Southwest revises its overweight passenger rules. Here's what's changing.

Southwest is walking back some recent changes in its policies for passengers who require a second seat.

Watch CBS News

Southwest is walking back some recent changes in its policies for passengers who require a second seat.

The rush to build thousands of U.S. data centers is driving demand for some workers, though economists project fewer permanent jobs.

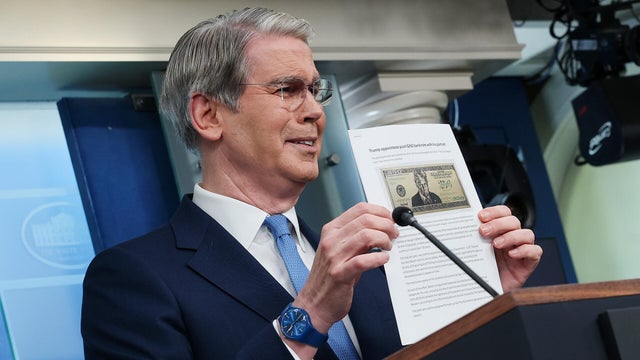

The department said it is preparing for the banknote in response to legislation proposed last year.

The Trump Accounts app allows parents to open new tax-preferred investment accounts for their children, including a $1,000 government contribution.

The personal consumption expenditures price index, the Federal Reserve's preferred gauge of inflation, jumped due to higher energy costs.

A software engineer at Google is facing federal charges after allegedly betting on confidential company information on Polymarket, netting more than $1.2 million in profits.

Australia is suing 3M for more than 2 billion Australian dollars ($1.4 billion) over so-called "forever chemical" contamination from firefighting foam at defense bases, the government says.

A household earning the average income would need to spend 40% of its income to afford the typical U.S. home, according to Redfin.

YouTube said it will automatically label photorealistic content created by AI, the video platform said.

Inheriting debt isn't common, but when it happens, it's important to understand the potential consequences.

A Federal Reserve meeting is set for mid-June. Here are three moves potential CD account holders should make now.

Mortgage interest rates spiked in May. Here are three dates on which they could fall again this June.

CBS News is tracking the rising cost of products most impacted by tariffs imposed and soon-to-be-imposed by President Trump, from grocery items to cars and trucks.

These charts track prices consumers pay for groceries and other goods now compared to five years ago.

Retirees say inflation, health care costs and market volatility are threatening their financial security.

As more people turn to chatbots for financial advice, experts say AI offers both pros and cons for retirement planning. Here's what to know.

Many employees expect to retire later as mounting expenses strain budgets, while others hunker down at work as part of the "great stay."

A summer job was once a seasonal tradition for millions of American teenagers. No more — here's why fewer young people are expected to clock in when school ends.

Employment watchdog accuses the New York Times of violating federal law by passing over a White male journalist for a job.

Since 2021, the share of U.S.-based employees who have left their jobs to work in another country has more than doubled.

A look at the features for this week's broadcast of the Emmy-winning program, hosted by Jane Pauley.

Southwest is walking back some recent changes in its policies for passengers who require a second seat.

Ricardo Hernandez-Navarrete graduated from high school after being released by ICE, but he and his mother still face the possibility of deportation.

The Justice Department announced the $1.7 billion fund as part of a settlement of a civil lawsuit President Trump brought against the IRS.

The five deaths came in vehicles that were struck by the bus when it did not slow down for traffic.

Southwest is walking back some recent changes in its policies for passengers who require a second seat.

The rush to build thousands of U.S. data centers is driving demand for some workers, though economists project fewer permanent jobs.

The department said it is preparing for the banknote in response to legislation proposed last year.

The Trump Accounts app allows parents to open new tax-preferred investment accounts for their children, including a $1,000 government contribution.

The personal consumption expenditures price index, the Federal Reserve's preferred gauge of inflation, jumped due to higher energy costs.

The Justice Department announced the $1.7 billion fund as part of a settlement of a civil lawsuit President Trump brought against the IRS.

A federal judge has ruled that execution by nitrogen gas doesn't violate the constitutional ban on cruel and unusual punishment, rejecting an Alabama inmate's claim that it causes excessive suffering.

The death toll from the Trump administration's series of strikes on suspected drug trafficking boats has risen to at least 199 people.

Former Attorney General Pam Bondi is testifying before the House Oversight Committee on Friday about her handling of the Epstein files.

Infectious disease specialists say the viruses are unlikely to become pandemics, but some are still raising concerns about the federal health response.

U.S. government plans to open a quarantine center for Americans exposed to Ebola on an air base in Kenya have been temporarily halted by a court order.

Infectious disease specialists say the viruses are unlikely to become pandemics, but some are still raising concerns about the federal health response.

The Trump administration announced plans to set up an Ebola quarantine and treatment center in Kenya for Americans exposed to the deadly virus overseas. Secretary of State Marco Rubio is now saying no Ebola patients will be allowed into the U.S. Mark Strassmann reports.

In the 1800s, Hartford, Connecticut, picked up the nickname, "The Insurance Capital of the World." Tony Dokoupil visits the city to ask people about rising insurance and healthcare costs.

Uganda on Wednesday ordered the closure of its border with Congo, where suspected cases of a rare type of Ebola are surging.

Police in Canada and around the world have been investigating more than 100 suicides linked to Kenneth Law.

The lead rescue diver told "CBS Mornings" earlier Friday that teaching the trapped miners how to scuba dive might be the only way to free them.

In the U.S. military's latest war games, AI took a front seat. A top commander told CBS News "it's not going to go away, and we ignore it at our own peril."

U.S. government plans to open a quarantine center for Americans exposed to Ebola on an air base in Kenya have been temporarily halted by a court order.

Trump said Friday that Iran must agree to never have a nuclear weapon and to reopen the Strait or Hormuz immediately, without tolls.

Musician Wyclef Jean is on a journey to release 7 albums as part of a single project titled "Quantum Leap." Jean joined CBS News with more details.

Grammy Award-winning artist Wyclef Jean released a new single, "Mr. October," from his new album "Clef Notes," which comes out June 26. The album is the first installment of this seven-album project "Quantum Leap." Jean joins to discuss why he plans to release seven albums in one year and the story behind his new single.

AI-powered shopping app Phia, founded by Bill and Melinda French Gates' daughter Phoebe Gates and Sophia Kianni, announced dozens of celebrity investors. Gates and Kianni share how they started the app and what's next.

Shrey Parikh, a 14-year-old eighth grader from Rancho Cucamonga, California, won the 98th annual Scripps National Spelling Bee. Lilia Luciano reports.

To mark the centenary of Marilyn Monroe, her last interview and last formal photo shoot, for Life Magazine writer Richard Meryman and photographer Allan Grant, are now presented in an expanded edition for the first time.

Dating apps are matching up with artificial intelligence as romance-seekers demand new ways to find love. Venture capitalist Matt Shumer joins "CBS Mornings" with more details.

Pope Leo has released the first encyclical of his papacy, focusing on humanity and, in part, warning of the risks posed by the growing use of artificial intelligence. The message comes amid growing dissent among young people over AI. Nicholas Thompson, CEO of The Atlantic, joins to discuss.

From labor shortages to environmental impacts, farmers are looking to AI to help revolutionize the agriculture industry. One California startup, Farm-ng, is tapping into the power of AI and robotics to perform a wide range of tasks, including seeding, weeding and harvesting.

A Google employee has been arrested for allegedly using insider information to make $1 million on Polymarket. Dustin Gouker, publisher of the Event Horizon newsletter on prediction markets, joins CBS News to discuss.

The digital investing platform Robinhood is now allowing AI agents to trade stocks and make credit card purchases for users. Yahoo Finance senior reporter Brooke DiPalma joins with the details.

The new species, named Microeledone galapagensis, has a blue hue, which is believed to be the rarest color in nature.

The Pentagon has released another batch of never-before-seen files on reported UFO sightings. CBS News senior national security correspondent Charlie D'Agata reports.

The 2026 Atlantic hurricane season is quickly approaching, and the National Oceanic and Atmospheric Administration is releasing its forecast for what to expect.

The pictures represent the longest-distance ever seen between two pictures of the same humpback whale, researchers said.

Independent scientists say the technology, while impressive, lacks some components to be truly considered an artificial egg.

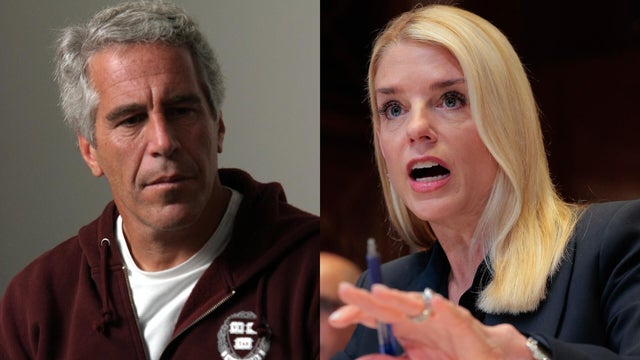

Former Attorney General Pam Bondi is testifying privately before members of the House Oversight Committee on the botched Justice Department rollout of the Epstein files. CBS News' Caitlin Huey-Burns reports.

Police in Canada and around the world have been investigating more than 100 suicides linked to Kenneth Law.

A federal judge has temporarily blocked the Justice Department from moving forward with work on the new "anti-weaponization" fund, including making any payouts. CBS News' Ed O'Keefe reports.

The Department of Justice is investigating the outside funding that Trump accuser E. Jean Carroll received for her civil lawsuits against the president. CBS News' Katrina Kaufman reports.

A man wanted in connection with the killings of three elderly men was caught after a massive search of Hawaii's Big Island that had left residents on edge.

A rare blue micromoon will appear in night skies this weekend. Here's what to expect.

Jeff Bezos' Blue Origin, Astrolab, Lunar Outpost and Firefly Aerospace are awarded with hundreds of millions of dollars in NASA contracts for the first phase of its moon base plans.

China has launched the Shenzhou 23 spacecraft with three astronauts heading to its space station.

Perfecting SpaceX's mammoth rocket will be critical to NASA's plans for returning astronauts to the surface of the moon.

The new rocket features a host of upgrades intended to improve safety and performance of the world's most powerful rocket.

A look back at the esteemed personalities who've left us this year, who'd touched us with their innovation, creativity and humanity.

Does the evidence show a cover-up, or was Todd Kendhammer wrongfully convicted for the murder of his wife?

Christy Salters-Martin dominated in the boxing ring but faced her toughest challenger at home.

Family seeks answers in death of newlywed who disappeared in 2005 while on Mediterranean honeymoon cruise.

Meet the tattooed beauty charged in the death of Google executive Forrest Hayes.

Federal Aviation Administration Administrator Bryan Bedford is reacting to Homeland Security Secretary Markwayne Mullin's suggestion to halt international flights to Newark, New Jersey, amid tense ICE protests. Lindsey Reiser reports.

Former Attorney General Pam Bondi is testifying privately before members of the House Oversight Committee on the botched Justice Department rollout of the Epstein files. CBS News' Caitlin Huey-Burns reports.

Ukrainian President Volodymyr Zelenskyy told "Face the Nation" moderator Margaret Brennan that his country is bracing for "big attacks" from Russia on Friday or Saturday night. "Our people have to be very, very careful, cautious, and children, and they have to use bomb shelters...nobody knows 100%, but there is a high percent," Zelenskyy said in an interview airing Sunday.

Multiple artists announced for America's 250th anniversary concert are no longer performing. CBS News' Lindsey Reiser reports.

President Trump said on social media that he's meeting with members of his national security team to discuss the latest round of negotiations with Iran. CBS News' Ed O'Keefe and Eleanor Watson report.