Who's the bigger "currency manipulator" -- China or Taiwan?

Late Sunday night President-elect Donald Trump accused China of artificially devaluing its currency to gain an advantage in international trade. The charge of currency manipulation came after Trump’s controversial phone call with Taiwan’s president, a phone call that appears to have been arranged by former Senator Bob Dole, who was acting as a foreign agent for Taiwan’s government. However, if there is a case to be made that a country is a currency manipulator, the evidence is much stronger against Taiwan than it is for China.

There was a time when China intervened in foreign exchange markets to keep the value of its currency below the rate justified by economic fundamentals, but more recently China’s exchange rate management has been propping the value of the yuan up rather than suppressing its value.

Perhaps, as explained here by Brad Setser at the Council of Foreign Relations, a technical case can be made that China’s actions to bolster the value of its currency constitute a violation of the rules concerning currency manipulation, but that doesn’t mean pushing this issue is a good thing for the U.S. to do right now.

If China were to let the yuan float freely against the dollar, the most likely outcome would be a large fall in its value. That would increase Chinese exports to the U.S., decrease imports from the U.S. and put downward pressure on U.S. GDP and employment.

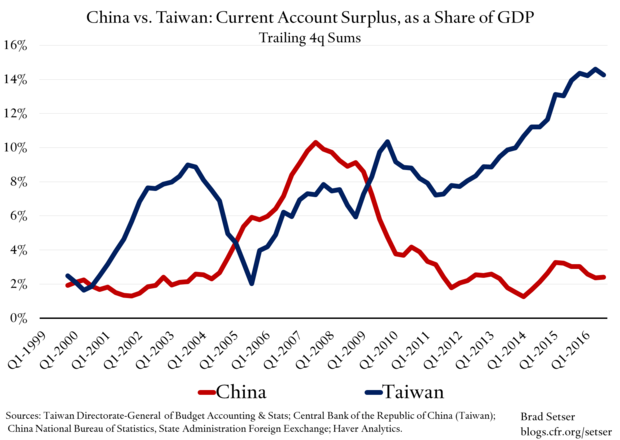

As Setser documents in further research, Taiwan is a different story. Its current account surplus was 14 percent of GDP in 2015, up from 10 percent in 2012, much larger than China’s surplus of between 2 and 3 percent, down from a peak of approximately 10 percent about a decade ago(chart above). According to Setser’s calculations, “Taiwan’s central bank clearly has been buying foreign currency in the foreign exchange market. The balance of payments data shows between $10 [billion] and $15 billion of purchases a year in recent years, and roughly $3 billion of purchases a quarter this year.”

That’s not the only piece of evidence pointing to Taiwan currency manipulation. As he noted, the country is also encouraging capital outflows in the private sector through regulatory changes. This is a way to put downward pressure on the currency’s value independent of central bank intervention.

Finally, in contrast to the yuan, which has strengthened in recent years, Taiwan’s real effective exchange rate has declined significantly over the last decade, and the drop is highly correlated with the rise of it current account surplus.

It’s not clear if Taiwan would meet all of the technical requirements to be sanctioned under the U.S. 2015 Trade Facilitation and Trade Enforcement Act. The law has numerical thresholds for the bilateral trade balance, the current account balance and the degree of foreign exchange market intervention, and it’s not clear that Taiwan’s bilateral trade surplus with the U.S. is large enough to cross the boundary.

But what is clear is that the case against Taiwan as a currency manipulator is much stronger than the case against China.

In light of this evidence, will Mr. Trump tone down the rhetoric against China and go after Taiwan instead? Don’t hold your breath.