Can you time the stock market? Why investors rarely buy low, sell high

The beginning of 2018 has been historic, continuing the never-before-seen dynamic that's been in play since President Trump's surprise victory in November 2016. For the first time, the S&P 500 had a perfect year in 2017 on a total return basis, climbing in each and every month.

On a relative strength-indicator basis, stocks haven't been this overbought since the 1950s. The CBOE Volatility Index -- known as Wall Street's "fear gauge" -- has never been this complacent. On a price-to-earnings ratio, stocks have only been more expensive heading into the peak of the dotcom bubble.

And investors have rarely been as bulled up amid one of the "easiest" rallies in history. SentimenTrader notes that the S&P 500 hasn't strayed more than 1.5 percent from a high in more than 90 days, the second-longest streak of persistent highs in history. Moreover, the "dumb money" strategy of buying at the open of the trading session has produced nine winning days in a row -- among the longest streaks in market history.

Change seems to be in the air, however. The bond market is showing signs of strain as the two-year Treasury bond yield pushes to two percent for the first time since 2008, up from a low of just 0.2 percent in 2011. Crude oil is threatening to push above the $65-a-barrel level for the first time since Saudi Arabia started the oil price war in 2014. The labor market is drum tight. The GOP's tax cut legislation is about to juice the economy just as GDP exceeds capacity for the first time since the financial crisis. And the Federal Reserve is set for another batch of interest rate hikes this year.

These trends all point to higher interest rates driven by a resurgence of inflation. A change of dynamics from what stock market bulls have enjoyed during this cycle.

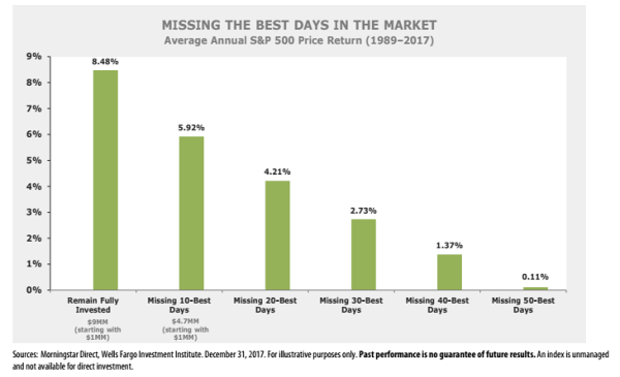

Yet history shows that trying to time the market -- attempting to buy low and sell high -- has been fraught with dangers of its own. Scott Wren at Wells Fargo Investment Institute admits that as investors ponder 2018, they likely do it "with a sense of both anxious anticipation and maybe a little fear." But he finds that since 1989, a cautious approach that inadvertently sits out the market out on its best days has a dramatic negative impact on performance.

Remaining fully invested since 1989 has resulted in an average annual return of 8.5 percent. Missing the 10 best trading days lowered this return dramatically -- to 5.9 percent. Missing the 50 best days over a 28-year period -- missing just 0.2 percent of the time -- dragged the average annual return to 0.1 percent.

It feels like investors are damned if they do, with market overvaluation pointing to weak returns going forward if they stay invested, and damned if they don't, with the market ignoring warning signs about valuations and grinding higher for years.