at Goldman Sachs believe this could be related to the realities of workers asking their boss for a raise. It's only when employers realize there are fewer people competing for jobs that workers' bargaining power starts to "bite" and results in bigger paychecks.

Typically, before the economic expansion ends we would see wage growth roughly double from current levels. Predictive data points compiled by Goldman, shown above, suggest we're not quite there yet. The bank forecasts wage growth this year somewhere around three percent.

Still, it shows things are on the right track and that the Fed is justified in moving towards normalizing interest rates.