Need $100 fast? These lower-cost loans can help.

Half of Americans can't afford an unexpected expense, so what happens when they need a car repair or their job sends them home early for a week? For millions, the answer is often a high-cost payday loan that usually carries an exorbitant interest rate.

But better options are now available after years of advocacy from consumer groups and new federal rules. Some large banks now offer small-dollar loans at rates far cheaper than payday loans. Since 2018, six banks — Bank of America, Huntington Bank, Regions Bank, Truist, U.S. Bank and Wells Fargo — let checking-account holders take out short-term loans of $10 to $1,000, making it more affordable to handle a financial emergency or make a purchase.

"They require no travel to a branch and no waiting for an online lender to review an application and transmit the funds," the Pew Charitable Trusts wrote in a recent report. "Instead, customers complete short applications via the bank's website or mobile app, and the bank deposits the funds, usually within minutes, into the customer's existing checking account."

The typical interest rate on such products, sometimes called installment loans, can rise as high as 18%. But that's less than the nearly 21% average annual percentage rate on credit cards today, and they're far more affordable than the short-term financing peddled to people with poor credit, such as payday, car title or pawn shop loans.

Compared with such options, a small bank loan is about 15 times cheaper, Alex Horowitz, who leads Pew's consumer finance research and authored the lending report, told CBS MoneyWatch.

"Borrowing $500 for four months from a payday loan costs about $500 in fees. Banks are charging $30 in fees," he said. "The upside is so big because low-income households haven't had good options to borrow money in the past. And now they do."

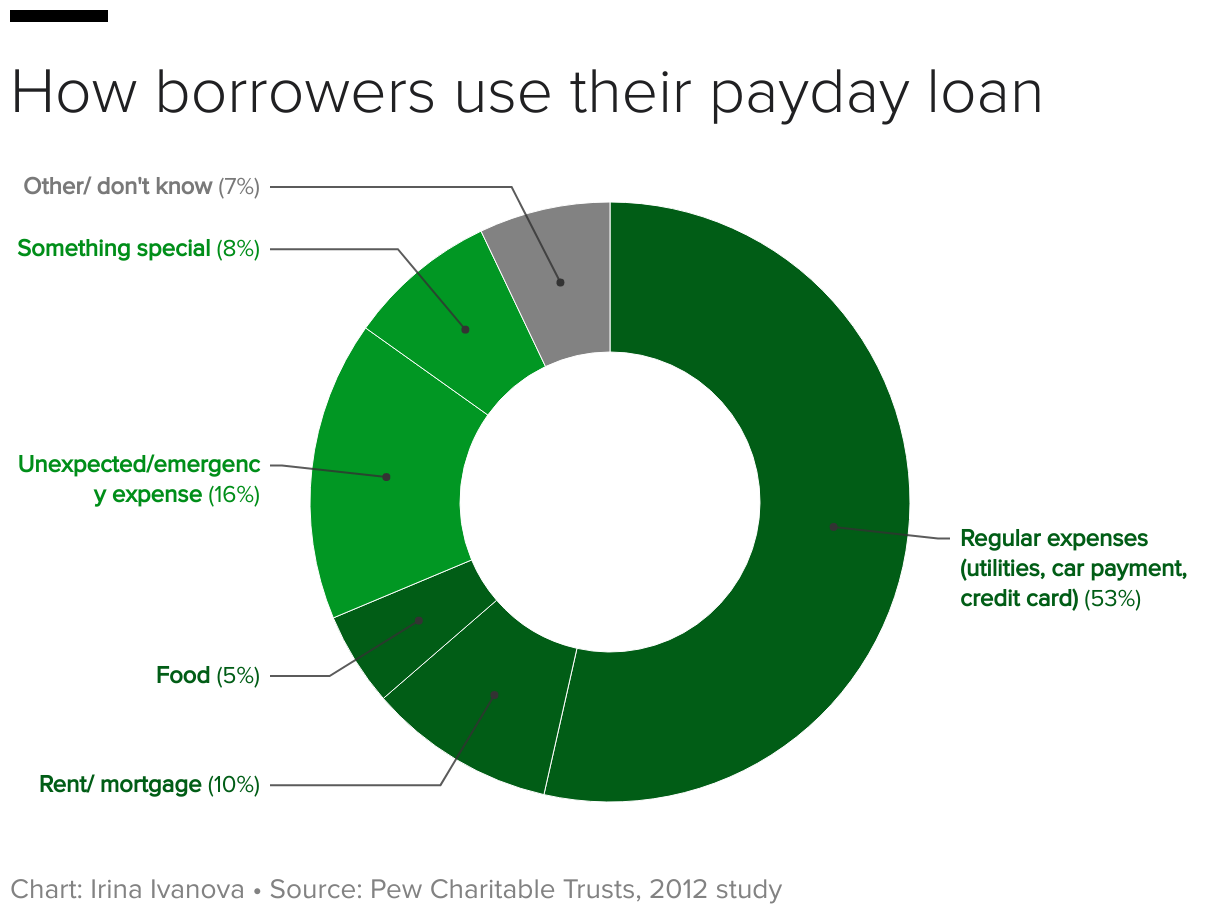

Payday loan math

The Federal Trade Commission offers this illustration of how fast payday loans can become unaffordable. Let's say someone borrows $500 from a payday lender. The loan costs $15 per $100, so the borrower writes a check (or authorizes a bank withdrawal) for $575, due in two weeks' time. If they can't pay it off when the two weeks are up, the lender tacks on $75 to roll it over for another two weeks, bringing the total owed to $650. So the cost of borrowing $500 for one month to $150 — to a whopping 360% APR.

Some states have moved to regulate these loans, with 18 states capping APRs at 36% or less, according to the Center for Responsible Lending.

It doesn't take a financial disaster to push people into borrowing. In a 2012 survey, the vast majority of borrowers said they used a payday loan for everyday expenses, such as food, rent or utility bills. Just 16% said they had an emergency expense, and 8% said they used the loan for "something special."

"A lot of Americans don't have much margin for error and need a little help when they get fewer hours at work in a week or have an unexpected expense," Horowitz said.

Payday loans have one major benefit: They're a fast way to get money if you're desperate.

"Payday loans are expensive, they have unaffordable payments, they leave people in debt for much longer than advertised, but they're quick," Horowitz said.

Until recently, banks generally shied away from offering small-dollar loans. It wasn't clear that it was legal for banks to lend without pulling a credit report, the cost of which outweighed the potential profitability of lending a small amount of money to a financially strapped customer.

But after guidance from financial regulators in 2020, some banks started offering these products, which rely heavily on automation and a customer's checking account history. Examining how often a customer makes deposits and withdrawals is often a better indicator of whether they can repay a few hundred dollars than a traditional credit report, Horowitz said.

Because the process is so automated, there's no way to ask for one, Horowitz noted — a person logs into their bank account, and if they're eligible to ask for a loan they'll see the option. "Banks want to show these loans to people who qualify for them, not people who don't," he said.

Some credit unions offer a similar product called a Payday Alternative Loan. Still, Horowitz said that tens of millions of Americans lack options for affordable borrowing in a pinch, and Pew is pushing for more banks to offer this option.

"This should be a universal product in the banking system," he said. "Millions of borrowers can save billions of dollars, and loans like this can replace a lot of the high-cost lending that takes place."