What is the average credit score for millennials?

Millennials have lower credit scores than older generations and are using credit much differently, a new study by credit bureau Experian shows.

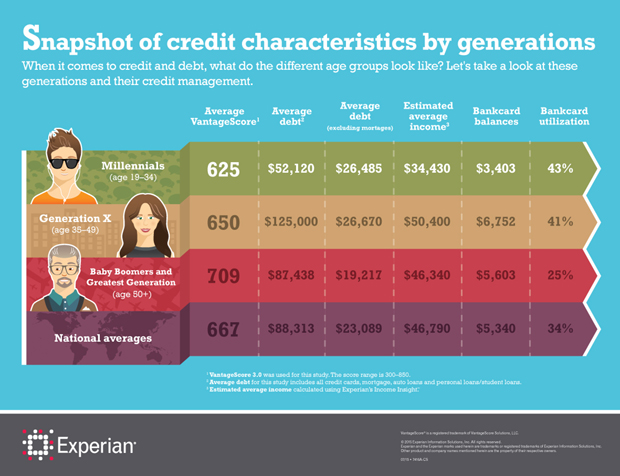

People aged 19 to 34 had a 625 average credit score, compared to 650 for Generation X (aged 35 to 49) and 709 for baby boomers (aged 50 to 69) and the "greatest generation," or those born around the Great Depression.

Millennials use more of their available credit card limits -- an average of 43 percent compared to 34 percent nationally -- while their average debt excluding mortgages equals 77 percent of their income, versus a 49 percent national average.

Contrasted with Generation X at the same age, millennials are:

- much more likely to have an auto loan than their predecessors, with vehicle loans comprising 14 percent of newly opened accounts compared to 1 percent for Generation X

- much less likely to apply for credit cards, with cards making up up 27 percent of their recently opened accounts, compared to 46 percent of Generation X

- somewhat more likely to have student loans, which make up 24 percent of recently opened accounts compared to 20 percent for Generation X

Experian used the VantageScore 3.0 credit score, which is a rival to the more widely used FICO credit scoring formula but works on the same 300-to-850 scale. Lenders have differing definitions of what constitutes a "good" score, but scores in the low 600s are typically considered mediocre or poor , while those above 700 are generally deemed good.

Low credit scores make it harder to qualify for loans, including mortgages, and could be a factor in the low rates of homeownership among people under 35. The U.S. Census Bureau says homeownership fell to 35.3 percent at the end of 2014, the lowest rate since the agency began keeping track in 1982.

Heavier student loan burdens have also been blamed for low rates of homebuying, but research by the Harvard Joint Center for Housing Studies found student loan payments didn't deter people from buying homes.

The lower scores are likely because millennials have thinner credit files than their older counterparts, so any missteps such as skipped payments or high credit utilization hurt more, said Michele Raneri, vice president of analytics for Experian.

One missed payment would be considered an aberration for someone who has responsibly handled several credit accounts for many years, but would be more worrisome for someone with few accounts and a short credit history.

"You don't know if it's a blip or not," Raneri said. "It could be that's their behavior that every three months or so they'll skip a payment."