1,000% loans? Millions of borrowers face crushing costs

Last Christmas Eve, Virginia resident Patricia Mitchell borrowed $800 to help get through the holidays. Within three months, she owed her lender, Allied Cash Advance, $1,800.

On the other side of the country, Marvin Ginn, executive director of Native Community Finance, a small lender in Laguna, New Mexico, reports that some customers come to him seeking help refinancing loans from nearby payday lenders that carry annual percentage rates of more than 1,000 percent.

"You get a person with low income into a loan with that kind of interest and it's like, 'Holy mackerel!' How do they ever get out of it?" he said.

Welcome to the world of payday loans. If the 2008 financial crisis that upended the U.S. banking system led to some reforms for consumers, this remote corner of the financial industry remains rife with problems. Regulation in many states is loose and enforcement weak. That environment has left millions of Americans trapped in a financially crippling cycle of debt that many struggle to escape.

Change may be on the way. The federal Consumer Financial Protection Bureau (CFPB) is expected in May to propose national standards for payday loans, which for now are regulated only at the state level. Striking the right balance will be critical, threading the needle so borrowers are protected from predatory lenders without wiping out the only source of capital available to many low-income Americans.

Legal loan-sharking?

Payday lending is big business. Every year, roughly 12 million people in the U.S. borrow a total of $50 billion, spending some $7 billion on just interest and fees, according to The Pew Charitable Trusts. An estimated 16,000 payday loan stores are spread across the U.S., with hundreds more such lenders operating online.

Payday loans and so-called auto title loans, which are secured by a borrower's vehicle, are marketed as being helpful for financial emergencies. Allied Cash Advance, for example, touts its payday loans as a way to "bridge the gap" after a car accident, illness or other unexpected expense leaves people temporarily low on funds.

In fact, the typical borrower uses payday loans for rent, utilities and other recurring expenses, said Nick Bourke, director of the small-dollar loans project at Pew, which is pushing for tougher payday lending rules nationally. And while these loans are usually due in two weeks, the sky-high interest rates and heavy fees make repaying them on time all but impossible.

"The No. 1 problem with payday loans is they're unaffordable," said James Speer, an attorney and executive director of the Virginia Poverty Law Center. "They're really not even loans at all -- it's just a way of sucking people into what we call a debt trap. It's more like loan-sharking."

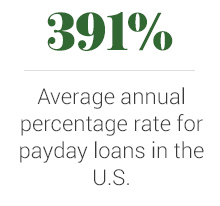

Most payday loans are exorbitantly expensive. The average annual percentage rate, or APR, on the loans is 391 percent, which comes to $15 for every $100 borrowed, according to Pew. But lenders in states without a rate cap often charge far more.

In 2014, for instance, the New Mexico Supreme Court heard a case in which two payday lenders peddled small "signature" loans that carried APRs of up to 1,500 percent. These loans required only a borrower's signature, along with verification of identity, employment and home address, as well as personal references.

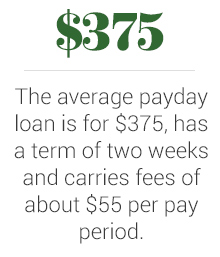

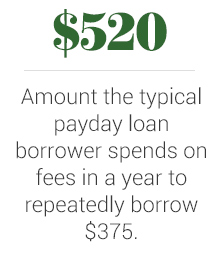

Lenders' origination fees and other charges further push up payday loan costs. The average fee for storefront payday loans amounts to $55 every two weeks, Pew's data show. That means borrowers typically pay more than $430 the next time their paycheck arrives, often leaving them struggling to cover their living expenses until the following payday.

As a result of these costs, instead of quickly borrowing and repaying the money, most payday loan users end up in debt for months at a time, repeatedly taking out loans as they run low on cash.

"The longer that payday lenders can keep flipping the loan, the more money they make," Ginn said.

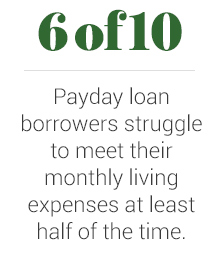

Another major problem, critics say, is that payday firms don't issue loans based on a person's income or ability to repay the money, like an ordinary bank loan. As a result, loans typically end up consuming well over a third of borrowers' total income. What lenders can do in many states, by contrast, is directly collect payment for a loan from a person's bank account.

The results are predictable. Borrowers often end up incurring what the CFPB calls "hidden" costs. Those include bank penalties for overdrafts and insufficient funds when payday lenders repeatedly try to debit a person's account to collect payment.

"It's a very dangerous practice because they debit your account whenever they feel like it," Speer said. "And if you overdraw your account, it causes all sorts of problems. Your rent doesn't get paid or you bounce a check at the grocery store, and then people get a letter [from a collection agency] saying they're going to prison for writing bad checks."

A spokeswoman for the Community Financial Services Association of America (CFSA), a trade group that represents payday lenders, defends the industry's practices, insisting that the group's members do take a borrower's ability to repay into account. Citing survey data, she also said the vast majority of payday borrowers weigh the risks and benefits before taking out a loan, arguing that most are aware of the overall financial costs.

"Where are you going to go?"

Mitchell, 44, a single mother who recently moved to North Carolina from Virginia, said that between January and February she racked up interest charges of nearly $582 and additional fees of $115 on her original $800 loan. Several hundred more dollars have piled up since then, she said, expressing concern that the debt would scuttle a job she recently applied for given that many employers review a candidate's credit record.

Many borrowers are well aware that payday loans are a bad deal. Near Laguna, New Mexico, in a cluster of villages known as Laguna Pueblo, the average household income for the roughly 8,000 members of the Laguna, Mesita, Paraje and other local tribes hovers around the poverty line. Residents have few low-cost options when it comes to a short-term loan.

Such concentrations of poor people are an invitation for payday lenders to do business. Gallup, New Mexico, which lies in the Navajo reservation, has about three payday lenders for every fast-food restaurant, said Ginn, whose federally certified lending firm caters to Native Americans.

"I've seen it where they'll borrow from one payday lender to pay another one, and then borrow from a third to pay the other two," he said of some of his customers at Native Community Finance. "They're aware of the cost, but access to capital on the reservation is so limited that they borrow anyway. If you need the money and the only access to capital is a predatory lender, where are you going to go?"

Not all states are so permissive. While 28 states allow payday loans with APRs of 391 percent or higher, the rest put lower caps on fees, along with other limits, or ban payday storefront lending altogether.

A model for change?

One state, Colorado, has gone to further lengths to protect payday loan borrowers without stamping out the practice altogether. A 2010 law replaced two-week payday loans with six-month installment loans capped at $500. The maximum allowed APR, at 45 percent, is nearly two-thirds lower than the average rate before the law, while other fees are limited.

The measure has reduced payday loan defaults, and three-quarters of borrowers are able to pay off loans early, according to Pew. While half of storefront payday lenders have since closed in the state, remaining firms have gotten more business, the group found.

"Colorado proves it's possible to reform payday lending in ways that benefit borrowers," Bourke said.

A spokesman for Ace Cash Express, a national provider of payday, title and installment loans, along with other financial services, said it closed nearly half of its 85 stores in Colorado after the 2010 law as its profits fell and the company cut costs. It now turns away more customers seeking small-dollar loans in the state, approving three out of 10 loan applications.

"Those borrowers who can still get loans like the new system because they don't have to pay the loan back all at one time," the spokesman said in response to emailed questions. "The old system worked very well for those who could pay the loan back quickly, less well for those who couldn't. So for many in Colorado, an installment loan is a great relief, and our customers seem happy about that."

Market solution

One complaint about the payday lending industry is that it lacks competition, making it hard for borrowers to shop around for the best terms. Doug Farry wants to change that.

A former TurboTax executive, he's the co-founder of Employee Loan Solutions, a program that lets employers offer small loans to their workers. Called TrueConnect, the product enables loans of up to $3,000 at an APR of 24.9 percent. That amounts to charges of $120 per year on a $1,000 loan.

To ensure people don't get in over their heads, loan amounts are limited to 8 percent of gross pay, compared with upwards of 39 percent in some states. Loans, which are made through Minnesota-based Sunrise Banks, are repaid through automatic payroll deductions.

"We made it so our borrowers would be able to repay their loans in small increments spread out over a year," he said. "That way they don't get caught in a debt trap."

Unlike payday lenders, TrueConnect also reports to credit bureaus when borrowers make payments. That can be especially valuable for people trying to rebuild their credit.

A number of public and private employers in California, Minnesota, Ohio and Virginia are now offering TrueConnect, which is designed to be rolled out as an employee benefit and which Farry said comes at no cost to the organizations that use it.

Employee Loan Solutions' "business model is one we can definitely use in New Mexico," said Rep. Javier Martinez, a Democratic member of New Mexico's state legislature who is pushing to crack down on payday lenders in the state. "It's a safe alternative, and it's a fair alternative.

What the feds can do

Such financial products can help, but they're likely not enough. Making small loans to subprime borrowers presents serious business challenges, including a high incidence of fraud, significant customer-acquisition costs and the complexity of dealing with varying state rules.

Those obstacles have largely deterred other types of lenders, such as credit unions, from entering the market.

That puts a premium on the forthcoming rules from the CFPB, which reformers hope will set national standards for payday and other small-dollar loans. Perhaps most urgent, Bourke said, is to put pressure on payday lenders to ensure that borrowers can repay loans. Loans also need to be more affordable, and lenders must be discouraged from trying to collect payment from borrowers' bank accounts in ways that rack up fees.

Bourke also urged the agency to set standards for short-term installment loans that many lenders have started pushing in recent years amid mounting scrutiny of payday loans.

"One problem we might see with the CFPB loan rules is that they're not bold enough in drawing really clear lines, and that could lead to bad products coming onto the market at the same time that low-cost lenders are discouraged by ambiguity [in the draft rules] from introducing products."

Ace Cash Express said it works with customers by converting loans to a payment plan with no additional fees or interest. "We don't lend to people whom we believe can't pay us back. No one should," the company's spokesman said.

But he acknowledged that some Ace Cash borrowers repeatedly roll over the same loan. The company wants regulators to let lenders convert shorter duration loans into installment loans, as Colorado does.

"What we don't want are regulations that appear to be reasonable but are really designed to make lending impossible," the spokesman said.

Echoing such concerns, the CFSA said setting federal standards requiring lenders to take a borrower's ability to repay a loan into account would drive most payday firms out of business.

The wrangling over the rules of the road for payday lending will continue for some time to come. Even after the CFPB issues its proposal, it could take a year or more to pass a final rule.

For her part, Mitchell said she's done with payday loans, noting that she tells her 12-year-old daughter to stay clear of the products.

"I would starve before getting another payday loan," she said. "I just think it's robbery."