Another weekend of cliff-hanging drama for Greece

Markets have been enthralled by the ongoing standoff between Greece and its creditors over the last few weeks, resulting in a series of over-the-weekend dramas. Each Friday, investors never really knew where things would stand when futures reopened for trading the following Sunday night. Now, it appears we're in for another weekend nail-biter.

Two weeks ago, it was the fate of what was then billed as last-ditch bailout negotiations. When that didn't go so well, it resulted in Greek Prime Minister Alexis Tsipras calling for a referendum vote on proposed austerity measures and the European Central Bank freezing its support of Greece's financial system. Greece then closed its banks and imposed capital controls and deposit withdrawal limits.

Last weekend, the high drama was at polling places across Greece: Would Greek citizens vote for or against the bailout proposal? A "no" vote was widely seen as increasing the risk of a Grexit (Greece abandoning the euro currency) and restoration of the Greek drachma.

Now, despite the "no" vote, Athens has submitted a proposal to its creditors that looks remarkably similar to the plan the Greeks rejected at the polls. This concession is a bid to reopen talks ahead of what's been billed as a "final" deadline Sunday for Greece to secure additional rescue funds in order to reopen its banks next week and meet a do-or-die debt repayment to the European Central Bank on July 20.

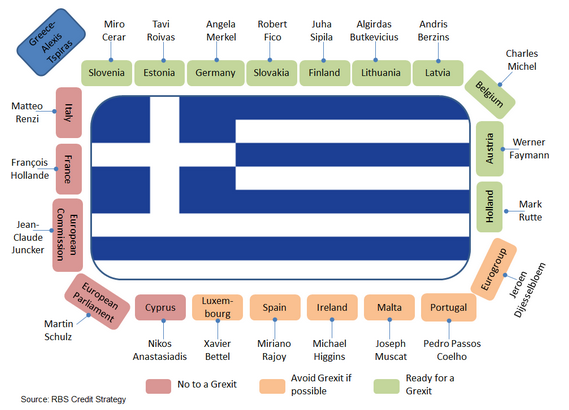

The situation clearly has many moving parts and remains fluid. First up, the Greek parliament will need to vote in approval of the latest proposal, which cannot be assured because members of Tsipras' own Syriza Party accuse him of ignoring the will of the voters.

The package Greece submitted, if accepted, would amount to a third bailout program asking for more than 50 billion euros in rescue funding in exchange for 13 billion euros in new austerity measures.

There's also a fascinating human element, with former Greek Finance Minister Yanis Varoufakis pushed out this week -- despite winning the referendum vote he wanted -- in an apparent backroom coup to appease Greece's hardliner creditors. Varoufakis apparently had enough, with the Greek press reportedly catching him leaving Athens for his wife's vacation home (despite his status as an elected member of parliament) on this critical weekend.

Before he left, Varoufakis penned an op-ed in The Guardian blaming Germany's finance minister for actively working to push Greece out of the euro in order to, in his words, "...put the fear of God into the French and have them accept his model of a disciplinarian eurozone."

The well-connected Ambrose Evans-Pritchard at The Telegraph, whose on-the-record interview earlier this week with Varoufakis -- in which he said the country was considering issuing California-style IOUs as a parallel currency -- was fingered as part of the reason Varoufakis was asked to resign. Evans-Pritchard believes Tsipras never thought he would win a "no" vote in the referendum and is now trapped by his own success.

With Greece retreating on austerity, the crux of the standoff now focuses on whether Germany and other hardliner creditors will accept a Greek debt write-off as a way to get the country back on a unsustainable fiscal footing. This could be done by reducing principal balances, extending maturities or lowering interest rates -- something both the International Monetary Fund and the U.S. Treasury have been calling for.

Any deal would need to pass the individual national parliaments of eurozone countries, drawing out the crisis that started in late 2009 even further. With Greece's economy stalling as banks remain closed, supply chains grind to a halt, and factories closing, the country simply can't wait much longer. Nor can the possibility of a political crisis and protests in Athens be dismissed as Tsipras essentially ignores the result of the referendum he called for.

Without a deal this weekend, Alberto Gallo at RBS believes Athens will be forced to turn to depositor "bail-ins" and currency IOUs to merely survive and keep the hope of staying in the euro alive.

The cost of failure? A Grexit, in his estimation, would cost Greece's public and private bondholders $253 billion while slashing 4.4 percent off Greece's economy next year.

How's that for high drama?