Do retirees spend less money as they age?

(MoneyWatch) If you're approaching retirement or are newly retired, can you plan to spend more money in your early years of retirement while you're still active and mobile, and justify this by assuming you'll spend less money as you get older? Some financial advisors suggest this strategy when helping clients' plan their retirement income and spending patterns, so let's take a look to see if this is a realistic assumption for you.

- The magic formula for retirement security

- A great way to stretch your retirement savings

- Retiring baby boomers: Dropping out to make every dollar count?

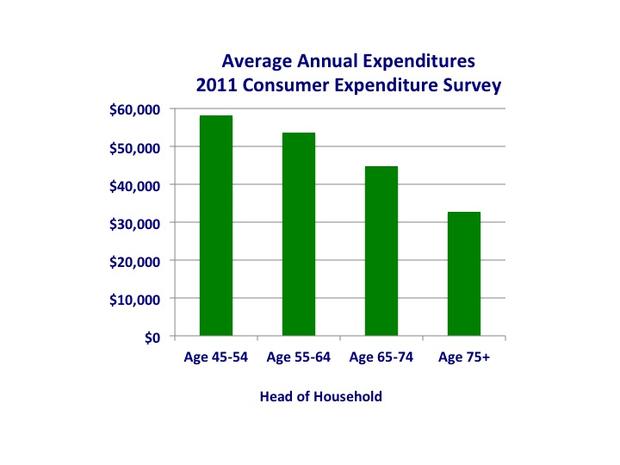

To gain insights into this critical issue, many financial analysts rely on the Consumer Expenditure Survey (CES) produced by the Bureau of Labor Statistics, part of the U.S. Department of Labor. The CES summarizes statistics on expenditures for a variety of goods and services that we buy each year, and breaks the results down by the ages of the head of each household unit. For example, if analysts see that households headed by someone who's age 65 to 74 spend less money on cars than households headed by people who range from age 55 to 64, or for younger age brackets, they conclude that older people spend less money on cars.

And indeed, the data supports the notion that spending peaks in households headed by people age 45 to 54, as shown by the following graph that summarizes data on total annual average expenditures from the 2011 CES.

Financial analyst and author Harry Dent takes this data several steps further and develops "demand curves" for dozens of common consumer items, based on the CES. These demand curves predict how expenditures are expected to change as you age. Dent's graphs show dramatic reductions as people age in many common consumer expenditures, including clothing, car expenses, computers, travel, jewelry, club memberships and furniture. Some predicted reductions in spending are counterintuitive -- for example:

- Accounting fees (doesn't everybody pay taxes?)

- Bedroom and bathroom linens (I'm assuming older people still use the bedroom and bathroom)

- Charges for checking accounts (don't older people still write checks?)

- Eye exams and eyeglasses (go figure!)

- Underwear for both men and women (I'm not going to touch that one!)

Other projected spending reductions by age are more predictable. For instance, the costs for cigarettes decline with age -- presumably there are fewer smokers in the older population, for reasons you can guess. Spending on men's haircuts men also declines with age -- I can personally attest to the validity of this phenomenon!

On the other hand, some expenditures increase dramatically and predictably with age, such as money spent on hearing aids, Medicare payments, long-term care, prescription drugs, and, ultimately, costs for cemetery lots and funerals.

Most of this information makes sense to me; as I get older, I realize that my happiness doesn't depend as much on material goods. I'm more interested in spending time with friends and family, so I don't spend as much on "things." I'm fine with buying "just enough" to meet my needs. For example, I don't replace "out of date" appliances very frequently if they still work; I still use my four year-old iPhone 2, and we have a 15 year-old TV and DVD player in the house. And I've got a whole closetful of clothes that still fit and look nice.

Dent contends that our collective spending habits drive our economy and stock markets, and he predicts that reduced spending by aging boomers will eventually cause "The Great Crash Ahead." Take his predictions with a dose of salt, however, as he's been wrong before, predicting the Dow would be at 40,000 by 2010 and that the S&P 500 would fall 30 to 50 percent in 2012 (it actually rose by more than 13 percent, with a total return of 16 percent including dividends).

But let's focus on how you should plan your retirement and how you'll generate retirement income from your savings. Let's return to my original question: Is it reasonable to plan to spend more money in your 60s but justify it by assuming you'll spend less in your 70s and beyond? Stay tuned for my next post, which examines this important question in more detail.