How to read a medical bill or explanation of benefits

Jeanne Pinder is the founder and CEO of ClearHealthCosts. Previously she worked for The New York Times for 23 years as an editor, reporter and human resources executive. This article was originally published on ClearHealthCosts.com.

The insurance company's "explanation of benefits" explains nothing. In fact it often confuses matters more.

Also: People believe their insurance companies are paying more than they really are, because quite often the explanation of benefits leads to that conclusion.

When I founded this company, in fact, a major impetus was the fact that no one could understand an explanation of benefits. Or a bill. Sometimes it seems that there's a conscious effort to hide information, just as there is in the old street-con card-hustler game called "three-card monte" (see an example in this YouTube video).

And in fact there is. Discussing the explanation of benefits, an insurance executive told me once, "We make them confusing intentionally, so people can't understand them." Anyone who has taken even a passing glance will say that confirms a suspicion: "This is not a bill" and "This page intentionally left blank" and "You may owe your provider" are all common occurrences.

This paperwork is described as "a mismanaged, tangled, screwed-up and incompetent mess," by Dave deBronkart, a.k.a. ePatient Dave, in this blog post; it takes off from a 2012 New York Times piece on the labyrinth of medical bills by Tara Siegel Bernard.

We've seen a lot of these in our reporting and crowdsourcing health prices with our journalist partners.

Because we've seen a lot of them and can show you the results, without revealing patient's personal health information but using their shared paperwork to enlighten you, we're doing this blog post with some examples.

Patterns:

- Insurers are paying a lot less than people think they are, and the EOB is designed to perpetuate that confusion. Often the insurer imposes a discount (or writedown or reduction) off the billed price, then adds the "discounted amount" and payment, and puts them on one line. This makes it look like the discount off the contracted rate is part of the payment. Time and again, people assume that the discount and the payment add up to the insurer's contribution. That is not true.

- Many insurers don't identify what procedure actually took place. They often leave out the procedure name and the procedure code, leaving the patient with only a date of service and a provider name. This seems intentionally obfuscatory. We have seen it before, and we think it's widespread in the industry — and a way of obscuring what really happened.

- Often the numbers on a bill don't add up. It seems sometimes that a string of chimpanzees are typing random numbers into a bill. This adds to the general confusion.

- Anyone who's tried to explain or argue a bill with the help of an insurer or a provider knows that hours on the phone in phone-tree and voice-prompt hell, and listening to hold music, are required to even ask a question. Asking the question seldom guarantees a straight answer.

So here are some examples of bills, part of our continuing effort to shed light on billing and explanation of benefits practices.

The insurer applied a "discount" to the billed price, but did not pay anything. The patient paid the allowable or discounted price in full.

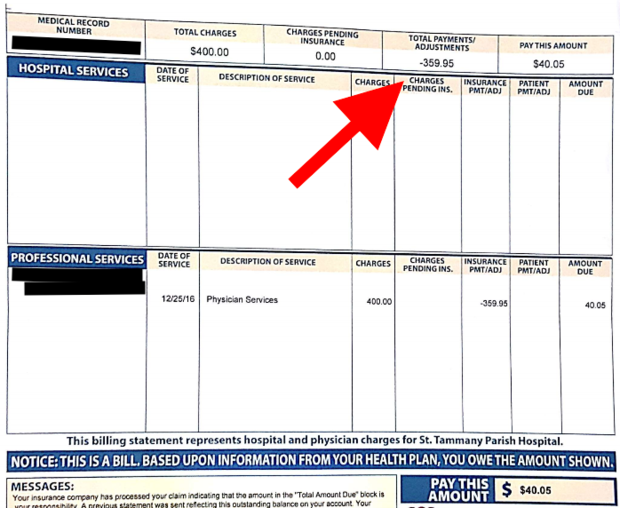

So how much did the insurance company pay? The payments/adjustments total $359.95, but how much was payment and how much was adjustment? The patient thought the insurance company paid the entire sum.

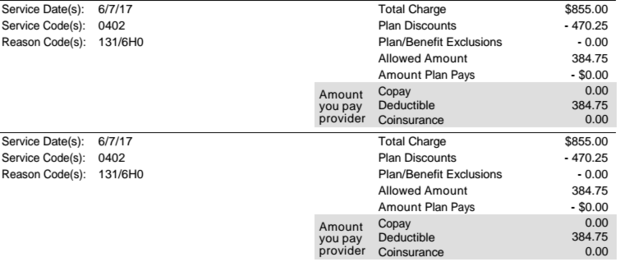

Exactly the same thing on exactly the same day? Two abdominal ultrasounds, one transvaginal and one not. And both are billed to her, with the insurer paying nothing. She has polycystic ovary syndrome, so this test must be done regularly, and she was shocked at this year's bill.

Same patient, same procedure, preceding year: Only one. That time, the plan paid $110.64, and only one was authorized.

A $2,130.90 bill. Insurance "discounts" of $1,432.03. Insurer paid nothing. Patient owes $698.87. The patient thought the insurer paid $1,432.03.

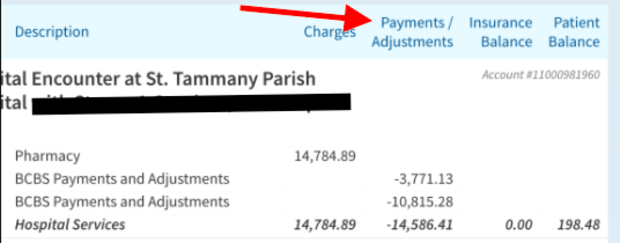

So the payments and adjustments (discounts, or whatever you want to call them) on this colonoscopy totaled $14,586.41. But what did they really pay? Also, it's a colonoscopy, so how could the charge be labeled "Pharmacy"? By the way, the patient believed, once again, that the insurer had paid the entire $14,586.41.

Discounts AND reductions from Blue Cross Blue Shield of Texas on this MRI. So Blue Cross wrote off or discounted $921.38, nearly 50 percent of the charge of $1,997.75. Our database shows you could have this MRI for cash in the New Orleans area from multiple providers for less than half the covered amount. Note "amount covered (allowed)" footnote refers to "the savings we've negotiated with your provider for this service."

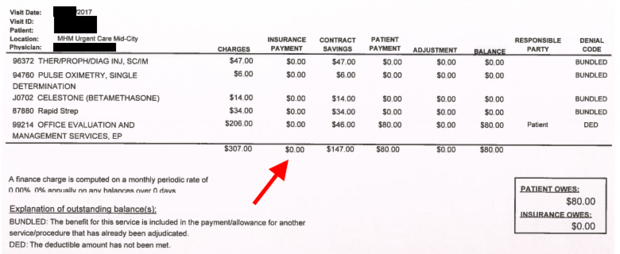

The numbers don't add up: Charge, $307. Contract savings, $147. Insurance paid, $0. Patient paid, $80. But $147+80=$227, not $307. So patient pays $80, twice? And what's the meaning of the denial code "bundled"? Confusing.

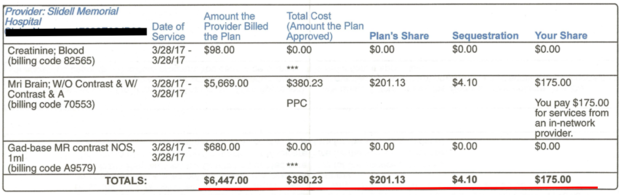

It's a bill for a brain MRI of $6,349. The insurer approved just $380.23; they paid $201.13, while the insured person paid $175. And what is the mysterious "sequestration" of $4.10″ ? Glad you asked! Look here and here: Automatic, across-the-board spending cuts from 2011. And that blood test — provider billed $98, plan approved nothing, and charged patient nothing. Mysterious.

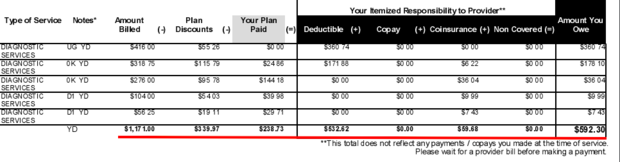

She said it was an "extracranial study" with a CPT code of 93880. On a bill of $1,171, they paid $238.73. She pays $592.30 in combination of deductible and coinsurance.

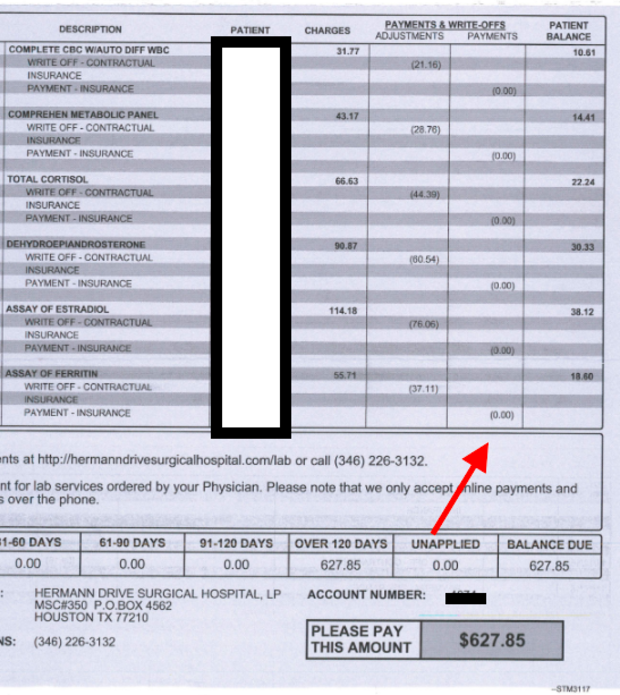

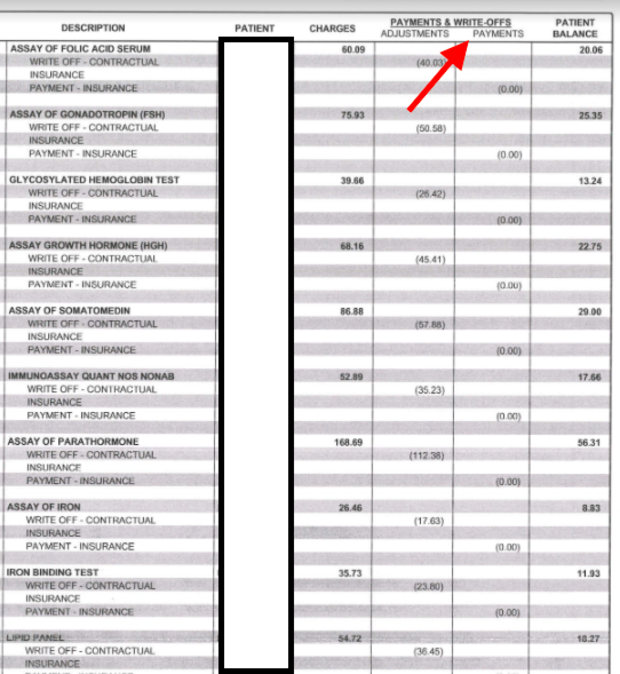

The insurer paid nothing on this long string of blood tests (partial bill). "There was an adjustment because I did have insurance," she wrote "the adj. of $1252.91 left me with the bill of $627.85. This was part of a physical that is fully paid by the insurance. I did not give permission to do tests that were not part of the covered physical exam but somehow still was billed for this."

Her note: "I got three stitches." Bill: $1,124. No insurance discount, no payment, no explanation — just instructions on how to pay.

"I have medical billing experience and even I can't understand or be certain of some of the things I am billed for," she wrote. "I know that I had a colonoscopy where 2 benign polyps were removed but I have no idea what the actual CPT code is that was submitted. While I know that a procedure may have many different CPT codes, can't the insurance company give at least a broad breakdown of these costs so that I can at least attempt to understand if I am being charged for the correct service? Additionally, I know that this charge does not include the charge for the pathology analysis of the polyps that were removed and I'm not entirely sure that the Anesthesiologist charge is included."

Emergency room charge: $2,130.90. Insurance paid nothing, but applied a $1,432.03 discount. She paid $698.87.

Gall bladder removal. Of the $10,577.10 charge, Blue Cross discounted $6,214.85 and paid $3,489.85; patient paid $672.46.

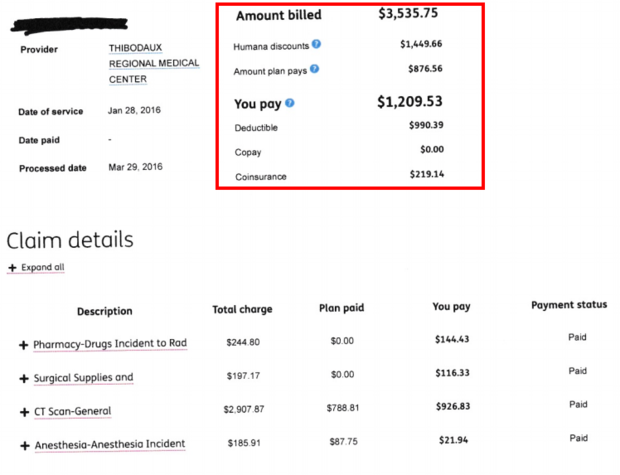

"This bill was for a CT scan of the elbow. I recieved a separate bill from the doctor that administered the meds during the CT scan."

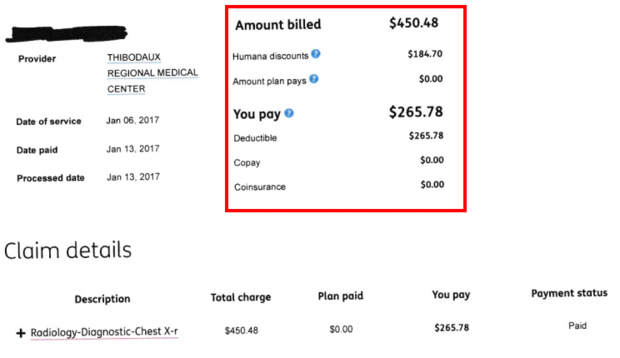

Chest X-ray for $265.78. Compare others here, from $20 to $988.

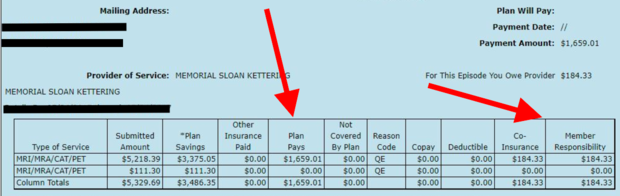

MRI at Sloan-Kettering. Fairly clear. Billed $5,329.69, plan paid $1,659.01, patient paid $184.33.

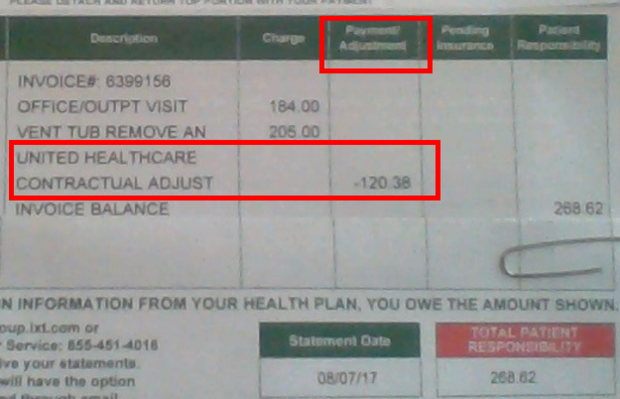

The insurer paid nothing. Instead, they just adjusted it down by the $120.38 — the sum is clearly marked as a "contractual adjustment" although the column heading says "Payment/adjustment."

Allergy test office visit. Charges $411; payment-adjustment together $341 — so what did they actually pay? No way to know.

A discount off a fancifully high sticker price does not necessarily mean you saved money. This procedure, an echocardiogram with Doppler, can be found under $400 on cash at many places in the neighborhood of Clearwater, Fla., where this procedure took place. Here's a search on our site for cash prices in that locale.

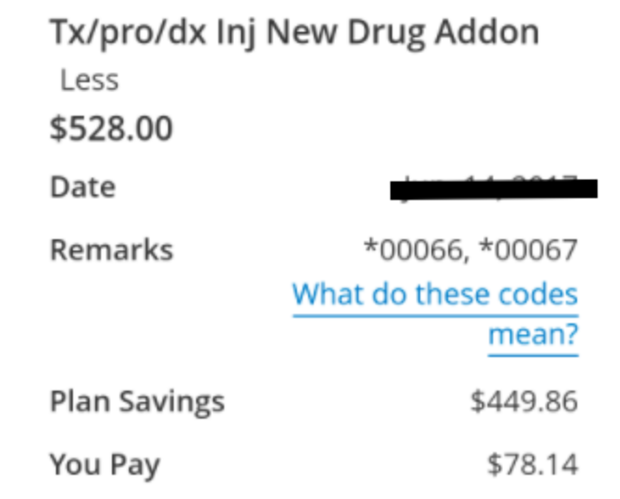

What did the plan actually pay? This emergency room visit shows "Plan Savings," which is clearly different from "Plan paid." But what did the plan pay? Nothing? And was the $449.86 applied to the patient's deductible?