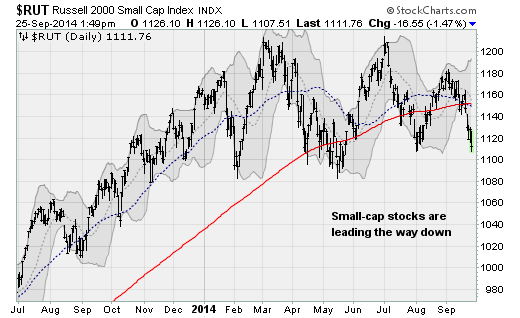

Why stocks are getting crushed

After drifting to new highs last week with ease and grace, stocks fell with a thud Thursday. The Dow Jones industrial average plunged 264 points. The S&P 500 fell below its 50-day moving average, a major technical support level that was last breached in July.

If this feels a little unusual, well, that's because it is: The market has been in the midst of a rare period of ultra-low volatility, encouraging confidence and complacency. Bearish sentiment had dropped to levels not seen since 1987. And the S&P 500 hasn't suffered the indignity of a serious pullback, enough to test its 200-day moving average, since 2012. Yep, it's been that long.

The catalyst for the smooth and easy rise, as I explored back in May, has been the support the stock market has enjoyed from ultra-low borrowing costs in the corporate debt market, which in turn has been supported by the Federal Reserve's ongoing QE3 bond purchase program. First announced in September 2012, the Fed has shoveled high powered cash into the financial system helping to take the monetary base from $800 billion before the recession to more than $4 trillion now.

But it's coming to an end. We had a little bond and stock market freak out in the spring of 2013 -- dubbed the "taper tantrum" -- after former Fed chairman Ben Bernanke hinted that given the strengthening economy, QE3 would soon start drawing to a close. Bernanke backed off, frightened by the market's response (which was blamed on communication errors) and didn't start tapering until last fall.

Investors were encouraged by other stuff, including the Fed's promises to hold short-term rates near zero percent for as long as possible, hot IPOs like Alibaba (BABA) and GoPro (GPRO), and the Ukrainian cease fire.

But suddenly, the end of QE3 looms. The final taper will likely happen at the Fed's October meeting, making November the first month the Fed is not making long-term bond purchases in more than two years. Moreover, we're fast approaching the window of the Fed's first short-term interest rate hike -- Wall Street is penciling in the middle of 2015 -- something that hasn't happened since 2006.

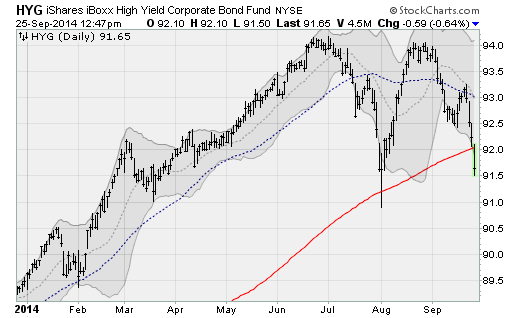

Now another rate tantrum is underway. You can see this in the way high-yield corporate bonds are coming under serious pressure with the iShares High Yield Corporate Bond Fund (HYG) dropping below its 200-day moving average for the first time since August 2013.

Other catalysts are being blamed, including weaker-than-expected durable goods and PMI services reports on the economic front. Apple (AAPL) is dragging down the tech sector in a big way due to software bugs and the "Bend-gate" problem related to users reportedly bending the iPhone 6 Plus model by simply leaving the device in their pockets while sitting. Others point to the historic record of September being a difficult month for stocks. And I've even seen the old "sell on Rosh Hashanah, buy on Yom Kippur" excuse trotted out.

Whatever the trigger, the selling looks set to continue based on how weak the market's internals have become. I'm talking about breadth, or how many stocks move higher. Wednesday's head fake bounce higher is illustrative: Although the major averages posted their best one-day gain since August, there were just 60 new one-year highs vs. 263 new lows.

Currently, just 70 percent of the stocks in the S&P 500 are in uptrends vs. 85 percent back in July when stocks were first trading at these levels.

Given the end of the Fed's cheap money, the need for a washing away of market excesses, and the violation of support levels, stocks should keep drifting lower into October before investors will need to contend with the next big catalyst: The sure-to-be-contentious mid-term elections.