Where are the benefits of international diversification?

(MoneyWatch) A common refrain from some investors and a few in the financial media is that diversification is losing its importance due to globalization. Whilecorrelations rose during the financial crisis, they aren't the only thing that matters. As long as there's a gap among returns of different asset classes, there are significant diversification benefits -- and each year since 2008 there has been a wide dispersion of returns. For example, the Vanguard 500 Index Fund (VFINX) is up 15.4 percent through May 13, while the Vanguard Emerging Market Fund (VEIEX) was up just 0.1 percent. That's a large dispersion of returns. Other stock asset classes such as U.S. large and small value stocks outperformed the S&P 500, while international asset classes underperformed. And this relative performance was the reverse of what happened in 2009, 2010 and 2012, when international funds outperformed U.S. funds.

- How commodities can help a portfolio

- Physicist hedge fund guru posts lukewarm returns

- Most common retirement planning mistakes

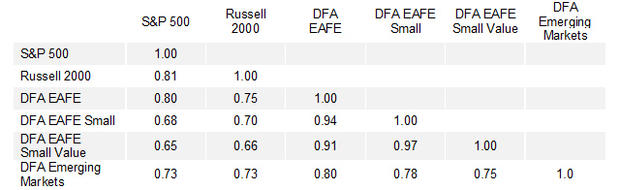

While understanding that the dispersion of returns matters, when we build a portfolio, all else equal, we would prefer to add asset classes that have lower correlations. With that in mind, we'll look at the correlation data for various asset classes to see which international asset classes provide the greatest diversification benefits. The table below shows the monthly correlations (so that we have enough data points) for the longest period for which we have data, January 1994-March 2013. The international indexes are provided by Dimensional Fund Advisors.

As you can see, the benefits of international diversification are greater when investing in international small stocks, international small value stocks and emerging markets than when investing in the international large stocks that are in the EAFE index. Interestingly, international small-cap stocks and small value stocks have even a lower correlation to U.S. small stocks than do international large stocks.

One explanation for this is that international small-cap and small-cap value stocks have greater liquidity risks including higher trading costs. Another explanation for the lower correlation is clear and simple -- many large companies are global giants, selling their products and services all over the world. Thus, while they tend to perform mostly like domestic companies in terms of returns, clearly global conditions will impact their earnings. On the other hand, many smaller companies are more dependent on the conditions of their local economies. Thus their returns are driven more by local, idiosyncratic factors. This makes them a more effective diversifier than international large-cap stocks.

As an example, the performance of two giant global pharmaceutical companies, for example, Merck (MRK) and Hoffman-LaRoche, is likely to be more highly correlated, because their products are sold worldwide, than the performance of two small-cap domestic restaurant chains whose products are sold only in their home countries.

Because of their lower correlation and the higher expected returns of international small-cap and small-cap value stocks, you should consider including an allocation to them when constructing your portfolio. Too many investors include only an allocation to the EAFE index. In fact, most investors should prefer them over international large-cap stocks.

Image courtesy of Flickr user 401(K) 2013.