A villain of the housing crash makes a comeback

The housing market crash, which started in 2007 and kicked off the Great Recession, blighted both the financial and real estate industries. Among the many participants whose reputations were ruined, few took more damage than the mortgage brokers who sold adjustable-rate mortgages. Known as ARMs, they became a four-letter word within the industry.

But nine years after their fall from grace into near oblivion, ARMs are making a slow, but steady, comeback. They're getting a boost from rising interest rates, which make them more attractive, better government regulations and, perhaps, more restraint from the mortgage brokers who sell them and are looking for redemption.

"ARMs carry the stigma of being the villains of the housing crash," said CEO Mat Ishbia of United Wholesale Mortgage, a national lending institution. "But they're still around and could be the right product for a lot of borrowers."

Prospective homebuyers, who can't afford to pay cash, have two basic mortgage options. The first is a fixed-rate loan, usually with a 30-year payback term to spread out the interest and principal payments. The other is an ARM, which comes in many different forms.

A simple ARM allows the buyer to obtain a fixed-rate loan for an initial set number of years, say, five or seven. Then over the rest of the loan term, the mortgage rate is adjusted, say, yearly or every three years, to the prevailing rate -- plus a margin -- that the mortgage lender pays to borrow the money it then lends out as a mortgage.

The adjusted rate for an ARM could be higher or lower than the original rate, depending on whether interest rates have risen or fallen. For example, if rates rise four percentage points, the ARM would also increase by that much.

That means you need to keep a close eye mortgage rates if you buy a home with an ARM. Otherwise you can wind up paying twice as much for your monthly mortgage bill if the ARM is repeatedly adjusted upward.

ARMs were immensely popular in the early 2000s, but fell into obscurity due to their connection with the subprime market crash (subprime loans are those made to borrowers whose credit rating isn't so good). Buyers who wanted to turn a quick profit on a home purchase used them as a way to "flip" houses and cash in on the soaring real estate market.

Banks and mortgage lenders expanded the types of ARMs they offered to the market during the housing boom to include "nontraditional options," said Chief Economist Mark Fleming of First American Financial, which provides title insurance and settlement services for the real estate market.

Tactics included "teaser rates" to lure buyers into special ARMs, which would reset every year or two, often without their owners realizing it. And "negative amortization," whereby you paid less than the minimum interest each month so the amount owed on the total mortgage increased rather than declined.

Subprime borrowers were given ARMs with no or limited documentation, meaning they didn't have to prove what their income was or even if they held a job (also known as "liar loans").

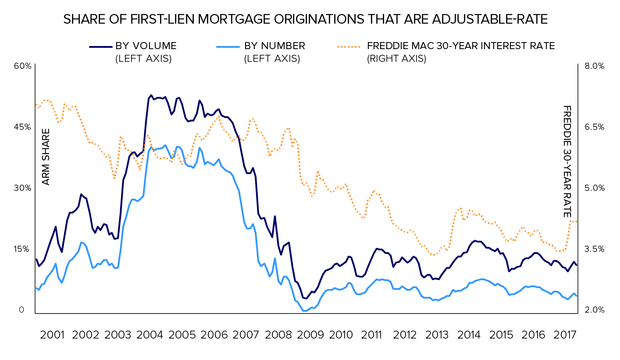

But many buyers still saw them as a good deal. In the greater Los Angeles area, a house hunter could buy a $400,000 home with just $10,000 down. ARMs represented more than 50 percent of the mortgage market in 2005. But when the recession came and foreclosure filings began to inch toward almost 4 million a year, ARM originations dropped close to zero.

It has taken a long time for ARMs to rebound, but that's the situation today. "They're about 5 percent of the market right now," said United Wholesale's Ishbia, "and we expect it to grow to 17 percent in two years." That would still be only third of its former size, according to Black Knight Financial Services, which provides data and analytics to the real estate industry.

The market also appears to be healthier this go around. Federal government-sponsored agencies such as Fannie Mae (the Federal National Mortgage Association), Freddie Mac (the Federal Home Loan Mortgage Corp.) and Ginnie Mae (the Government National Mortgage Association) are now offering ARMs. Also, the U.S. Consumer Financial Protection Bureau is placing tighter restrictions on the ARM market and is educating consumers on how best to use these loans.

According to a study by the Federal Reserve, ARMs are a play on rising interest rates. When rates are low, as they have been for many years, homebuyers prefer a fixed-rate 30-year mortgage. But the Fed is gradually raising interest rates due to an improving U.S. economy.

When mortgage rates head toward 5 percent, some borrowers may move to ARMs, which usually carry an interest rate more than half a percentage point lower than the 30-year fixed rate. During the life of an average mortgage, which is around nine years (because so many people sell before paying off their mortgage), the borrower of a $300,000 ARM could save more than $8,000, according to lenders.

And that's particularly true for first-time buyers, who are millennials these days. "Why borrow with a higher interest rate and pay a mortgage for 30 years, when the odds that you'll actually reside that long in the first house you buy are slim to none," said First American's Fleming.

But most prospective buyers still remember the homeowners who lost their houses because they gambled on ARMs in an overheated market. Even advocates of ARMs admit they're more complicated than fixed-rate loans and that you can't just shop online or go to your local bank and demand the best rate.

"Go to a broker," urged Ishbia. "It sounds counterintuitive to use a middleman, but they will shop for you and get you the best deal."