How the four stock premiums work

(MoneyWatch) It's well established in the academic literature that there are four factors (or what can be called "drivers of returns") that determine the vast majority of the risk and return of diversified portfolios. They are are beta, which expresses the risk of the overall stock market; size, or the risk of small stocks; value, or the risk of value stocks; and momentum.

Those factors are all calculated as long-short portfolios. And they're calculated as annual averages, not compound returns. Each of the four factors has provided a premium return to investors.

- Beta is the return of the overall stock market minus the return of riskless one-month Treasury bills

- Size is the return of small stocks minus the return of large stocks

- Value is the return of value stocks minus the return of growth stocks

- Momentum is the return of stocks that have outperformed in the recent past (typically one year) minus the return of stocks that have underperformed

The first two premiums -- beta and size -- are considered risk premiums. There's a debate about the source of the value premium. Some believe that it's a risk story, as value stocks are riskier than growth stocks. Others believe that it's a behavioral story. (It's a free lunch because investors persistently overpay for growth stocks.) And some believe that it's a combination of the two (not a free lunch, but a free stop at the dessert tray).

There's no debate about the momentum premium, as it's purely a behavioral story -- its existence is the greatest challenge to the efficient market hypothesis. What we also know is that all four factors are both well known and have persisted.

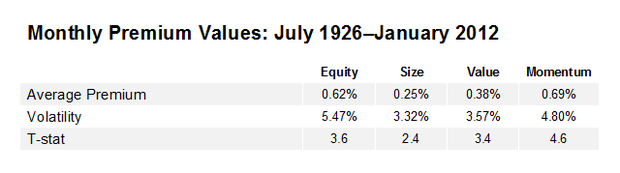

What would likely surprise many investors is the relative size of the premiums, as well as the level of their statistical significance. The following table provides the monthly equity, size, value, and momentum premiums for the longest time period for which we have data available, July 1926 through January 2012.

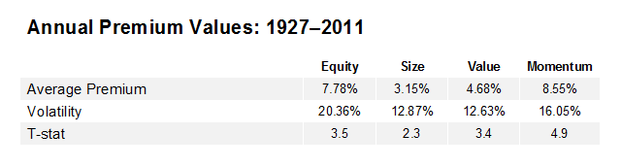

When we look at annual data for the period 1927-2011, we see similar results.

Not only has the momentum premium been the largest, but it has been the most statistically significant. There are a few other things that you should be aware of when considering the data.

Volatility

The volatility of the premiums is a multiple of the premiums themselves. So if you are going to invest in these factors, you must be prepared for a large amount of volatility in their returns.

Definitions

While the small premium has been less than the value premium, this is due to a difference in how the two premiums are defined. While the value premium is defined as the return of the top 30 percent of stocks as ranked by book-to-market minus the return of the bottom 30 percent, the size premium is defined as the return of the bottom half of stocks less the return of the top half. Since the smaller the market cap, the greater the return has been, using the same definition as used for value would have produced a greater premium.

For example, while the monthly return of stocks in the CRSP 6-10 deciles was 1.19 percent, the monthly return of deciles 8, 9, and 10 (the bottom 30 percent) where 1.24, 1.29, and 1.50, respectively. And while the return of CRSP deciles 1-5 was 1.19, the return of deciles 1, 2, and 3 (the top 30 percent) were 0.85, 1.00, and 1.05, respectively.

Compositions

Mutual funds are typically long only, not long-short portfolios (as are the factors). Thus, it's hard to capture the full premium. In technical terms, it's hard to have a very high "loading" (the degree of exposure to the factor) on some of the factors. Typically, well diversified stock portfolios will load at close to 1.0 (or 100 percent) on beta. However, it's hard to find value funds that have very high loadings on value, say above 0.7. But because of the less extreme definition of small stocks, you can find microcap funds that even have more than a 1.0 loading on the size factor. So it's more achievable in theory.

However, trading costs are greater in small stocks than in large stocks, increasing the importance of controlling those costs through patient trading strategies. (It's one reason why active managers in small stocks rarely outperform passively managed funds over the long term.)

Trading costs

Trading costs are also a problem for momentum strategies due to their high turnover (and the cost of shorting negative momentum stocks).

The bottom line is that while the premiums are impressive on paper, it can be a long way from strategy to realizable results. (Strategies don't have costs, but implementing them does.) Therefore, one must be cautious before trying to implement a strategy based on theoretical results. However, the historical evidence does demonstrate that there are fund families (such as Dimensional Fund Advisors and Bridgeway) that have created well-designed passively managed funds that have managed to capture a good share of the premiums (earning the return of the asset class in which they are investing). They have done so by maximizing the benefits of indexing (low cost, relatively low turnover, and relatively high tax efficiency), minimizing or eliminating the negatives (such as forced turnover and the realization of short-term gains) and incorporating momentum screens into their strategies.

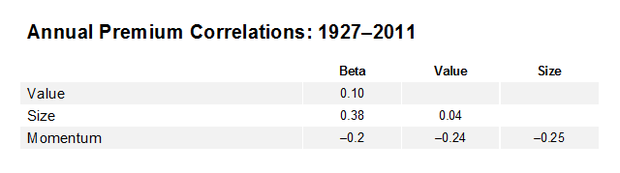

There's one more important point we need to cover regarding the four factors. The correlations of the returns of the four factors are low to negative, making them good diversifiers of portfolio risk. Remember, even though a total stock market fund owns both small-cap and value stocks, it has exposure to only one of the drivers of returns -- beta. The reason is that their holdings of small-cap (value) stocks are offset by their holdings of large-cap (growth) stocks, which have negative exposure to the size (value) factor. If you want your portfolio to be more diversified from the perspective of what drives returns, you need to "tilt" your portfolio so that includes exposure to these factors. The following table shows the annual correlations for the period 1927-2011.

Note the negative correlation of momentum to the other three factors. This is why there's increasing attention to how it can be incorporated into portfolio strategies.

Image courtesy of Flickr user 401K