Businesses ramped up hiring in April as U.S. economy regained speed

Employers added a robust 211,000 jobs in April, a sign the U.S. economy is strengthening after meager growth in the first three months of the year.

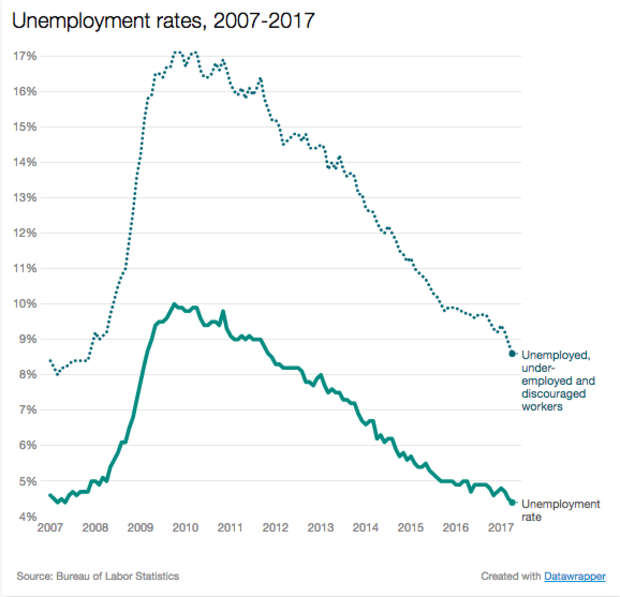

The nation's jobless rate ticked down from 4.5 in March to 4.4 percent, the lowest level since May 2007, the U.S. Labor Department said Friday. A broader measure of unemployment, which counts unemployed people, discouraged workers and those working part-time who can't find full-time work, also dropped to a nearly 10-year low, at 8.6 percent.

By industry, the biggest payroll gains were in leisure and hospitality, which added 55,000 jobs, and health care and social assistance, which added 36,800. The retail sector, which was up by 6,300 jobs in April, has lately been a drag on overall job growth, with 14 companies this year announcing closing or liquidation. A total of 56,000 retail jobs were lost in February and March.

Some analysts had raised concerns about a possible slowdown after a disappointing March job report and first-quarter GDP estimates that showed growth slowing to a glacial 0.7 percent. Indeed, the March figures were even worse than initially estimated, with the Labor Department revising down jobs added to a mere 79,000.

But the Federal Reserve on Wednesday dismissed the first-quarter weakness as "transitory," predicting that the economy would gain speed over the rest of the year. With stronger-than-expected hiring in April, the central bank is on pace to raise interest rates when it meets again in June.

"The month-to-month numbers are unreliable, but what will get the Fed's attention is that the unemployment rate has fallen from 4.8 percent in January to 4.4 percent just three months later," Ian Shepherdson, chief economist at Pantheon Macroeconomics, said in a note. "Fed hawks will now be even keener to see rates rise further, despite the leveling-off in hourly wage growth in recent months."

The official unemployment rate has hovered under 5 percent for a year. But although most economists think the labor market is at, or approaching, full employment, trouble spots remain.

Wage growth in April slowed down from its pace earlier in the year, rising at 2.5 percent annually, to an hourly average of $26.19. That's below the 3 or 4 percent growth typically seen in prior recoveries.

The number of people who are sitting out work altogether remains historically high. The labor participation rate -- the portion of the population that is either working or available to work -- was 62.9 percent in April. It's been at or below 63 percent for three years, a rate that was last seen in the late 1970s. In part, that reflects America's aging population, as older people exit the workforce.

"There is room for [participation] to increase, but it's not going to go back to where it was before," said Gus Faucher, chief economist of the PNC Financial Services Group, ahead of the jobs report. "It's an older workforce, and more people are not interested in working."

The rate is likely to remain low for the near future, economists say, as more baby boomers retire and many young people postpone their first jobs to pursue an education. The drop in younger people working, in particular, comes in part from the high costs of living coupled with sluggish wage growth, said Lindsey Piegza, chief economist at Stifel Fixed Income.

"There's a lack of motivation among some of the younger Americans, who just spent the last four or six years earning a college degree at a hefty price, and then can't find a job above minimum wage," she said. "And a lot of women are saying, 'When you look at the rising cost of childcare compared to what I can earn in the marketplace, why am I forgoing staying at home with my children?'"