Buying lottery tickets will never make you rich

Regularly play the lottery? You're in good company. The average American spends $207 annually on tickets. And the figure is twice as high in several East Coast states, where giant jackpots for games like Mega Millions and Power Ball appear to be particularly alluring.

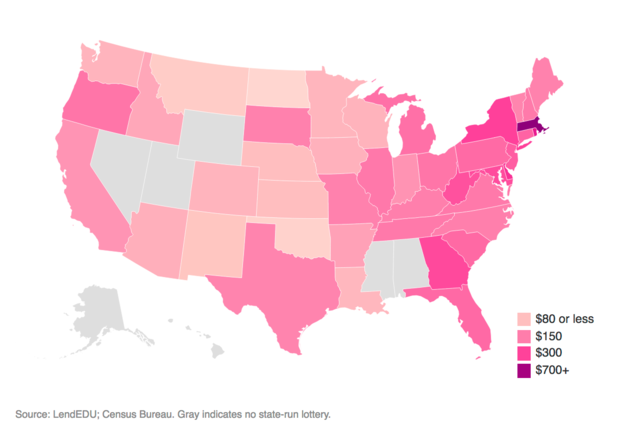

According to a study by LendEDU, the average Massachusetts resident spends a whopping $735 annually on lottery tickets. Rhode Islanders plop down $514 annually. And if you live in Delaware or New York, you're likely spending about $400 a year, or $33 per month (see map below).

The only trouble with investing that kind of dough in lottery tickets is that the odds are definitely not in your favor. Indeed, you're 300 times more likely to get struck by lightning in any given year than win a multimillion-dollar jackpot in the Mega Millions or Power Ball contest -- no matter how frequently you play.

The odds are better with "scratchers" -- those little instant winning tickets that you can buy for prices ranging from $1 to $50, according to LendEDU. But it's sure no way to get rich.

The lending site experimented with determining "a return on investment" with scratchers by buying $1,000 worth of tickets. The good news: The site won with 68 of the 314 tickets -- indicating that you have a near 22 percent chance of a positive return with lottery scratchers. And, in fact, a big win ($500) on a $20 ticket helped LendEDU recover the bulk of its investment.

The bad news: The site -- like most players -- lost money in the end, recovering just $974 of its $1,000 investment for a total return averaging -2.6 percent.

How per-capita lottery spending varies by state

Put another way, if you were a Massachusetts resident "investing" $735 a year in lottery tickets, after 40 years and a total expense of $29,400, your "jackpot" would be worth $18,289 -- about $11,000 less than you invested. That's assuming you were as lucky as the players at LendEDU. You have a three out of four chance of losing on any given bet, and though the winners could pay off handsomely, those rich-but-rare big payoffs are no match for the relatively rotten odds.

Want to turn the odds in your favor? Consider investing your lottery cash elsewhere.

The investing world has one near sure thing -- U.S. Treasury bills. These supersafe investments have posted only one money-losing year in the 90-year history examined by market researchers at Ibbotson, a division of Morningstar Investments.

Although Treasurys won't make you rich overnight, if our hypothetical lottery player invested the same amount of cash in T-bills year after year, he would have a tidy $62,447 at the end of 40 years -- $44,158 more than he would end up with playing the lottery.

Don't need a sure thing, just better odds? Consider big-company stocks, which have about a 73 percent chance of producing a positive return in any given year, according to Ibbotson data. (Incidentally, that's roughly the inverse of your odds with lottery scratchers, which have about a 22 percent chance of producing a win, according to the LendEDU study.)

And even though stocks have money-losing years roughly every four years, on average, those losing years are no match for the better odds. Big-company U.S. stocks have returned 10 percent annually, on average, since 1926. Thus, if you invest your $61.25 per month in a broad basket of U.S. stocks, your nest egg is likely to grow to a whopping $387,350 over 40 years.

Willing to take a somewhat bigger risk? You, my friend, know how to become a millionaire. Small-company stocks are more volatile -- rising in just 62 years out of 90, or roughly 69 percent of the time. But they also promise bigger potential payoffs -- 12 percent on average annually. What would your nest egg be worth after 40 years? A cool $720,592.

Keep at it for just another three years and, guess what? You're a millionaire. You'd have $1,033,640.

Sure, it's not quite as exciting as imagining that a $1 ticket will turn you into a millionaire overnight, but it's a much better bet.