Danger zone: America's retirement system is breaking down

In a special report launching today, Eye on America: Retirement, CBS News explores the changing nature of retirement and how to prepare for the future.

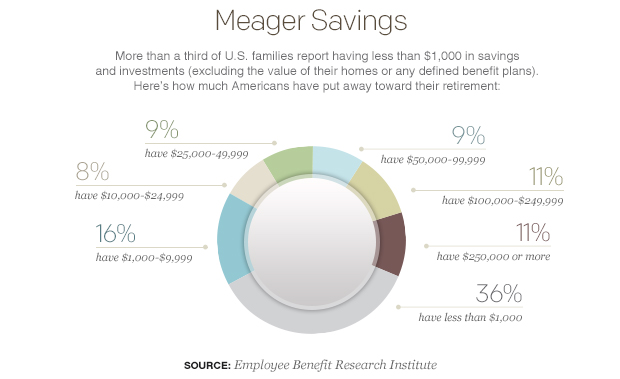

Roughly half of all U.S. families have no money set aside for retirement, Federal Reserve data show. Not a cent. But even that alarming savings deficit doesn't fully capture the emerging socioeconomic crisis facing what is, after all, a rapidly graying nation.

That's because even Americans who work diligently to prepare for their later years are falling behind, thwarted by a confusing, patchwork system that has placed the burden of saving for retirement squarely onto individuals. As a result, only 18 percent of U.S. workers say they are very confident of having enough money to live comfortably during their retirement years, according to the Employee Benefit Research Institute (EBRI).

"What has happened over the last 20 or 30 years is a transfer of risk from employers to employees," said Anthony Webb, senior research economist with Boston College's Center for Retirement Research.

But shouldn't people accept responsibility for planning their financial future? Well, yes and no. Most of us recognize the importance of living within our means, while millions of Americans already divert part of their income into an employer-sponsored 401(k), IRA and other accounts to ensure they'll have enough to live on in retirement.

Yet millions more find it hard or impossible to save, largely for reasons beyond their control. They are casualties of broad economic, social and other forces, from high unemployment, stagnant income and spiraling health care costs to eroding labor protections and rising income inequality. Behind these currents, as always, are political choices we make as a nation, along with the deep-pocketed special interests that steer public policy in ways that may not align with the common good.

The danger? In the years ahead, a growing segment of the U.S. population could see their living standards erode as their retirement savings -- those who have any -- run dry.

Hue Galloway, 63, typifies the struggles many people face preparing for retirement, even those who have tried their best to save.

The New Britain, Conn., resident had both a 401(k) and IRA account, along with additional savings, as a field technician for TicketMaster. But when the father of six was laid off in 2008 after more than a decade with the company, his income plummeted. He looked for work for more than three years, but couldn't find a full-time job. A part-time position with a mailing company turned out to be a scam. Unable to pay his mortgage, his house was foreclosed.

At the time he was laid off, Galloway had some $130,000 in his retirement accounts. He had another $40,000 or so in a savings account, but he has had to spend those funds to make ends meet. Today, he lives almost entirely on Social Security, which amounts to $1,500 a month.

Compared with many Americans, of course, Galloway is fortunate -- he worked for a company that offered retirement benefits. As of 2010, only 51 percent of private-sector workers had access to a retirement plan at work, according to estimates by Robert Hiltonsmith, a policy analyst at Demos, a liberal-leaning think-tank. And that figure is decreasing, down 10 percentage points from a decade ago.

Perhaps even more troubling is the dearth of savings among people approaching retirement: Four of 10 Americans ages 55 to 64 have no money put away for retirement. For those in that age range who do have a 401(k), IRA or other retirement account, the median balance is $120,000, according to the Fed's most recent Survey of Consumer Finances. That isn't as much as it might sound -- for the typical household, that amounts to income of only $400 a month.

Median savings across all households with retirement plans is only $40,000, far short of what most retirees need to get by, let alone to maintain their standard of living.

And when families who lack a retirement plan are factored in, the numbers look positively dire. Overall, the median retirement account balance for all working-age households in the U.S. is $3,000, and $12,000 for near-retirement households, according to the National Institute on Retirement Security. Minorities are especially at risk, the nonprofit research group found: Three out of four black households and four out of five Latino households have less than $10,000 in retirement savings.

"We're already entering a crisis state, and it's going to get worse," Hiltonsmith said.

401(k): High costs, poor returns

By far the most common way employees save for retirement these days is through a workplace 401(k), which over the last three decades has supplanted pensions as the employer plan of choice. Here's the problem: As originally conceived, that's not what 401(k) plans were designed to do.

Created in 1978 as a minor part of a major tax law, 401(k) plans were intended to help well-paid corporate executives shelter income from taxation. Congress later decided to expand access to the plans to rank-and-file workers, and even then the idea was for such investments to merely supplement, not replace, ordinary pensions.

Critics point to a number of defects in 401(k) plans. The most serious, some experts say, is that they require individuals to manage their investments, exposing them to risks they lack the expertise to discern. That point was driven home during the financial crisis, when millions of people saw the value of their 401(k) holdings plunge.

"Employees are neither equipped nor trained to handle risk," Webb said.

Another strike is the high administrative, marketing, asset-management and other fees many financial firms charge for 401(k) plans. Hiltonsmith calculates that such fees diminish a person's nest egg by an average of about 30 percent. Webb comes up with a slightly lower figure, saying that relative to a low-cost index fund, an actively managed 401(k) reduces retirees' wealth by about 20 percent.

Notably, meanwhile, higher fees don't add up to better investment returns.

"If the fees on actively managed funds were buying better investment performance, then those fees might be money well spent," Webb said. "But evidence suggests that the average actively managed fund underperforms an index fund."

Finally, although stocks have shot up to record highs this year, boosting 401(k) balances, home prices remain well below where they were before the housing bust. For most people, the value of their homes matters far more to their retirement prospects than how the stock market is faring. This is especially true in the U.S., where the wealthiest 10 percent of the population owns more than 80 percent of stock holdings.

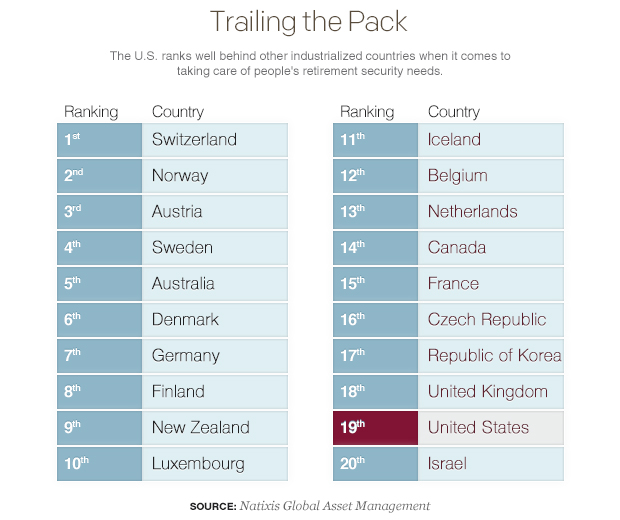

The shift from traditional pension plans to 401(k) plans may partly explain why the U.S. tends to fare poorly compared with many other industrialized countries around the world on measures of retirement security.

Investment firm Natixis Global Asset Management, which has more than $867 billion under management, recently evaluated 150 nations to see which do best in ensuring retirement security and meeting retirees' financial expectations. Examining criteria including health and health care quality, income and finances, and quality of life, the firm found that the U.S. ranks only No. 19, trailing countries such as Israel and the Czech Republic (see chart below).

Complexity breeds perplexity

Inadequate savings and high investment costs are only part of the story, however. In preparing for retirement, Americans also must navigate a system that is dauntingly complex.

Part of the difficulty is rooted in the nature of retirement planning itself, which is far more complex than, say, saving to buy a house or pay for college. Among many variables, it requires guesstimates about likely earnings at different career stages, assumptions about investment returns, assessments of the financial impact of having children and -- lest we forget -- some notion of how long you'll live.

In the public sphere, at least, there is Social Security, which workers can count on for a steady stream of income when they retire. But even that involves a tricky calculation about when to start taking payments, while benefit amounts are contingent on the vagaries of politics and federal budgeting. And Social Security benefits, which are generally assumed to replace roughly a third of the income that most retirees require, are inadequate on their own to make up for gaps in private retirement assets.

Indeed, roughly half of workers in the private sector lack access to any kind of employer retirement plan. And those who do participate in a defined-contribution plan face a bewildering array of possible investments. Numerous surveys over the years indicate that most employees are fuzzy on the returns they're getting on these assets and, at least until disclosure rules were tightened last year for 401(k) plans, largely in the dark about the often heavy fees they pay to participate.

"We have made it so complicated to save, and that's a problem even for Americans who are trying to do the right thing," said Tracey Flaherty, senior vice president of government relations and retirement strategy at Natixis Global Asset Management.

Spend less, save more?

Of course, cultural factors and individual judgment do come into play in planning for retirement. Although estimates vary on how much people should save, most experts say that to maintain their standard of living in retirement, a typical family needs to replace 75 percent to 85 percent of their pre-retirement income.

Yet many Americans just aren't disciplined enough to save, Flaherty said, contrasting consumers' willingness today to go into hock to finance their lifestyle with previous generations' aversion to debt.

"Saving is a bit like dieting," Webb added. "All of us understand the importance of being good, but we don't want to be good just yet."

Then again, squirreling money away is tough in wake of an epic financial crisis, when poverty has flared, income inequality surged and many people are losing their grip on the middle class.

Why wages matter

The housing crash slammed home prices, damaging what for a majority of retirees is their most important financial asset. But the biggest obstacle to putting money away -- one that long predates the financial crisis -- is that wages for nearly all Americans have been stagnant for more than 30 years. That trend has continued following the housing crash in what has been the weakest post-recession recovery in U.S. history.

Of late, in fact, people have gone backwards: Between 2009 and 2012, economists Emmanuel Saez and Thomas Piketty have shown, average income for nine out of 10 U.S. households fell nearly 16 percent.

"If you don't have enough left over in your paycheck, you don't feel as if you can put something away," Hiltonsmith said.

Denise Oseni, a 40-year-old mother of three from Alexandria, Va., can attest to that. A high school physical education teacher, she says she has been unable to save money. Although Oseni once had a 403(b) plan -- a tax-preferred savings account for people who work in public education -- through her school job, she was forced to tap the funds when she inherited her ex-husband's debt after getting divorced. She also suffered a serious injury at school and was forced to go on federal disability, reducing her income by two-thirds.

Oseni, who hopes to return to work, says she has found it all but impossible to save while raising two young boys and helping to pay for college for her oldest son. Taking in her elderly father, who can't afford senior care, has added to the financial stress.

"It's hard for me even to fathom how I can put money aside," she said, adding that paying for her home and meeting other expenses has taken precedence over saving for retirement. "I'm not really able to save toward retirement. I don't want to be a burden on my kids, but I do want to be able to maintain my own household."

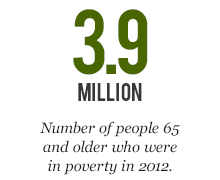

The main reasons employees cite for not stashing money away are the cost of living and day-to-day expenses, according to EBRI. Economizing can be even harder for older people, who make up a disproportionately large share of the long-term unemployed. Poverty is widespread among seniors -- about 9 percent of Americans age 65 and over are poor, according to federal data.

Many low-income older people also have health problems, resulting in higher medical costs. That often further drains retirement assets and can make it hard for seniors to extend their working lives, the standard advice these days for retirees with inadequate savings.

"High out-of-pocket medical, and especially long-term care costs, pose the greatest threat to older Americans' economic security," Richard Johnson, director of The Urban Institute's Program on Retirement Policy, told a Senate panel on aging last year.

In short, it's hard to save what you haven't got. And the reality in the U.S. today is that, like Oseni, tens of millions of Americans are just struggling to get by. Journalist and tax expert David Cay Johnston notes that almost a third of the roughly 154 million Americans who held a job at any point in 2012 made less than $15,000 a year.

For people in this group, saving for retirement is a pipe dream. And with so many people around the country today living paycheck to paycheck, including a growing chunk of the middle class, it doesn't take a prolonged bout of joblessness for the savings that people have managed to put aside to vaporize.

Better than it looks?

Trends in retirement aren't all bad. As women have entered the workforce en masse, their earnings have lifted family incomes. It also has allowed more women to accrue Social Security benefits and acquire 401(k) accounts of their own. Meanwhile, people with pensions may be financially secure in retirement even without personal savings.

Americans now in their 50s and 60s are also generally healthier and better educated than those in previous generations, allowing them to work longer and save more for retirement. And for some, retirement today is an opportunity to reorient their lives in ways they find fulfilling, whether pursuing a second (or third) career, traveling or simply moving closer to family.

"There has been a shift, [and] the biggest one has to do with the perception of what is retirement," said Rebecca Hall, an advisor with financial planning firm Ameriprise. "Now the conversation is, 'When is that point in time when I can do something different' -- that idea of semi-retirement."

Some experts also reject the premise that Americans actually face a retirement crisis. University of Wisconsin-Madison economist John Karl Scholz argues that families choose to consume more when children are at home, but reduce consumption when kids have left the nest. Given those lower spending needs during their twilight years, in his view, most people are saving enough.

As a result, Scholz contends that only a relative handful of U.S. households face a serious shortfall in retirement savings.

"We think there is very little evidence that Americans, at least for those born before 1954, are preparing poorly for retirement," he and his colleagues wrote in a widely cited 2008 paper. They also expressed confidence that "Americans are ... preparing sensibly for retirement, given the existing generosity of Social Security, Medicare and pension arrangements."

Meanwhile, even experts who concede 401(k) plans have serious deficiencies say they're the only game in town. And to be sure, not all plans are created equal.

Brightscope, a provider of retirement plan information and ratings, notes that some companies far surpass others in their funding contributions and other benefits, such as immediate vesting. It cites law firm Sullivan & Cromwell, health care management firm North American Partners in Anesthesia and accounting giant Ernst & Young among the U.S. companies with the best 401(k) plans.

Experts also say the retirement system can be improved. One idea is to roll out on a national level the kind of retirement plan that California introduced in 2012. Aimed at lower-income workers whose employers don't offer a plan, the California Secure Choice Retirement Savings Program requires employers to withhold 3 percent of an employee's pay, with participants automatically enrolled unless they opt out. Those funds are then invested under the state's pension system or by a private fund manager.

If a large segment of the population is ill-prepared for retirement, meanwhile, many people with decent jobs and income have managed to save sufficiently to live out their lives in relative comfort. It can be done (in part by applying some of the strategies that will be detailed in this CBS News Eye on America retirement series).

The trouble is that subpar 401(k) returns are but one symptom of what are deeper inefficiencies in the American retirement system -- inefficiencies that big-money politics make hard to root out. Just one example: The bulk of individual tax incentives for retirement savings go to the top 20 percent of income-earners, according to the Center for Budget and Policy Priorities. That means most of the tax breaks that reward savers go to people at the top, even though it's those further down the income ladder who need the most help saving for retirement.

This isn't only unfair, critics say -- it's bad for the economy. "Ultimately, there needs to be shared responsibility between employers, employees and government," Hiltonsmith said, in decrying the added risk being piled on workers.

For retirees, those risks aren't a matter of arcane public-policy disputes, but of simple survival.

"It's not comfortable, but I'm making it work," Galloway said of his current financial predicament. Still, he added, "If I live more than 10 years, I think I'll end up wiping out the savings."