An IRS rule that can aid your retirement income strategy

The year-end deadline for the IRS required minimum distribution (RMD) is looming for retirees age 70½ and older. These IRS rules require you to withdraw minimum amounts from traditional IRAs and work-based savings plans like a 401(k). If you don't take out at least the minimum required, any shortfall in your annual withdrawal is subject to a 50 percent penalty -- so it's smart to make at least the minimum withdrawal to avoid this penalty.

If you've never had to deal with this requirement before, you might think it provides a sort of roadmap for making appropriate withdrawals from your retirement savings. However, the RMD wasn't actually intended to be used that way. Instead, its main purpose is to subject your savings to income taxes because you didn't pay taxes on the money when you contributed it to your retirement account. There's one exception: The RMD also applies to withdrawals from Roth 401(k) accounts, even though these withdrawals aren't included in your taxable income. RMDs don't apply to Roth IRAs.

Still, many retirees use the RMD to determine the annual amount they'll withdraw from their savings. Is this a reasonable strategy? The answer depends on your goals and objectives. Let's take a look.

How the RMD works

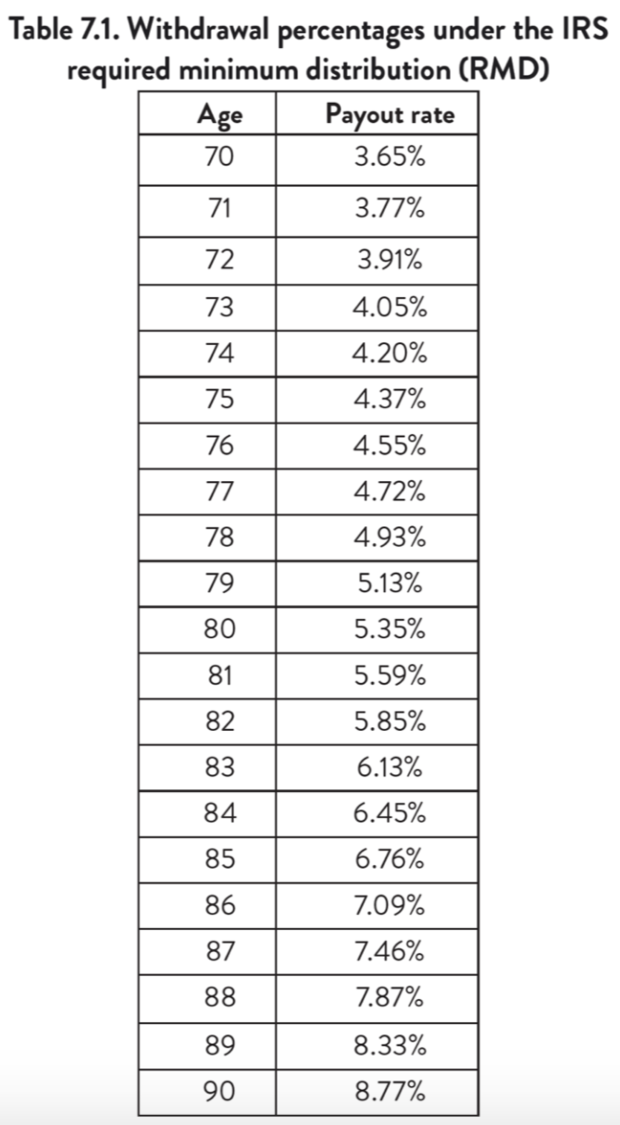

The RMD calculates the minimum withdrawal amount by taking your account balance on Dec. 31 and dividing it by your life expectancy, as outlined in IRS Publication 590-B. To make things easier, the RMD rules can be converted into a series of withdrawal percentages, as shown the following table from my recent book, "Retirement Game-Changers."

For example, suppose you have $100,000 in retirement savings on Dec. 31 and you're subject to the rules for the first time because you attained age 70½ this year. Your RMD would be $3,650 (that's 3.65 percent of $100,000). If you want to use the RMD methodology to determine withdrawal amounts before age 70½, you can use a simple withdrawal rate of 3.5 percent.

The RMD does have a few features that represent best practices for withdrawing from invested savings. First, the method adjusts your withdrawal each year to reflect investment returns -- favorable returns can boost your withdrawals, whereas poor returns will reduce them. This is more desirable than withdrawing a fixed amount each year, ignoring investment returns.

Second, the withdrawal percentage increases each year, automatically adjusting for your remaining life expectancy, which reduces as you age.

One significant advantage of the RMD is that most IRA or 401(k) plan administrators can easily determine the right amount for you, so you don't have to make complicated calculations. Many will also automatically pay the RMD to you in the frequency you elect, such as monthly, quarterly or annually.

One good strategy could be to withdraw the total RMD amount from your invested assets as soon as possible after the beginning of the calendar year and instruct your IRA or 401(k) administrator to transfer it electronically to your checking or savings account. You can withdraw amounts as needed throughout the year to pay for your living expenses. With this approach, your withdrawal amount won't be subject to investment volatility throughout the year.

A two-step approach

A recent study by the Stanford Center on Longevity systematically compared 292 different retirement income strategies, including optimizing Social Security benefits, systematic withdrawals from invested assets and purchasing a lifetime annuity. It came up with what it calls the Spend Safely in Retirement Strategy as a strong contender for a retirement income strategy to consider. It has two steps:

- Optimize Social Security through a thoughtful delay strategy.

- Use the IRS RMD to determine annual withdrawals, together with investing your savings in a common stock index fund, target date fund or balanced fund.

This strategy compared favorably to more complex strategies.

Still, using the IRS RMD to determine your annual withdrawals has a few disadvantages:

- The withdrawal amount can fluctuate significantly from year to year if you have a significant allocation to stocks. Whether this is a problem depends on how much you're relying on your withdrawals to meet your basic living expenses. Some people might not tolerate a reduction in their spending due to a declining stock market, or worse, a crash. If that's the case, consider investing a portion of your savings in a low-cost fixed-income annuity that isn't subject to investment volatility.

- You may want to withdraw more than the RMD, for example, if you want to travel more during the early part of your retirement when you're still active and healthy. In that case, you can set aside a "fun bucket" that equals an estimate of the extra amounts you want to spend in your go-go years. Suppose you want to spend $5,000 per year on travel for the first 10 years of your retirement. You would then set aside $50,000 from the rest of your retirement savings, withdraw the RMD from that amount and also withdraw $5,000 from your "fun bucket."

No matter what you decide to do, you should spend the time it takes to develop a thoughtful retirement income strategy that will last the rest of your life, no matter how long you live and no matter what happens in the stock market. Then enjoy your retirement.