After the historic market rebound, what's next?

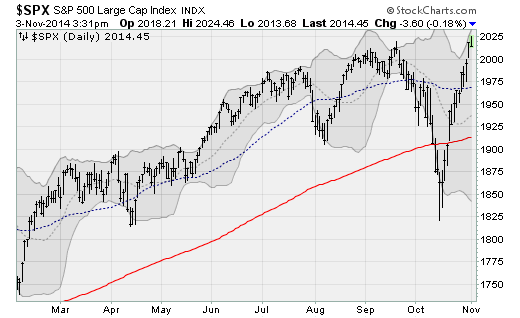

Now that we have officially left October and its wild Wall Street ride behind, it's worth taking a quick look back at the month and use that as a lens for previewing what November might have in store. For sure, the volatile month ended on a rather positive note. Large-caps set new record highs on Friday as Japan kept the promise of cheap money stimulus alive even as the U.S. Federal Reserve put an end to its two-year-old QE3 bond-buying program.

The solid finish stood in stark relief to the fear and nervousness seen earlier in the month -- especially because October has a spooky reputation on Wall Street given that the market crashes of 1929 and 1987 both happened with Halloween in the air. But this year, October even ended up being the best month for beaten-down small-cap stocks in 15 months.

The rebound was powerful and persistent, with the S&P 500 trading more than 0.5 percent above its five-day average for the month's last two weeks according to the folks at SentimenTrader. The only other times this happened coming off a six-month low were the bear market bottoms in 1982 and 2002. Yet the peak-to-trough decline in the S&P 500 was worth less than 10 percent.

In other words, such a powerful rebound off such a mediocre pullback has never happened before. So now that we're into November, with a fairly muted first day of trading, what comes next?

The stage looks set for further gains -- at least in the near term. This October was the eighth time the S&P 500 dropped at least five percent only to reverse and close in positive territory. The S&P 500 has been positive in November five of the previous seven times, with an average gain of 2.1 percent. And December has also been positive five times, with an average gain of 0.7 percent.

Another tailwind for the weeks ahead comes Japan's move to keep the flow of cheap money stimulus going as the Fed backs off.

Specifically, the Bank of Japan surprised the market last week by boosting its Quantitative and Qualitative Easing, or "QQE," program from an annual purchase rate range of 60 trillion to 70 trillion yen previously to 80 trillion yen (about $700 billion). The BOJ also increased the amount and widened the types of equities eligible for purchase. For scale, if the Fed were to do something similar, given the size of the U.S. economy it would be worth $3 trillion a year in purchases.

Traders celebrated the move because of the popularity of the yen carry trade -- something I've discussed before -- and how that encourages computer trading algorithms and macro hedge funds to pile in. Japan's actions slammed the value of the yen lower against the dollar, benefiting these yen carry positions.

In fact, the yen-dollar exchange rate dropped to levels not seen since 2007.

But as we advance into November, some concerns are on the horizon, including how Wall Street reacts to the likely GOP takeover of the Senate in Tuesday's midterm elections. It could bring back bad memories of the fiscal cliff, the government shutdown and threats of debt defaults.

Moreover, the October jobs report to be released on Friday and the publication of the October Fed meeting minutes later this month could remind investors that Fed policymakers are sticking to their mid-2015 timing window on the first short-term interest rate hike since 2006.

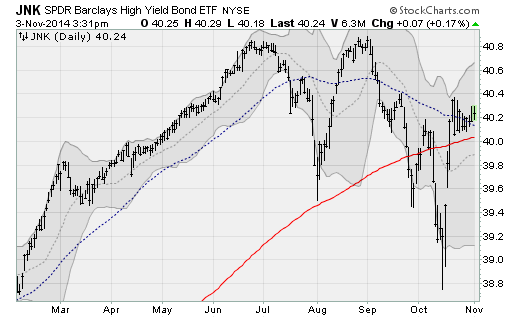

Whenever this discussion has attracted attention in the past, the high-yield bond market was the first to show signs of stress. That'll be another area worth keeping an eye on as we move through November and toward year-end.