Asset Allocation Guide: How much risk should you take?

Today, we begin a series designed to help you determine the best way to allocate your assets. I have written a great deal on this subject, but it's advice worth repeating time and again. We’ll start with focusing on the ability to take risk.

An investor’s ability to take risk is determined by four factors: (1) investment horizon; (2) stability of their earned income; (3) need for liquidity and (4) options that can be exercised should there be a need for a “Plan B” (a contingency plan that can be adopted should events occur that increase the likelihood of the plan failing to achieve it’s objective).

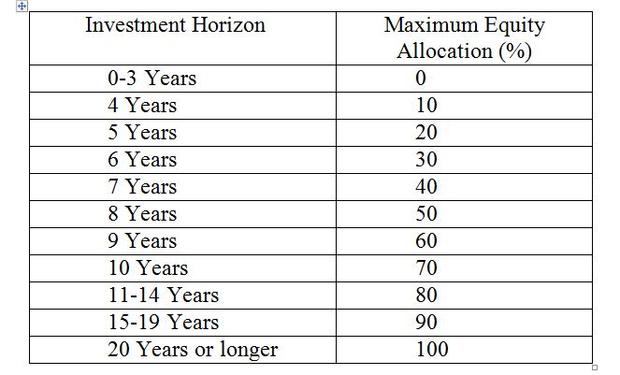

Let’s begin with the issue of the investment horizon -- the total amount of time an investor plans to hold a security or portfolio. The longer the horizon, the greater the ability to wait out the inevitable bear markets. In addition, the longer the investment horizon, the more likely equities will provide higher returns than fixed-income investments.

The following table provides a guideline for this part of the ability to take risk. As always, keep in mind that this table is just a rule of thumb, and no one solution works for everyone. It should be used as a jumping off point.

An investor’s ability to take risk is impacted by the stability of their earned income. The greater the stability of earned income, the greater the ability to take the risks of equity ownership. For example, a tenured professor has a greater ability to take risk than either a worker in a highly cyclical industry where layoffs are common or an entrepreneur owning a business with cyclical earnings. The tenured professor’s earned income has bond-like characteristics. All other things being equal, she has more ability to hold equity investments. The entrepreneur’s earned income has equity-like characteristics. He should hold more fixed income investments.

A third factor impacting the ability to take risk is the need for liquidity. The need for liquidity is determined by the amount of near-term cash requirements as well as the potential for unanticipated calls on capital. The liquidity test begins by determining the amount of cash reserve one requires to meet unanticipated needs for cash such as medical bills, car or home repair or job loss. Financial planners generally recommend a cash reserve of about six months of ordinary expenses.

The fourth factor impacting the ability to take risk is the presence (or absence) of options one can exercise should a severe bear market create the risk the investment plan will fail. Options may include delaying retirement, taking a part time job, downsizing the current home, selling a second home, lowering consumption or moving to a region with a lower cost of living. The more options, the more risk one can take. However, you should not consider an option such as moving to a location with a lower cost of living unless you are actually prepared to take that action.

Editor's Note: Some material for this article was adapted from the author's book, “The Only Guide You’ll Ever Need to the Right Financial Plan.”

You can try out CBS MoneyWatch's new online asset allocation calculator.