For retirees, myths collide with reality

Retirement has long been idealized in American culture as our "golden years," a reward for decades of labor filled with travel, warm family moments and other opportunities for fulfillment.

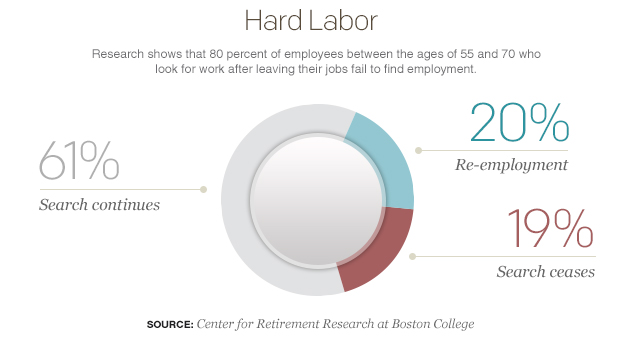

But for the vast majority of Americans, that dream is losing its luster. For starters, more people are working in retirement, blurring the definition of what it means to retire. Increasingly, retirement also reduces financial security. Americans are retiring today with more debt and higher healthcare costs, while increasingly bearing the burden of nursing often meager savings over their remaining years.

Even if people nearing retirement do manage to build a sizable nest egg, they often have much less investment income because of the low interest rates that the Federal Reserve has encouraged since the 2008 financial crisis. If employees were lucky enough to have a retirement plan at work -- and only two-thirds of Americans do -- it's likely they haven't saved enough to maintain the same standard of living over what could amount to 30-year retirement.

"Work more"

Giovanni Perrupato, a cobbler in Hoboken, New Jersey, is a prime example of the inherent contradictions that are changing the very meaning of retirement.

At 68, he considers himself retired, yet works six days a week. Before officially retiring in 2011, Perrupato's plan was to keep working with his sons in the shop he started with his father in the 1960s, while shifting to a less strenuous schedule. But ordinary financial strains, along with some unexpected expenses over the years, have forced him to change his retirement plans.

"I thought I was going to take it easy, but now I see I got to work more," he told CBS News.

Given the recession and slow-growth economy of recent years, today's retirees are also more likely to have ongoing financial commitments -- adult children that need financial support, ailing parents to care for, and mortgage and credit card debt of their own.

As a result, only 18 percent of U.S. workers are very confident of having enough money to live comfortably during their retirement years, according to a March survey by the Employee Benefit Research Institute (EBRI). That's down from a peak of 37 percent 20 years ago.

Rebecca Hall, a financial advisor with Ameriprise for the past 17 years, has seen a "shift in perception" over time that reflects these emerging realities. Clients used to come to her to find out when they could afford to stop working. Today, her clients are more likely to seek advice on how to downshift to semi-retirement. They want to find out when they can "gradually phase out of full-time, high-stress jobs to eventually not working," Hall said.

For some retirees, that means continuing to work -- assuming they manage to find a job. A recent Gallup poll found working Americans say they plan to retire, on average, at 66, or four years above the self-reported retirement age for currently retired people. Baby Boomers who said the don't have enough money in another Gallup report, reported they plan to work until 73.

"Golden years" myth

Changing views about retirement aren't only a matter of Americans learning to cope with financial restraints. The fact is, traditional notions of retirement were always a bit of a myth. "It was really a marketing pitch that included golf and travel," said Steve Vernon, a research scholar for the Stanford Center on Longevity and a contributor to CBS MoneyWatch.

The retirement myth grew out of series of policies instituted after World War II to move older workers out of companies to make room for veterans, and eventually baby boomers. In the 1970s and 80s, companies used pensions as a way to encourage workers to retire early. "But not that many people got to take advantage of it," Vernon said.

Even in their heyday, defined benefit plans -- which provide a guaranteed stream of income and which have largely been supplanted by riskier 401(k) plans -- were no panacea.

When pensions were at their peak in 1992, only about 43 percent of retirees received income from the plans. And if surveys in the early 1990s showed the most Americans were optimistic about their retirement prospects, that actually reflected "gross overconfidence," said Dallas Salisbury, president and founder of EBRI.

"There's a tendency to look back at the golden days of defined benefit plans," added Anthony Webb, a senior research economist at Boston College's Center for Retirement Research. "These plans undoubtedly worked in low-inflation environments for people who worked their whole lives for a single company. But they didn't work well in the past for people who weren't covered by them or who hopped from job to job. And they may not be appropriate for today's more mobile workforce."

Today, EBRI's research shows, the retirement savings of people participating in employer-sponsored plans for 20 to 30 years is roughly equivalent to what the traditional pensions would have provided. Likewise, Social Security still replaces roughly the same amount of income for retirees as it did when pensions were more common -- a third or less for higher earners and the great majority of income for lower earners.

Americans have always been short on retirement savings, Salisbury said. The main difference today is the heightened anxiety around how retirees can make those savings last, he explained. With 401(k) plans, two-thirds of individuals collect their funds as a lump sum when they retire rather as a steady stream of income.

"Now people have to figure out how much they can spend each month, and they worry about what happens if they live to 100," Salisbury said. "That almost guarantees two-thirds of retirees have higher stress levels."

Is retirement overrated?

The irony of the retirement myth is that even those who managed to turn it into a reality -- moving to a golf community, say, or a seniors' resort in the sun -- often didn't even enjoy it. A recent AARP study found that the great majority of older Americans -- 71 percent of people age 50 to 64 -- want to stay in their homes and communities.

To that end, whole industries also are cropping up, along with job opportunities for active seniors, to help Americans "age in place," as the concept is known.

Although policy experts voice concern about many Americans' inadequate retirement savings, they are more sanguine about the changing nature of retirement itself. They see signs that more individuals are approaching retirement with realistic goals and are doing more to prepare.

"Research shows that if you work longer, you are healthier, happier and more mentally fit," Vernon said, adding that greater participation in the workforce by older people can also benefit the broader economy.

Perrupato, a vigorous, bongo-playing small business owner, may typify the new retiree. While he admits he isn't having the retirement he imagined, asked if he would have changed anything, he told CBS News, "I maybe would have saved a little more money, but that's about it." Overall, he said, "I can't complain because I'm having a good life."